- Oceania sees highest growth of 8%, China’s output up 3%

- Vedanta, PT Bintan expansions boost regional supply

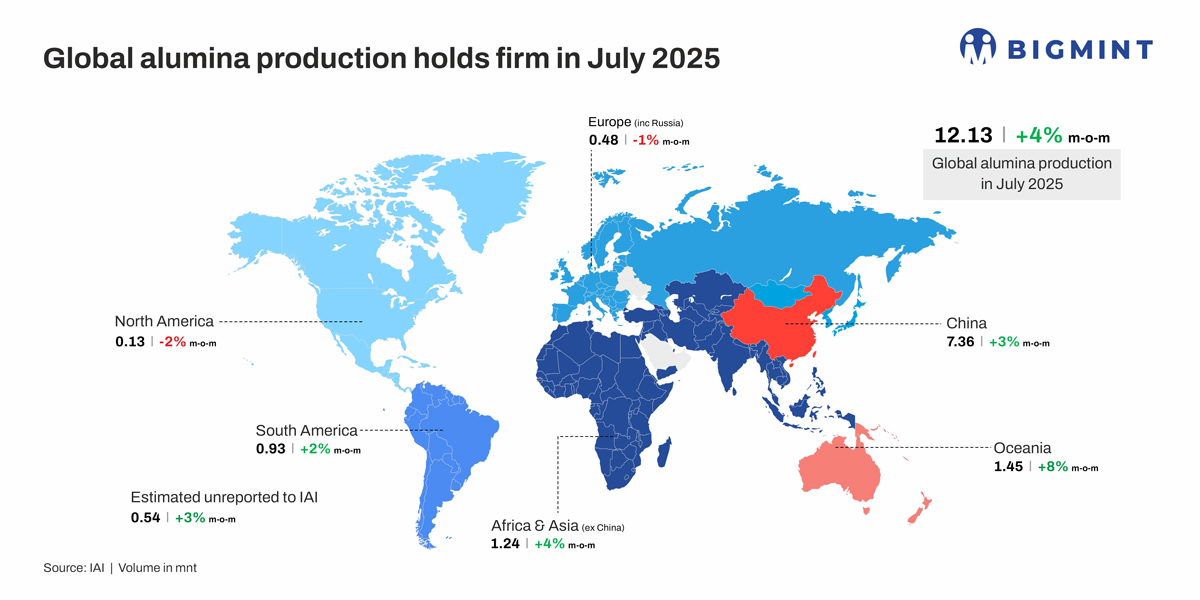

Global metallurgical alumina production rose 4% to 12.13 million tonnes (mnt) in July 2025 from 11.72 mnt in June, supported by stronger refinery operations and fresh capacity additions in Asia, according to the International Aluminium Institute (IAI).

On a y-o-y basis, production was also up 4.14% from 11.65 mnt recorded in July 2024, underlining a steady expansion trend.

Country-wise breakdown

China, the world’s largest alumina producer, posted an estimated output of 7.36 mnt, up 3% m-o-m from 7.13 mnt in June. The gain highlights stable refinery operations despite seasonal pressures, keeping China’s share well above 60% of global supply.

Oceania recorded the strongest growth at 8%, with output at 1.45 mnt in July against 1.34 mnt in June, supported by higher refinery run-rates. Africa and Asia (excluding China) also registered a 4% increase, reaching 1.24 mnt compared with 1.20 mnt in June.

South American production edged up 2% m-o-m to 0.93 mnt from 0.92 mnt, sustaining its gradual upward trajectory. In contrast, Europe (including Russia) saw a marginal dip of 1%, producing 0.48 mnt against 0.49 mnt in June. North America faced a sharper contraction of 2% to 0.13 mnt from 0.132 mnt.

Alumina output unreported to IAI was assessed at 0.54 mnt, up 3% compared with 0.52 mnt in June, further contributing to the overall expansion in global supply.

The July rebound underscores robust supply growth across Asia and Oceania, offsetting minor declines in Western markets. China’s sustained strength remains the cornerstone of global alumina output, while Oceania’s recovery signals critical support for seaborne trade flows.

Drivers of global alumina production growth in Jul’25

China remained a key driver of July’s alumina growth, with metallurgical-grade output rising 3% m-o-m as operating capacity and utilisation improved to around 81.6%. Northern plants expanded production notably, while southern refineries stabilised operations after routine maintenance, offsetting earlier disruptions.

At the same time, improved market profitability and favourable price dynamics encouraged refiners to maximise output. Strong alumina spot and futures prices, with arbitrage opportunities between domestic and overseas markets, further incentivised producers to operate at higher rates and tighten supply in certain regions.

Overseas capacity additions and smoother refinery operations also boosted global output. Indonesia’s PT Bintan Alumina started feeding its Phase III refinery, adding nearly 1 mnt/year capacity, while Vedanta’s 1.5 mnt/year expansion at Lanjigarh in India reached full production, lifting regional contributions.

Meanwhile, unlike previous months marked by seasonal shutdowns, July experienced limited maintenance disruptions, enabling steadier operations across major hubs and ensuring consistent supply growth.

Outlook

Global alumina supply is expected to stay strong in the coming months, supported by steady Chinese operations and higher run-rates in Oceania. Capacity ramp-ups from Vedanta and PT Bintan will further boost regional output, helping Asia offset weaker trends in Europe and North America, keeping global supply balanced in the near term.

Leave a Reply