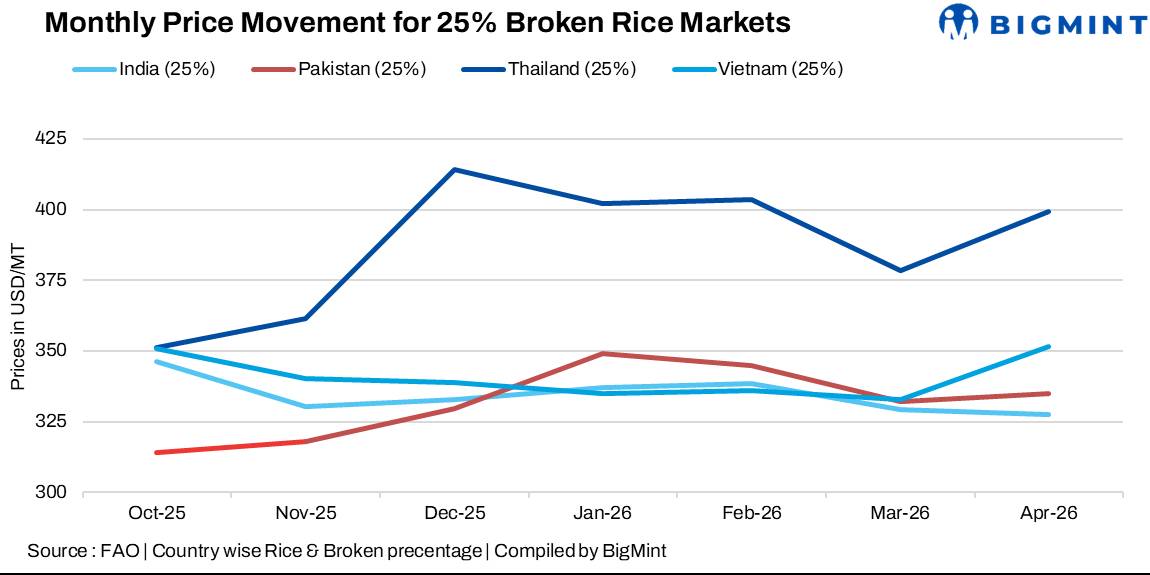

- Thailand continues to trade at a premium of $70/t above India

- Pakistani prices recover after aggressive price discounting phase

The global market for 25% broken non-basmati rice has witnessed notable price divergence among major exporters over the last months which is the peak export window. India remains the cheapest source, while Pakistan and Vietnam compete in the mid-priced segment, and Thailand maintains a significant premium.

Price movements between October 2025 and April 2026 reflect differences in domestic supply conditions, export demand, and pricing strategies across the four key rice-exporting countries. While the market remains well supplied overall, the widening price gap between origins is increasingly influencing buyer preferences and trade flows, with importers balancing cost competitiveness, quality, and supply reliability when making sourcing decisions.

India remains most competitively priced supplier

India has maintained a clear pricing advantage throughout the period, with export prices declining from $346/tonne (t) in October 2025 to $327/t in April 2026. The steady downward movement suggests comfortable domestic availability and strong exportable surplus, allowing Indian exporters to offer rice at the lowest prices among all major suppliers.

At the same time, import restrictions and tighter trade regulations in key West African markets — particularly measures aimed at controlling formal rice imports and protecting domestic currencies — have also weighed on buying activity, limiting demand from one of India’s major destinations. Slower offtake from these price-sensitive markets has added further pressure on exporters to lower offers and remain competitive.

Overall, India’s lower price positioning is strengthening its competitiveness and helping sustain export momentum.

Pakistan prices recover but remain above India

Pakistan’s 25% broken rice prices have followed a different path. Prices stood at $314/t in October 2025, then declined sharply till December 2025, following which there was a recovery to nearly $349/t in January 2026. Subsequently, prices eased slightly to $335/t in April 2026.

During the sharp decline in October-December, Pakistan’s 25% broken rice prices were temporarily trading below Indian prices. This was primarily driven by aggressive price discounting by Pakistani exporters, who were responding to intensified competition after India fully returned to the global rice market. With India offering abundant and competitively priced rice, Pakistan faced pressure to lower prices to defend market share in key non-basmati destinations.

At the same time, ample domestic non-basmati supplies and weaker export demand created inventory pressure, prompting exporters to clear stocks through lower-priced sales. Pakistan also appears to have shifted more volumes toward low-value markets, further pulling down average export prices.

Thailand continues to command highest premium

Thailand remains the most expensive origin in the market. Thai 25% broken rice prices rose sharply from $351/t in October 2025 to over $414/t in December, before moderating slightly to $399/t in April 2026. Despite the recent decline, Thailand still trades at nearly $70/t above India, reflecting tighter domestic supply conditions, higher production and logistics costs, and traditionally higher paddy prices.

Thailand’s focus on premium-quality rice and value-based exports also allows it to sustain a pricing premium over competing origins. However, this elevated pricing could reduce competitiveness in mainstream export markets, especially when buyers have access to cheaper alternatives from India and Vietnam.

Vietnam offers most stable pricing

Vietnam has shown the most stable pricing trend among major exporters, with prices remaining within a relatively narrow range of $333-351/t, ending at $351/t in April 2026. This stability reflects a balanced supply-demand situation, supported by steady availability from the Mekong Delta harvest, firm domestic paddy prices, and disciplined exporter pricing.

Positioned between India’s low-cost varieties and Thailand’s premium segment, Vietnam has maintained competitiveness by offering a balance of affordability, consistent quality, and reliable supply. Its growing focus on higher-quality, value-added rice exports has also helped support price stability, making Vietnam an attractive alternative for buyers seeking dependable sourcing.

Outlook

Going forward, India is expected to remain the global price benchmark for 25% broken rice, unless domestic policy changes or supply concerns emerge. Its pricing advantage is likely to continue attracting demand from key importing nations. Thailand may struggle to expand market share unless prices soften, while Pakistan and Vietnam are expected to compete for the middle segment of the market.

Overall, the widening price gap among major exporters suggests that buyer preference will increasingly depend on balancing cost and quality, with India likely to remain the preferred source for volume-driven demand and Thailand continuing to serve premium-oriented markets.

Leave a Reply