Freight markets, often overlooked in mainstream coal analysis, have become the decisive force behind global arbitrage in December.

A sudden, sharp decline in voyage rates has materially altered delivered pricing into China, India, and Southeast Asia.

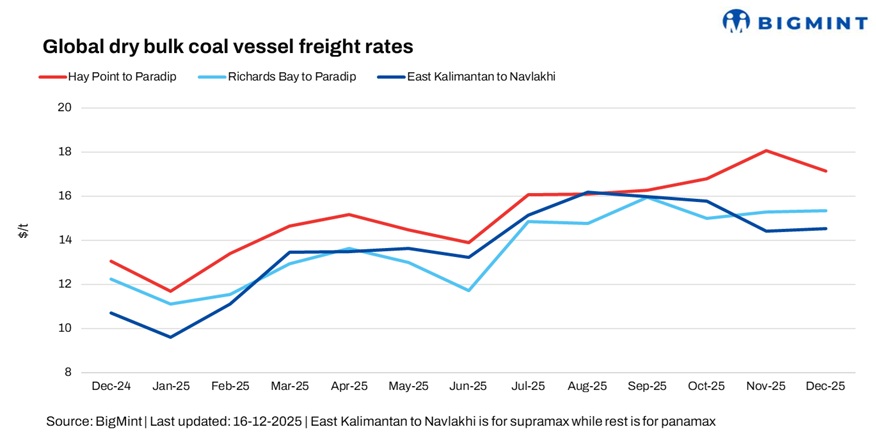

Major coal routes see dramatic rate cuts:

- Kalimantan → India West Coast Panamax: drops to $9/mt

- Australia → China Panamax: drops across spot and Q1 forward

- Panamax futures lose momentum

- Capesize 5TC rises slightly but Q1 forward collapses

The structural message is clear: Freight is falling faster than FOB coal prices.

Arbitrage reconfigured.

As a result:

Russia

- Delivered discount into China shrinks from $25/t to $20/t

Indonesia

- Delivered discount narrows by ~40%

Australia

- Suddenly competitive again into China

- NEWC 5500 moves from overpriced to strategically priced

India

- 5,500 NAR delivered drops to $92 CFR, despite weak FOB declines

Freight acted as a “shock absorber,” preventing seaborne prices from collapsing further even as Chinese domestic prices plunged.

Why this matters

Freight-driven repricing affects:

- Trade flows

- Supplier competitiveness

- Indian procurement

- Portfolio hedging

- Forward arbitrage positioning

- Coal/gas switching for utilities

In short, logistics – not demand – became the dominant price force this winter.

Leave a Reply