- Demand outlook improves with China’s rising imports

- Operational disruptions aggravate global supply tightness

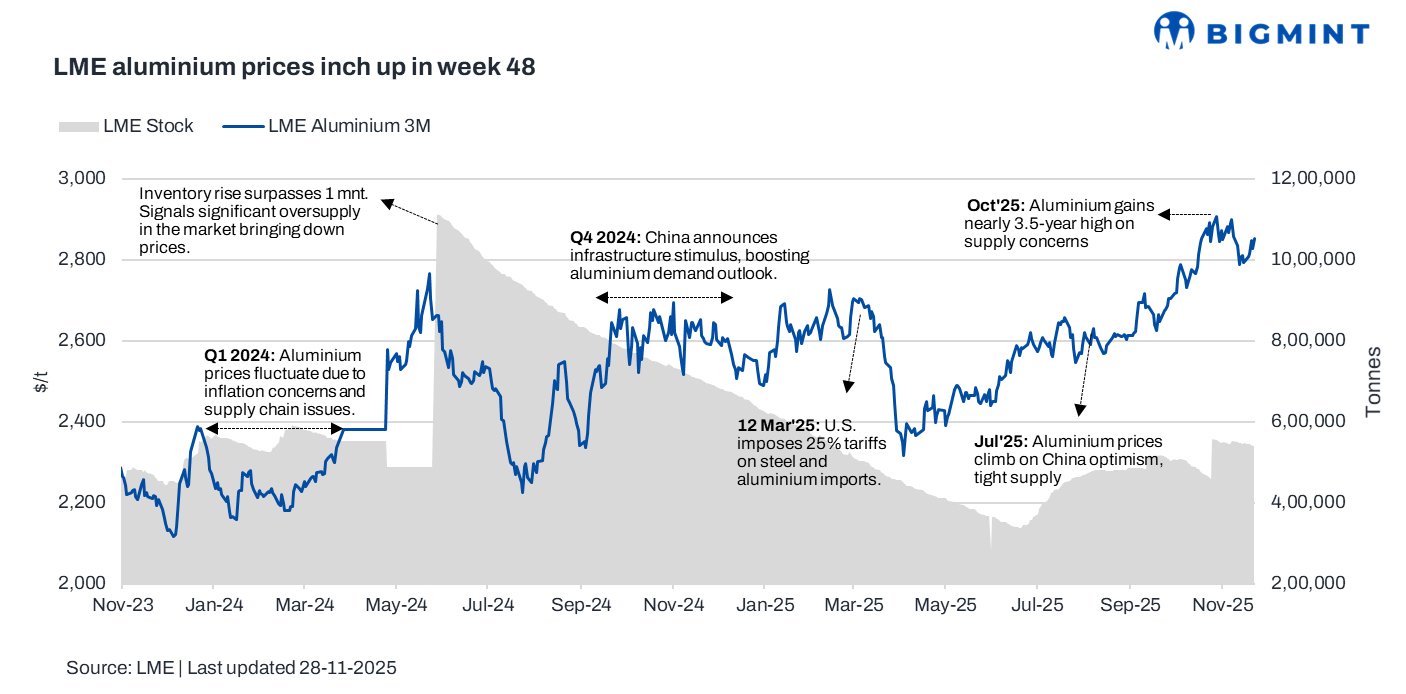

Aluminium prices on the London Metal Exchange (LME) edged higher w-o-w during week 48 of CY’25 (24-28 November) as expectations of a December US rate cut boosted market sentiment, while tightening global supply and steady Chinese demand added support despite mixed inventory signals and ongoing disruptions at key smelting and refining facilities.

Pricing, inventory trends

LME aluminium prices averaged $2,830/tonne (t) in week 48, marking a $24/t or 1% gain w-o-w from week 47 (17-21 November). The week began with prices at $2,808/t, which then rose to around $2,850/t mid-week. Prices closed at $2,852/t on 28 November.

Meanwhile, LME aluminium inventories witnessed minor outflows, with stocks down by 0.9% at 542,300 t in week 48 against 547,285 t in week 47.

What impacted prices in week 48?

LME aluminium prices posted a modest gain w-o-w, supported chiefly by rising expectations of a US Federal Reserve rate cut in December, following a series of dovish signals from policymakers. This shift improved overall risk appetite and lifted sentiment across base metals.

Supply-side factors also underpinned prices. Chinese smelters are nearing government-mandated capacity limits, restricting output growth at a time when demand prospects are firming. Global supply tightness was further aggravated by operational disruptions, including a potline shutdown at the Grundartangi smelter in Iceland, Alcoa’s closure of the Kwinana alumina refinery in Australia, and deep production cuts at Century Aluminium’s Iceland operations.

Industry data added to the mixed but generally supportive backdrop. The International Aluminium Institute reported a 0.6% y-o-y and 3.6% m-o-m rise in global primary aluminium output in October. However, inventory movements were uneven: SHFE stocks increased, while Japanese port inventories declined, offering no clear signal but reinforcing caution around availability.

On the demand side, China’s aluminium imports continued to rise, with October inflows up more than 10% y-o-y and strong year-to-date growth, reflecting resilient consumption in major downstream sectors.

Together, these factors — looser monetary expectations, tightening supply conditions, and steady Chinese demand — helped aluminium prices inch higher over the week.

Outlook

Aluminium prices are likely to remain supported in the near term as expectations of a US rate cut continue to buoy sentiment and supply constraints persist across key smelting regions. However, mixed inventory trends and uncertainty around China’s demand trajectory may cap sharp gains. Market direction will hinge on macro signals, energy prices, and developments in global production stability.

Leave a Reply