- Ex-mill rates rise despite weak port activity

- Trade sentiment may shift once paddy arrivals begin

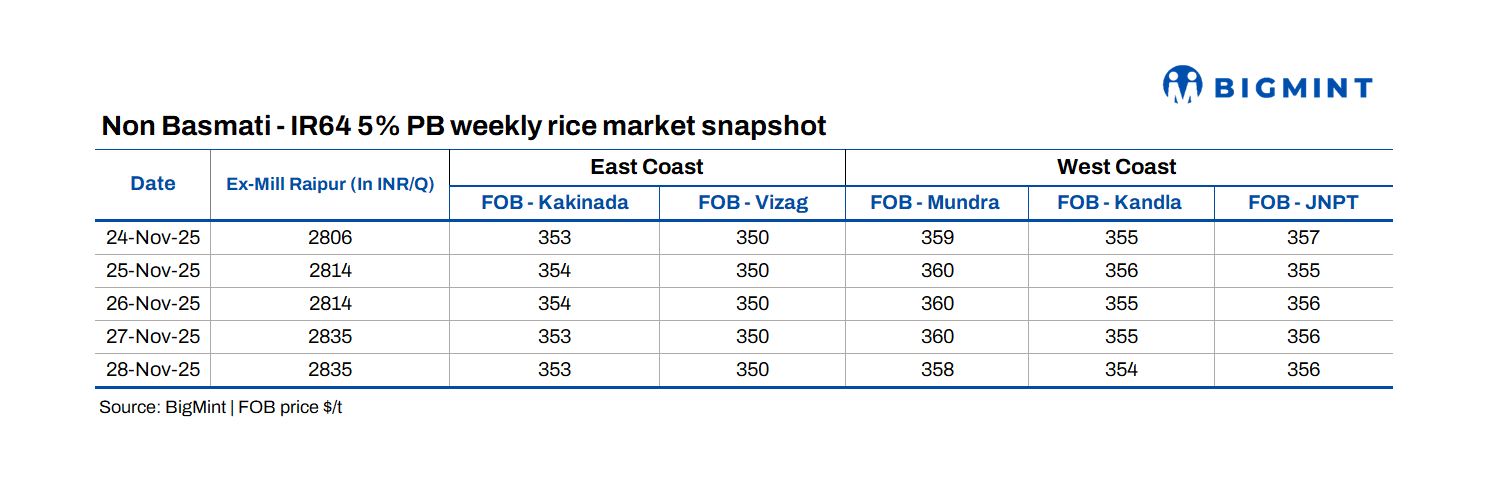

Chhattisgarh’s rice market remained unsettled through the final week of November as delayed government policies, thin trade and tightening paddy availability pushed ex-mill prices higher across the state. The ex-mill rate for IR 64 Parboiled 5% rice in Raipur climbed from INR 2,806 per quintal on 24 November to INR 2,835 by 28 November, reflecting millers’ difficulty in securing raw paddy and buyers’ continued resistance to higher offers.

Millers in Chhattisgarh expressed frustration at the late announcement of the Open Market Sale Scheme (OMSS), noting that most stakeholders have been focused on clearing government stocks ahead of new-season paddy arrivals. Trade volumes remained depressed for weeks as millers struggled to procure cargo, with many reporting that paddy scarcity has forced ex-mill values higher even as buyers quote aggressively lower rates.

Market participants expect conditions to shift from 30 November onward when paddy distribution begins. Government procurement is slated to start on 1 December at an MSP of INR 3,100 per quintal, a level millers say offers little margin and restricts their ability to source paddy for commercial milling.

Several millers noted that labour deployment, warehouse utilisation and financing flows remain strained, with bank guarantees on hold and GPS-tracked stock movements leaving little flexibility for raw rice handling. Warehousing has become a structural constraint, with facilities storing paddy rather than milled rice for up to three months.

Port activity remains muted as buyers hold back

Export sentiment was subdued across major east and west coast ports, with limited buyer interest keeping prices steady. At Visakhapatnam, rates held at $350/t from 24 to 28 November, while Kakinada rates, too, remained unchanged at $353/t. Mundra saw a marginal downtick from $359 to $358, Kandla slipped from $355 to $354, and JNPT slipped from $357 to $356.

Exporters reported weak cargo availability from Chhattisgarh for both Visakhapatnam and Kakinada, prompting buyers in these markets to quote INR 2,950 and INR 2,970 respectively for IR 64 PB 5%. Kakinada, however, continued to access local Andhra Pradesh supplies, keeping trade active at around $355/t. In contrast, old and recycled government-distributed rice continued moving from Mundra and Kandla to meet lower-grade demand in overseas markets.

Leading suppliers, including ITC, voiced concern over local market participants keeping offers artificially low to liquidate existing inventories, a strategy that has contributed to stagnant price momentum and further weakened private trade.

Policy drag continues to weigh on sentiment

A miller from Rajnandgaon noted that OMSS auctions proceeded at around INR 28 per kg, but traders expect a price revision as the scheme struggles to stimulate demand. Millers argued that custom milling remuneration remains inadequate at roughly INR 120 per quintal, given rising operating costs and restricted margins under MSP procurement. With business flows constrained, both employment and farmer-level transactions have slowed, deepening concerns across the value chain.

Following bulk cargo traditionally moves to Kakinada by rail, while coastal shipment proves costly. Several exporters had pre-bargained loading commitments but reported that commercial business has largely stalled as the market awaits clear policy direction and new-season arrivals.

Export trades provide limited support

Despite sluggish sentiment, a few deals were concluded during the week. A mill from Ranchi shipped 7,000 t of IR 64 PB 5% to Abidjan, Côte d’Ivoire from Kakinada. Also, a 500 t parcel of IR 64 PB 5% traded at $360/t from Mundra to Cotonou, Benin.

Outlook

Market participants expect the first and second weeks of December to determine the market’s direction as paddy procurement and government stock movement resume. For now, trade remains paralysed, margins compressed and supply-chain constraints unresolved leaving India’s rice sector waiting for clearer signals before activity can normalise.

Overall, the market is expected to remain cautious through the first half of December, with trade activity improving only after paddy movement and government stock releases ease supply constraints. A more decisive trend may emerge toward the end of the month once procurement volumes are clearer and liquidity returns to the milling and export sectors.

Leave a Reply