- CBAM implementation reshapes raw material trade flows

- Carbon costs emerge as a key competitiveness risk

Europe’s stainless steel market continues to face mounting structural challenges as subdued demand conditions coincide with tighter environmental regulations, reshaping trade flows and cost dynamics across the value chain. These trends were highlighted during a presentation at the The International Material Recycling Conference (IMRC) 2026, held by the Material Recycling Association of India in Jaipur by the Commercial Director of stainless steel recycling company Oryx Stainless Group, Joost Van Kleef.

CBAM impact on raw materials and trade

According to the presentation, the phased implementation of the EU’s Carbon Border Adjustment Mechanism (CBAM), effective from January 2026, is expected to materially alter stainless steel raw material sourcing. CBAM will progressively replace free carbon allowances, with imports of carbon-intensive materials such as ferronickel, nickel pig iron (NPI), and stainless steel slabs facing carbon-linked levies based on embedded emissions.

Industry estimates shared at the conference suggest CBAM-related costs for NPI imports could exceed EUR 200 per tonne of material once carbon pricing and reduced free allocation are factored in, potentially discouraging imports into the EU. While stainless steel scrap remains exempt from CBAM charges, reporting requirements will continue, reinforcing scrap’s strategic role in lowering the industry’s carbon footprint.

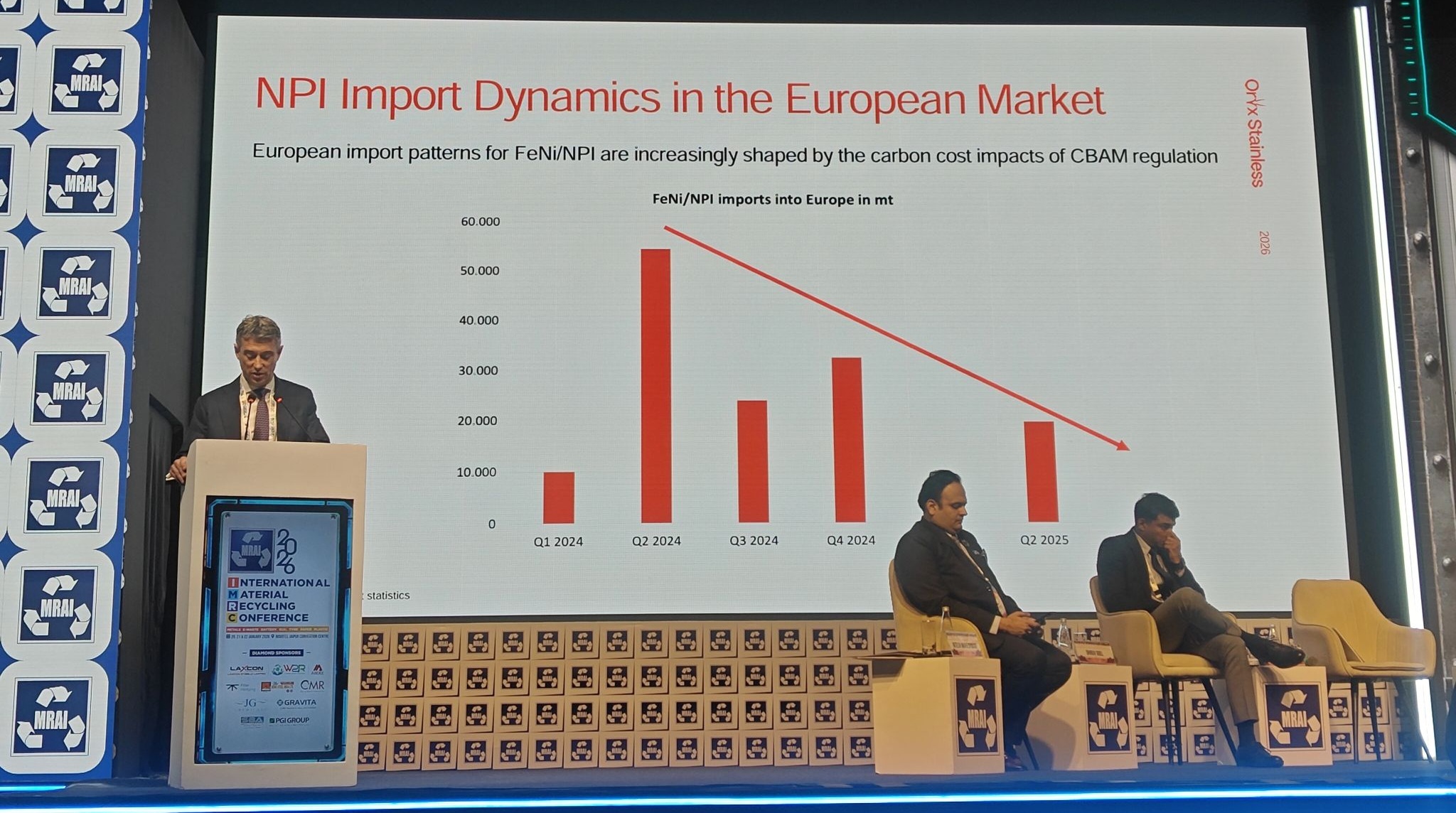

NPI import dynamics and CBAM application

From 2026, the EU’s Carbon Border Adjustment Mechanism (CBAM) will apply exclusively to Scope 1 emissions, covering direct emissions generated at production facilities. Imports of ferronickel (FeNi), nickel pig iron (NPI), and stainless steel slabs, which carry embedded Scope 1 emissions, will therefore fall directly under CBAM regulation. Indirect emissions from purchased electricity (Scope 2) remain excluded at this stage, except for cement and fertilisers.

Under the current framework, annual import volumes of 50 tonnes or less will be exempt, while stainless steel scrap will not be subject to CBAM surcharges, although reporting obligations will continue. The European Commission is expected to publish a scope review in Q4 2025, with a legislative proposal likely in early 2026 to extend CBAM coverage to additional sectors and potentially include indirect emissions.

Market participants cautioned that CBAM-related costs could materially raise landed costs for NPI and FeNi imports into the EU, accelerating shifts toward low-emission and scrap-based supply chains.

EU stainless flat market under pressure

EU stainless flat consumption has continued to decline, with around 500,000 tonnes per annum of demand “missing” compared with historical levels. Import penetration remains high, while capacity utilisation across EU mills has stayed uneven. Profit margins have tightened consistently over recent quarters amid weak demand, volatile energy costs, and rising compliance burdens, reinforcing calls for a more coordinated EU industry policy.

Outlook

As CBAM transitions from a reporting mechanism to a cost-bearing regime in 2026, carbon intensity is expected to become a decisive factor in Europe’s stainless steel trade, reshaping NPI import flows and further challenging the competitiveness of regional producers.

Leave a Reply