- EU’s crude steel production drops 3% y-o-y in Jan-June

- European scrap consumption drops on economic slowdown

- EC tightening scrap export regulations amid decarbonisation wave

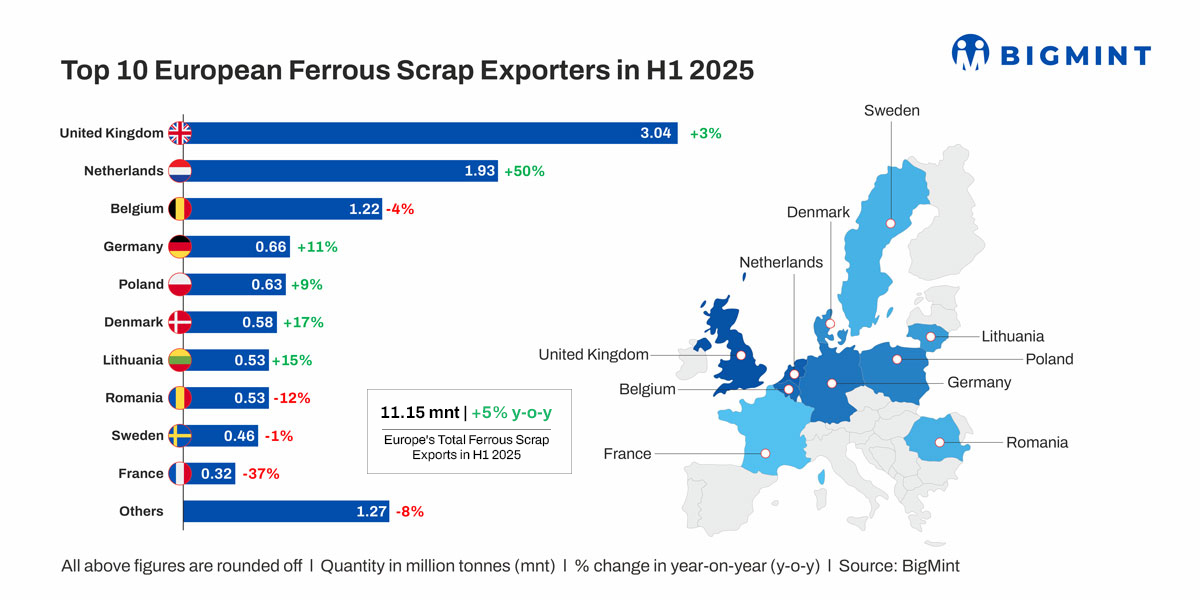

Morning Brief: In January-June 2025 (H1CY’25), the EU and UK raised their ferrous scrap exports to third countries by 5% y-o-y to 11.15 million tonnes (mnt), as per BigMint data.

The rise in export volumes was driven by an increase in shipments to major destinations such as Turkiye, Morocco, Pakistan, and other Asian countries. In H1, the EU’s crude steel production stood at 62.8 mnt, 3% lower than 62 mnt produced in H1CY’24, indicating relative stability after the Q1 slowdown.

EU: Macroeconomic backdrop in H1CY’25

Europe saw modest recovery in H1, supported by easing inflation, steady employment gains, and slightly improved consumer demand compared to the inflation-hit H1CY’24. Risks from global trade tensions and policy uncertainty persist, but sentiment remains cautiously optimistic.

In Q1CY’25 the economy expanded by 0.6% q-o-q, the strongest since Q3CY’22, led by Ireland’s 9.7% surge and solid growth in Spain (0.6%) and Germany (0.4%). Investment rose 1.8%, while household consumption slowed to 0.2%. In Q2, however, growth slowed sharply to 0.1% q-o-q, the weakest since late 2023, amid trade uncertainty, particularly from US tariffs.

Scrap market scenario

Overall, Europe’s ferrous scrap export market saw a rise in export volumes, particularly from key suppliers such as the Netherlands, UK, Denmark, Germany, and Lithuania, due to improved scrap availability and a decline in domestic scrap usage on a decline in crude steel production.

Despite a modest 0.4% GDP rise in Q1, Germany’s steel sector continues to falter. Crude steel output dropped 11% y-o-y in January-June, and recycled steel prices weakened in Q2 under the weight of a strong euro and soft domestic demand. Meanwhile, blast furnace production slumped and recyclers faced high collection costs with little margin relief.

In Scandinavia, the summer lull and geopolitical tensions trimmed scrap trade volumes. The UK faced a similar plight amid muted Turkish demand, volatile foreign exchange, and limited container space that kept market sentiment low, even as dockside prices ticked up. Supply tightness persists, with shredders operating at just below 50% capacity.

As per BIR data, in Q1, the EU-27 recorded a sharp 7.1% y-o-y decline in ferrous scrap consumption, which fell to 19.05 mnt. This contraction coincided with a 2.5% drop in crude steel output to 32.4 mnt, highlighting weaker industrial activity and cautious steel demand. Scrap collection remained steady compared to the previous year, but subdued demand weighed on consumption.

With low signs of economic recovery in Europe during Q2, ferrous scrap usage is estimated to remain stagnant or drop 1% q-o-q to around 18.5-18.8 mnt, taking total H1 consumption to roughly 37.5-38 mnt.

This shows that Q1’s gradual economic recovery was partly offset by declining steel demand in Q2.

Price movements

HMS (80:20) bulk prices FOB Rotterdam spiked in mid-Q1 but retreated sharply in Q2 as demand from key importers weakened.

In Q3 so far, prices have held steady at $315-320/t, signalling persistently sluggish buying interest and limited recovery prospects.

Outlook

On 23 July, the European Commission launched a customs surveillance system to track imports and exports of metal waste and scrap–including ferrous, aluminium, and copper–across the EU. The measure, part of the Steel and Metal Action Plan (SMAP) adopted in March, is designed to safeguard circularity and strengthen competitiveness as the bloc pursues its 2030 target of 55% emissions cut from 1990 levels.

The move comes amid a tightening scrap market, where rising exports to third countries are reducing availability within the EU and heightening concerns over supply security. The Commission is concerned that global market dynamics–such as the US’s recent 50% tariffs on a wide range of steel and aluminium products (excluding scrap)–could intensify incentives to ship scrap abroad, aggravating the EU’s own supply constraints.

Further threats to supplies from the EU and UK stem from Tata Steel’s GBP 1.5 billion EAF in Port Talbot to be commissioned in FY’27-28. The plant will produce 3-3.2 mnt of crude steel annually, consuming over 2 mnt of scrap. With scrap to form 70-80% of the charge, a large volume currently exported–7.5 mnt in 2024 and 1.9 mnt in Q1CY’25–will be redirected to domestic use. This shift could pressure exports.

The EU ferrous scrap export market is expected to remain stagnant or show only slight improvement in Q3, with exports likely hold steady as the European Commission seeks to shield the domestic steel sector from cheaper imports, particularly amid rising US tariffs.

At the same time, the tightening of the Waste Shipment Regulation (WSR) could further restrict exports to Turkiye, which takes over 60% of EU scrap. With EU steel-using sectors projected to grow 2.3% in 2025, domestic scrap demand will rise, further driving retention within the bloc. Yet, macroeconomic headwinds, geopolitical risks, and growing competition from Asian suppliers mean that the export outlook remains uncertain and global trade flows are increasingly volatile.

Leave a Reply