- EC directs Member States to avail of indirect cost compensation under EU-ETS

- Commission may extend CBAM to some downstream products in Q4CY’25

- EC will prepare setting of targets for recycled steel, aluminium in key sectors

Morning Brief: The European Commission has prepared a draft of the ‘Steel & Metals Action Plan’ which was presented in the European Parliament on 19 March 2025 following a strategic dialogue between the EU steel industry and Commission President Ursula von der Leyen on 4 March.

In terms of the steel industry’s environmental impact, the Action Plan spells out certain broad objectives which are as follows:

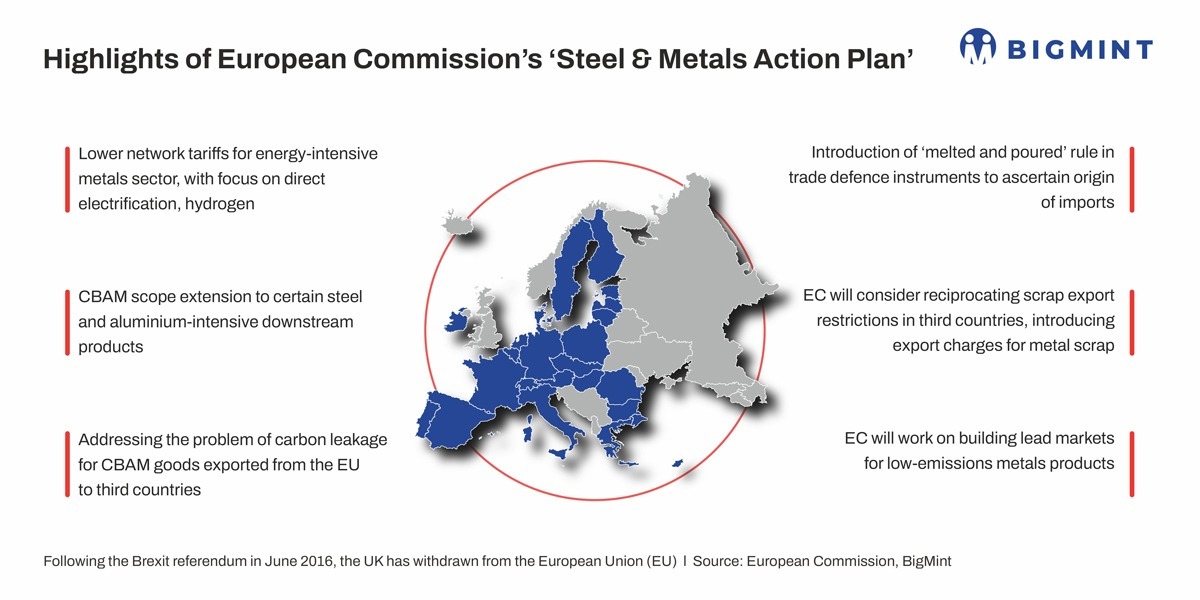

- Fast-tracking metals industry decarbonisation through direct electrification and adopting hydrogen in hard-to-abate sectors

- Increasing CBAM efficiency by addressing problems of circumvention and carbon leakage

- Assessing the need for recyclability and/or recycled content requirements for additional product groups

- Reciprocating export restrictions with third countries which have imposed curbs on scrap exports

- Creating lead markets which will lead to a broader adoption of low-carbon metals in Europe

Clean & affordable energy

In a bid to lower energy costs for the energy-intensive industries, the Commission is consulting Member States on a “State aid clean flexibility instrument based on (power purchase agreements) PPAs and industry committing to consume clean electricity. In addition, the Commission will provide guidance to Member States on the design of public support schemes for clean energy through two-way contracts for difference, including their combination with PPAs for the private sector. Such public support schemes should pay particular attention to energy-intensive industries and the metals sector”.

The objective is to accelerate grid connections and the uptake of renewable and low-carbon hydrogen.

The State Aid Guidelines for Emission Trading System (ETS) indirect cost compensation provide scope for Member States to compensate carbon costs passed on through electricity bills, for certain trade-exposed and carbon-intensive sectors, which include steel and other metals industries.

Hydrogen

Since direct electrification is not always possible or cost-effective, hydrogen is a key enabler of decarbonisation in the steel and metals industries. For example, direct reduction using hydrogen is the most promising option to decarbonise primary steel production, and hydrogen is the main contender to provide high-temperature heat in replacement of natural gas, the EC notes.

The Commission also announced in the Clean Industrial Deal it would adopt by this month the delegated act on low-carbon hydrogen to provide clarity for suppliers, off-takers and investors. The third call under the European Hydrogen Bank announced for Q3 2025 in the Clean Industrial Deal, will continue to support access to affordable renewable and low-carbon hydrogen for different off-takers, including steel.

Increasing CBAM efficiency

While CBAM introduces a measure on imported goods, it does not deal with the possible carbon leakage risks for metals produced in the EU that are subject to the EU ETS price and which are exported to third countries, competing with producers based in countries with lower climate ambitions. So, the Commission will propose a solution to ensure the effectiveness of CBAM and address the risk of carbon leakage (with the consequence of maintaining a level playing field for CBAM exported goods).

There is a risk that carbon leakage in CBAM-covered goods could shift further downstream in the value chain through circumvention, that is avoiding the CBAM obligations by making slight modifications to the CBAM basic goods or if EU consumers start favouring downstream goods imported from producers in third countries with weaker climate policies. The Commission is currently quantifying these risks and in Q4 2025 will propose extending CBAM to certain downstream products.

Moreover, there is a risk of circumvention of CBAM objectives when goods produced in low-carbon production facilities in third countries are redirected to European customers while carbon-intensive production continues for other markets.

To address these issues, the Commission will present an anti-circumvention strategy in the second half of this year.

Promoting circularity

The volume of scrap used for recycling in Europe is diminishing due to a lack of demand from the EU industry (especially for steel) and better market conditions for scrap in third countries.

Scrap should be better sorted and treated to ensure its usability in high-quality applications such as automotive. To facilitate the uptake of secondary content in such sectors traditionally dependent on primary metals, the Commission will prepare the setting of targets for recycled steel and aluminium in key sectors in a cost-effective way and a feasibility study for this will be completed by the end of 2026 as part of the End-of-Life Vehicles Regulation.

The EC will also assess the need for recyclability and/or recycled content requirements for additional product groups.

A number of third countries do not allow metal scrap to be exported to the EU, thereby reducing access to this strategic secondary raw material. That is why the Commission will consider proposing by Q3 2025 a measure on common rules for exports to reciprocate export restrictions with third countries.

Public support for decarbonisation

Low-carbon metals will remain more expensive than their conventionally produced alternatives for the foreseeable future. Lead markets, both public and private, will show the way for a broader adoption of low-carbon metals as the market standard.

As announced in the Clean Industrial Deal, the Commission will propose as part of the Industrial Decarbonisation Accelerator Act to introduce resilience and sustainability criteria to foster clean European supply for energy-intensive sectors.

To enable the industries investing in decarbonisation to reap ‘green premiums’, the Industrial Decarbonisation Accelerator Act will develop a voluntary label on the carbon intensity of industrial products. This should be the basis for further engagement with international work on measuring carbon intensity. In the interest of speed, the Commission will start with steel in 2025.

Leave a Reply