- Wide bid-offer disparities restrict trading activity

- Comfortable inventories reduce import demand

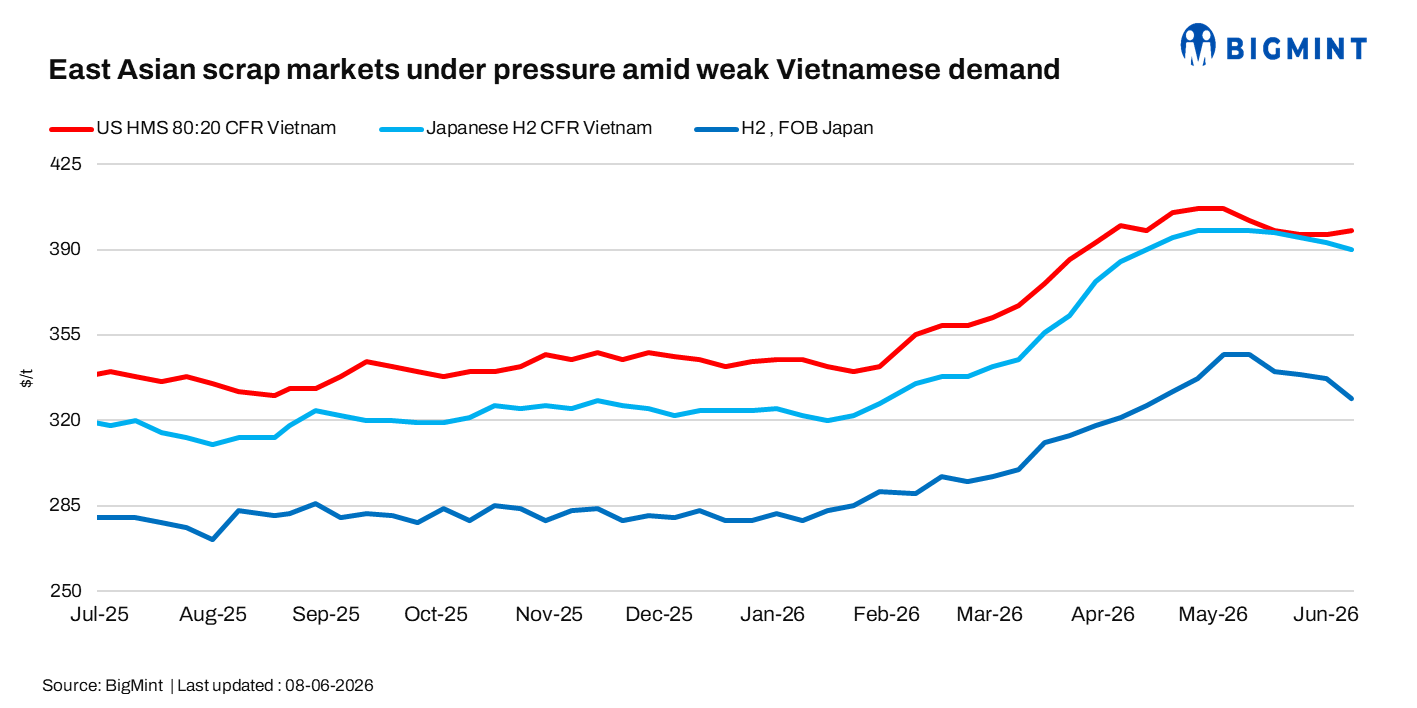

East Asian ferrous scrap markets remained under pressure during the week ended 8 June 2026, as weak Vietnamese steel demand, comfortable inventories, and cautious buying sentiment continued to weigh on import activity. Japanese export prices softened amid limited buying interest from key destinations, while deep-sea scrap offers remained largely stable.

Weekly assessments

- Japanese H2 scrap was at $390/t CFR Vietnam, down by $3/t w-o-w.

- Japanese H2 scrap was at JPY 52,700/t ($329/t) FOB Tokyo Bay, down by JPY 1,100/t ($7/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $398/t CFR Vietnam, up by 2/t w-o-w.

Japan

Japanese scrap export sentiment weakened during the week amid subdued buying interest from Vietnam and Bangladesh. H2 export prices were assessed at JPY 54,500-55,500/t ($340-346/t) FOB Japan, down JPY 500/t ($3/t) w-o-w, while H2 FOB Tokyo Bay prices fell by JPY 1,100/t ($7/t) to JPY 52,700/t ($329/t).

Vietnamese buyers were heard bidding at $380-385/t CFR for H2 scrap, while Japanese suppliers maintained offers at $387-393/t CFR Vietnam (around JPY 55,000/t FOB Japan). The wide bid-offer gap continued to restrict trading activity, although one deal was heard at $385/t CFR Vietnam during the week. Weak steel demand and seasonal factors continued to weigh on sentiment.

Meanwhile, H2 scrap offers to Bangladesh were heard at $420-425/t CFR, but buying activity remained limited as steelmakers returned from the Eid holidays and reassessed market conditions.

Vietnam

Vietnamese mills remained cautious as the rainy season slowed construction activity and weakened steel demand. Comfortable inventories and delayed infrastructure projects continued to limit scrap procurement requirements.

Japanese high-grade scrap offers declined by around $4-5/t w-o-w to $418-420/t CFR Vietnam, while buyers targeted below $408-410/t CFR, limiting trading activity. Weak longs demand, coupled with extreme heat and the onset of the rainy season, continued to weigh on construction activity and steel consumption, prompting mills to reduce rebar offers by around VND 300/kg ($11/t) w-o-w to VND 15,000/kg ($570/t) exw.

Deep-sea scrap prices remained largely stable, with US/Australia-origin HMS 80:20 offers at $400-405/t CFR Vietnam and bids around $395/t CFR. Buying interest stayed limited, with some buyers favouring deep-sea cargoes and domestic scrap over higher-priced Japanese material.

Outlook

BigMint expects East Asian scrap markets to remain under mild pressure amid weak Vietnamese steel demand and seasonal disruptions. However, stable Japanese collection prices and steady deep-sea offers may limit downside, while post-Eid demand in Bangladesh and Vietnam will remain key market indicators.

Leave a Reply