- Tokyo Steel hike lifts Japan H2 export prices

- Vietnam demand set to revive in March

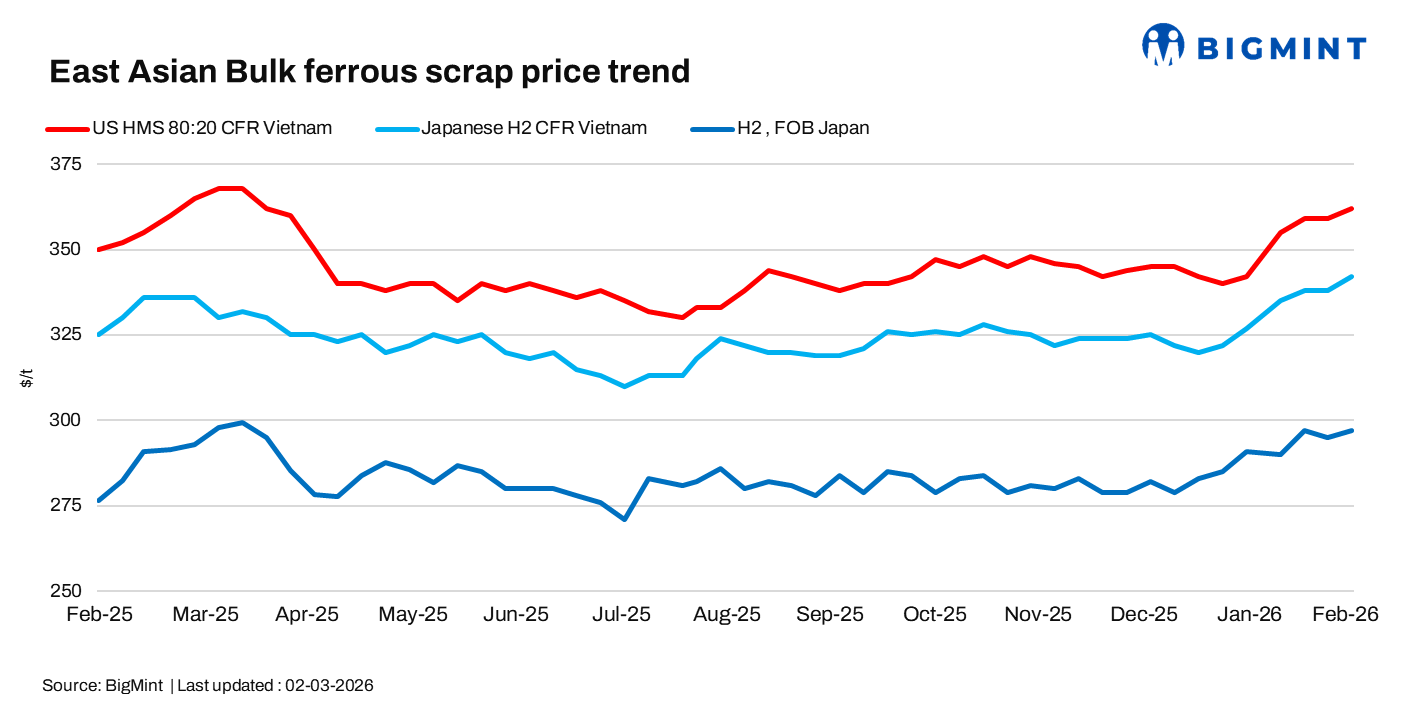

East Asian scrap markets firmed in the week ended 2 March , supported by Tokyo Steel’s latest domestic price hike and improving post-holiday sentiment. While trading volumes remained moderate, supplier expectations strengthened, narrowing downside risks across regional and deep-sea segments.

Weekly assessments

- Japanese H2 scrap was at $342/t CFR Vietnam, up by $4/t w-o-w.

- Japan’s H2 scrap at JPY 46,500/t ($296/t) FOB Tokyo Bay, up by JPY 900/t ($6/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $362/t CFR Vietnam, up by $3/t w-o-w.

Japan: H2 prices rise on stronger domestic cues

BigMint assessed Japan’s H2 scrap at JPY 46,500/t ($297/t) FOB Tokyo Bay on 2 March, up JPY 900/t w-o-w. The increase followed Tokyo Steel’s recent purchase price hike, which lifted supplier expectations and tightened domestic availability.

According to market participants, “Japan’s H2 scrap prices firmed on stronger domestic demand. Supplier sentiment improved, lifting export offers and FOB Japan H2 was heard at JPY 47,000-48,000 ($299-306/t).”

H2 offers to Vietnam were heard at $338-345/t CFR, up from pre-holiday levels of $332-335/t. However, bids were reported above $329/t CFR, leaving a visible gap between buyers and sellers. A weaker JPY partially offset higher offer levels, though the overall trend remained upward. Domestic H2 FAS collection prices also rose to around JPY 45,000/t.

Vietnam: Market to regain momentum

Vietnam’s import scrap market remained relatively slow as participants returned from extended holidays and finished steel demand stayed subdued. Rebar offers were steady at VND 14,300-14,600/kg ($547-558/t) EXW, while construction activity showed early signs of recovery.

The deep-sea bulk segment moved marginally higher, with HMS 80:20 assessed at $350/t CFR East Asia, up $2/t w-o-w. US-origin offers were heard at $360-365/t CFR Vietnam, while Australian cargoes were indicated at $355-360/t CFR.

Scrap inventories stood at 1.16 million tonne (mnt) in early February, sufficient for 26-27 days of operations at current output levels. With seasonal demand expected to strengthen from March and inventories gradually depleting, mills are likely to resume active scrap bookings in March-April.

Vietnam imported 0.39 mnt of scrap in January 2026, up 39% y-o-y from 0.28 mnt in January 2025. For CY’25, total imports reached 5.46 mnt, rising 22% compared with 4.49 mnt in 2024, supported by higher steel production.

Outlook

Japanese export prices are expected to remain firm, underpinned by domestic cost support and improved regional sentiment. Vietnamese buying activity is likely to pick up from March, potentially lending further support to regional and deep-sea scrap prices.

Leave a Reply