- Drop in bunker prices pressures freights

- China spot iron ore falls $8/t on tariff woes

Dry bulk iron ore freights declined on all major routes, except India-China where these remained stable. As global discussions over tariffs continue without clear direction, market participants are holding back, leading to subdued activity across major routes. This cautious sentiment has been felt strongly in the Pacific arena, where demand, especially from key loading regions and India, has remained limited. With fewer fixtures being reported, owners have found it increasingly difficult to maintain rate levels, resulting in a gradual softening of the market.

As vessels complete their voyages and re-enter the market, the supply-demand imbalance becomes more pronounced, giving charterers greater negotiating power. In regions like the South Atlantic and the Continent-Mediterranean, muted activity and weaker backhaul demand such as for cement have also dampened overall sentiment. This has created a ripple effect across other regions, including the Indian Ocean, where the oversupply of ships and cautious outlook from China on iron ore imports have together led to downward pressure on Supramax freight rates.

Meanwhile, the fall in Capesize iron ore freight rates is primarily driven by a combination of weak demand and oversupply of tonnage across both the Atlantic and Pacific basins. Charterers, benefiting from the oversupplied market and weak fundamentals, are bidding lower, testing owners resistance. Despite slight corrections in the FFA market, sentiment remains fragile, offering little support to physical freight levels. The muted activity out of South America, a key loading region for iron ore, further underscores the market’s lack of momentum.

A significant decline in bunker prices has exerted downward pressure on freight rates.

Factors influencing freights

- Baltic indices drop w-o-w: The Baltic Dry Index (BDI) was recorded at 1,489 on 7 April, decreasing by 113 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,219, decreasing by 253 points w-o-w, reflecting weak demand. The Baltic Supramax Index (BSI) also edged down by 24 points w-o-w to 971 points.

- China’s iron ore spot prices drop $8/t w-o-w: China’s spot prices of iron ore fines (Fe 62%) were assessed at $95.65/tonne (t) CFR on 8 April, decreasing sharply by $8/t w-o-w. Iron ore prices have fallen amid renewed US tariff concerns and weak demand for seaborne purchases. Mills are delaying purchases, expecting further price corrections due to poor macro-economic sentiments. The US plans to impose a 50% tariff on China if it doesn’t remove its 34% retaliatory tariffs on US goods, President Trump said on 7 April. With limited trading activity and expectations of weak economic indicators ahead, bearish pressure on prices persisted.

Route-wise updates

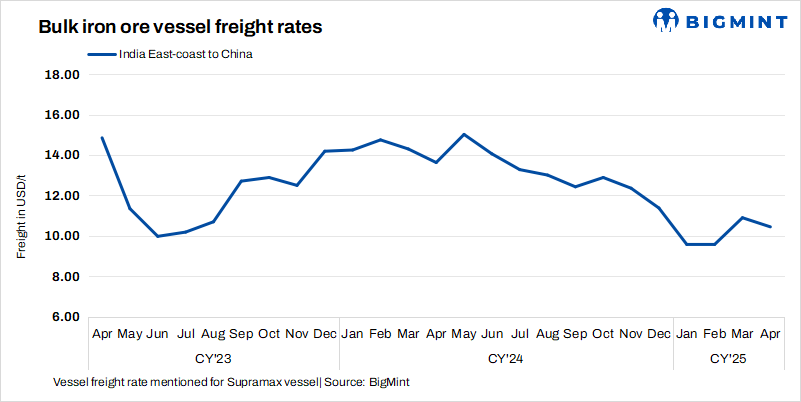

- India-China: Freights from the Indian Ocean to China were recorded at $10.5/t, remaining largely stable w-o-w. However, no fixtures were heard in this route amid weak demand in China post-Qingming Festival.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $7.7/t on 9 April, decreasing by $1/t w-o-w. According to sources, major Australian miners Rio Tinto, and FMG were seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $7.55-8.75/t. Shipment is scheduled for 21-27 April.

- Brazil-China: Freights for Capesize vessels from Brazil to China decreased this week. Rates from Tubarao to Qingdao Port were assessed at $20.6/t on 9 April, decreasing by $2.20/t w-o-w. As per sources, freight rates fell due to limited fixing activity and subdued trading during Asian hours, coupled with a lack of fresh cargo demand.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port dropped by $1.3/t w-o-w to $15.7/t. Sources informed BigMint that soft market sentiment and an oversupply of available tonnage weighed on rates despite stable cargo inquiries, leading to a decline in freight levels.

Leave a Reply