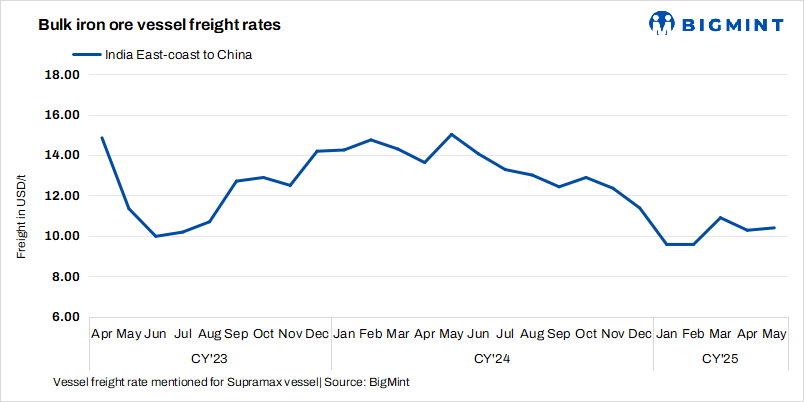

- Pre-monsoon restocking activity keeps India-China rates firm

- Baltic Capesize Index falls w-o-w amid reduced fixture activity

Dry bulk iron ore freights declined w-o-w across major routes, with the notable exception of the India-China corridor. While other routes saw easing demand and a build-up of prompt tonnage, the India-China segment remained firm, supported by strong market fundamentals and regional factors.

Freights on the India-China route faced upward pressure due to a spike in pre-monsoon shipment activity. With the monsoon season approaching, Chinese steel mills and traders accelerated their procurement of Indian iron ore. They aimed to complete shipments before adverse weather conditions disrupted port operations and loading schedules along the Indian coast.

This surge in cargo movement led to tighter tonnage supply in the region. As more vessels were tied up with pre-monsoon fixtures, availability for prompt loadings declined, increasing competition among charterers. As a result, freights on the India-China route remained largely firm.

Meanwhile, Capesize freights dropped due to weak market activity in the Pacific region. A key factor was the mismatch between the prompt availability of vessels and the laycan dates (loading windows) of cargoes. This disparity made it difficult for shipowners to secure suitable cargoes, leading to reduced fixture activity and a subsequent drop in offers.

Factors influencing freights

- Baltic indices fall w-o-w except for BSI: The Baltic indices, indicating trends in vessel demand, showed mixed trends w-o-w. The Baltic Dry Index (BDI) was recorded at 1,299 on 12 May, decreasing by 122 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 1,709, dropping by 370 points w-o-w. However, the Baltic Supramax Index (BSI) inched up by 14 points w-o-w to 969.

- China’s iron ore spot prices rise $2/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $101.25/tonne (t) CFR on 13 May, rising by $2/t w-o-w. Easing trade tensions between China and the US resulted in healthier market sentiment, and market momentum increased after the announcement. Mills’ outputs increased marginally, supported by strong raw material demand, healthy margins, and fresh steel trades.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.5/t, inching up by $0.2/t w-o-w. Market activity continued, with several fixtures currently under negotiation on this route.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $7.4/t on 14 May, falling by $0.4/t w-o-w. According to sources, major Australian miners Rio Tinto and BHP booked Capesize vessels from a Western Australian port to Qingdao at around $7.40-7.45/t. Shipment is scheduled for 29 May-2 June.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $18.4/t on 14 May, declining by $0.8/t w-o-w. As per sources, due to an expected oversupply of vessels and, then, a sudden increase in available tonnage, there was downward pressure on rates.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao decreased by $0.8/t w-o-w to $13.6/t on 14 May. Sources informed BigMint that Ore and Metal booked one Capesize vessel from Saldanha Bay to Qingdao at around $13.28/t, with shipment scheduled for 31 May-4 June.

Leave a Reply