- Monsoon affecting vessel availability

- Bunker prices inches down

Dry bulk iron ore freights remained subdued w-o-w, while higher cargo volumes supported vessel utilisation. While the Atlantic region remained subdued with limited fresh enquiries, improved activity from the Continent-Mediterranean also contributed to the upward pressure. This regional imbalance in demand and supply dynamics, particularly the stronger pull from Asia, has been driving the recent uptick in Supramax freight rates.

Conversely, Capesize freight rates to China have softened, particularly in the Pacific, due to a notable decline in cargo availability. The absence of fresh fixtures and reduced chartering activity have suppressed demand for Capesize vessels, applying downward pressure on rates.

Compounding this trend is a growing preference among charterers to split Capesize cargoes between two Panamax vessels, driven by operational flexibility and cost advantages. This shift has led to an accumulation of open Capesize tonnage in key loading areas, creating an oversupplied market and further depressing freight levels despite isolated firmness in the Atlantic segment.

Factors influencing freights

- Baltic indices decrease w-o-w, BSI goes contrarian: The Baltic indices, indicating trends in vessel demand, fell w-o-w. The Baltic Dry Index (BDI) was recorded at 1,689 on 23 June, decreasing by 279 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,879, sharply down by 843 points w-o-w. However, the Baltic Supramax Idex (BSI) inched up by 37 points w-o-w to 973.

- China’s iron ore spot prices remains stable w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $93/t CFR on 24 June, remaining firm w-o-w due to a combination of steady steel production, ample seaborne supply from major exporters like Australia and Brazil, and high port inventories in China that cushion short-term fluctuations. Additionally, muted restocking demand from mills, limited speculative activity in the futures market, and the absence of major policy changes in China’s steel sector have kept market sentiment balanced.

- Iran-Israel conflict: Despite a ceasefire announcement, market sentiment stays cautious. Minor bunker price correction was noted, but charterers remain on the sidelines, while most owners prefer to hold until clearer spot cues emerge, highlighted a source from shipping industry.

Route-wise updates

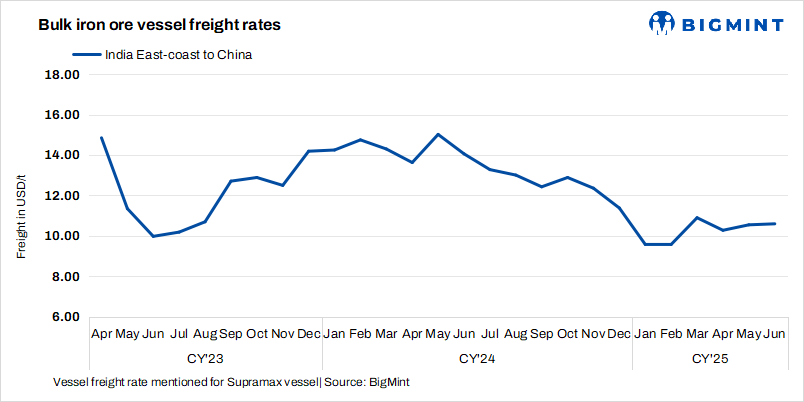

- India-China: Freights from the Indian Ocean to China were recorded at $10.6/t, inching up by $0.2/t w-o-w. The ongoing monsoon season has impacted vessel availability. Larger parcel sizes remain limited, tightening supply of bigger vessels. As a result, demand for Supramax vessels has increased.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $9/t on 25 June, decreasing by $1.9/t w-o-w. According to sources, major Australian miners Rio Tinto and BHP booked Capesize vessels from a Western Australian port to Qingdao at around $9.5-9.65/t. Shipment is scheduled for 1-4 July.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $22.8/t on 25 June, decreased by $3/t w-o-w. As per sources, two Capesize vessel got booked from Tubarao to Qingdao at $24-26/t for the shipment period of 16-25 July.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao dropped by $2.2/t w-o-w to $17.3/t on 25. It is heard that Ore and Metal booked one Capesize vessel from Saldanha bay to Qingdao at $16.88/t for the shipment period of 9-13 July.

Leave a Reply