- Volatility in bunker prices weighs on freights

- Baltic Capesize Index falls 204 points w-o-w

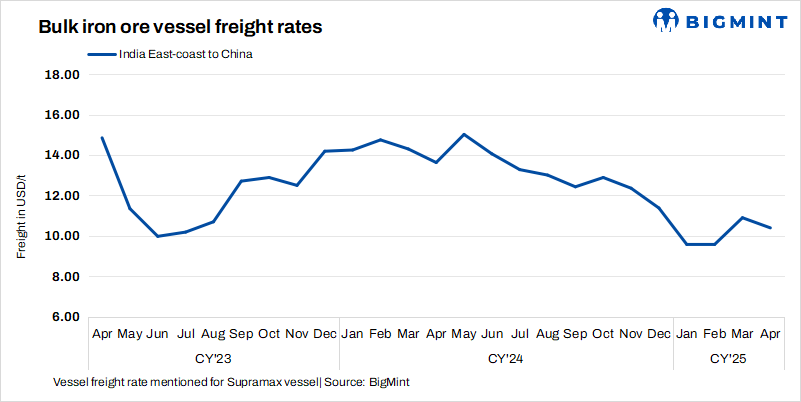

Dry bulk iron ore freights declined w-o-w despite a number of fixtures being recorded. Rates from India to China trended down this week amid sluggish market activity across the Asia-Pacific region. The ongoing Ramadan holidays in parts of Asia and the Middle East led to reduced trading, limiting fresh cargo inquiries. This decline in demand created an oversupply of tonnage, putting downward pressure on freights. Additionally, weak sentiment in the broader dry bulk market further contributed to the lacklustre conditions.

Volatility in bunker prices and imbalances in vessel availability also increased operational uncertainties. Consequently, charterers adopted a cautious approach, refraining from committing to higher freights. This hesitancy led to reduced trade volumes, exerting downward pressure on freights.

Meanwhile, Capesize vessel freights declined following the oversupply of ballasters in the Atlantic market. With a sufficient number of vessels repositioning to the region, the availability of tonnage increased, outpacing the current demand for cargo movement. This imbalance resulted in downward pressure on freights, particularly for forward-loading cargoes, where the lack of immediate fixtures led to weaker pricing sentiment.

However, major miners such as Rio Tinto, BHP, and FMG were active in securing tonnage at lower freights.

Factors influencing freights

- Baltic indices fall w-o-w: The Baltic Dry Index (BDI) was recorded at 1,602 on 31 March, decreasing by 41 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,472, falling by 204 points w-o-w, reflecting weak interest. The Baltic Supramax Index (BSI) also inched down by 17 points w-o-w to 995 points.

- China’s iron ore spot prices edge up by $1/t w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $104.1/tonne (t) CFR on 1 April, rising by $1/t w-o-w as steel mills expected a demand recovery in Q2 2025. However, there were concerns about the availability of economical materials. Seaborne market activity was limited, with a focus on higher-grade fines, while low- to mid-grade cargoes faced negative margins.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.4/t, falling by $0.6/t w-o-w. Some fixtures were under negotiation on this route, while subdued demand for vessel bookings exerted downward pressure on rates.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $8.7/t on 2 April, decreasing by $0.4/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP, and FMG were seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $8.60-8.75/t. Shipment is scheduled for 10-17 April.

- Brazil-China: Freights for Capesize vessels from Brazil to China decreased this week. Rates from Tubarao to Qingdao Port were assessed at $22.80/t on 2 April, dipping by $1.65/t w-o-w. As per sources, Vale booked a Capesize vessel from Tubarao to Qingdao at around $22.75/t, with shipment scheduled for 27 April-3 May.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port dropped by $1.7/t w-o-w to $17/t. Sources informed BigMint that Ore and Metal booked one Capesize vessel from Saldanha Bay to Qingdao at around $16.6/t, with shipment scheduled for 15-19 April.

Leave a Reply