- Iron ore shipments from Western Australia impacted due to rainy weather

- China seems to have completed iron ore re-stocking activities before holidays

Dry bulk freight trade activities have decelerated, experiencing reduced trading engagement as Chinese mills concluded restocking efforts ahead of the upcoming holidays.

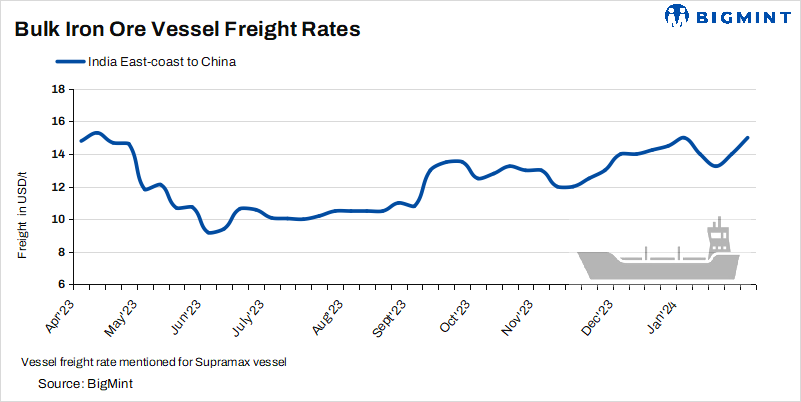

Asia-Pacific Supramax dry bulk (cargo capacity 50,000-55,000 t) freight rates for an iron ore-loaded vessel from the east coast of India to China was recorded at $15/tonnes (t) on 31 January, 2024, recording an increase of around $1/t w-o-w, according to BigMint’s assessment.

Route Specifications:

- Australia-China: Wet weather conditions in Western Australia have led to a decline in iron ore shipments, resulting in below-average shipping volumes from the region.

- Brazil-China: This route is currently seeing the strongest gains, with rise in fresh enquiries and cargo volumes. The freight has slightly declined due to vessel availability.

- India-China: The route has recorded higher fixtures with less trade volumes, as demand for small vessels is high. As per sources stated, “Market fixtures in east coast of India (ECI) are higher.”

Capesize freight drops w-o-w: Capesize freight rates have decreased due to reduced demand for large vessels and sluggish trading activity. Sources indicate that the movement of cape vessels has slowed down, influenced by geopolitical issues impacting freight rates. High bunker prices and limited tonnage availability have further contributed to the pressure on freight rates.

Outlook: Dry bulk freight rates are expected to remain volatile due to certain factors, which are upcoming Lunar holidays in China. Additionally, the potential increase in available vessels as Chinese New Year approaches could put downward pressure on rates.