- Limited vessel availability pushes up rates

- Active bookings seen from Australian miners

Dry bulk iron ore freights increased w-o-w on various routes amid favourable market sentiment.

The uptrend on the Indian Ocean to China route could be attributed to a combination of supply-demand dynamics and market optimism. First, vessel availability was relatively tight, with shipowners maintaining an optimistic stance and holding out for higher rates. Stronger demand on alternative routes also pulled vessels away from the Indian Ocean, reducing supply and adding to the upward pressure on freights.

This was further compounded by a slow start to the trading week in the Indian Ocean, where limited cargo availability created a sense of urgency among charterers. As a result, those needing to secure tonnage were willing to pay a premium, which pushed freights higher.

The broader Pacific Basin market outlook remained firm too, which encouraged owners to resist lower bids and wait for more favourable fixtures. Furthermore, seasonal factors, including stockpiling by Chinese steel mills ahead of anticipated production increases, drove increased iron ore shipments, further tightening vessel availability.

The rise in iron ore Capesize vessel freights could be attributed to heightened demand in both the Pacific and Atlantic basins, driven by increased activity from major miners and a surge in cargo demand from South Brazil and West Africa to China. In the Pacific, weather-related port closures in China disrupted vessel operations, leading to tighter tonnage availability and higher freights.

Factors influencing freights

- Baltic indices rise w-o-w: The Baltic Dry Index (BDI) was recorded at 1,669 on 17 March, increasing by 269 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,857, rising by 435 points w-o-w, reflecting positive sentiment. The Baltic Supramax Index (BSI) also climbed up by 66 points w-o-w to 930.

- China’s iron ore spot prices increase by $2/t w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $103.5/tonne (t) CFR on 18 March, rising by $2/t w-o-w amid stable steel mill margins, steady liquidity in the seaborne market, and a preference for medium-grade fines due to their faster consumption and better market liquidity. While hot metal production has yet to show strong seasonal growth, the gradual improvement in mill profitability has encouraged more medium and high-grade iron ore trades.

Route-wise updates

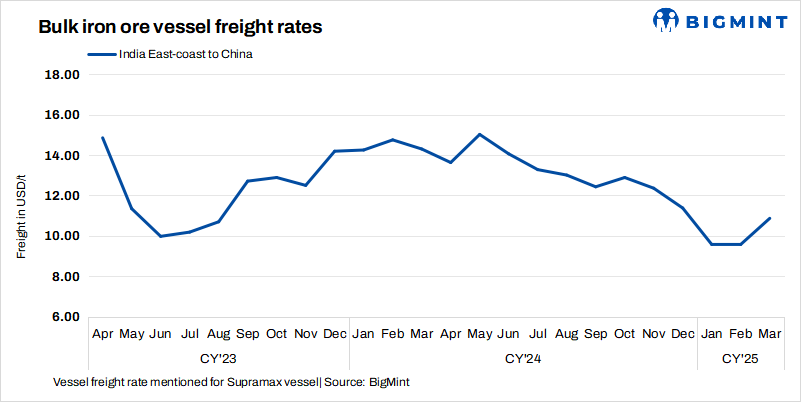

- India-China: Freights from the Indian Ocean to China were recorded at $10.9/t, inching up by $0.2/t w-o-w. Tightening vessel availability due to stronger demand in key markets supported freights.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $10/t on 19 March, edging up by $0.1/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP, and FMG were seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $9.75-10.80/t. Shipment is scheduled for 27 March-5 April.

- Brazil-China: Freights for Capesize vessels from Brazil to China climbed up this week. Rates from Tubarao to Qingdao Port were assessed at $24/t on 19 March, rose by $1.30/t w-o-w. As per sources, Bunge and Mercuria booked a Capesize vessel from Tubarao to Qingdao at around $24.25-24.75/t, with shipment scheduled for 11-20 April.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port increased by $1.30/t w-o-w to $17.9/t. Sources informed BigMint that one Capesize vessel from Saldanha Bay to Qingdao was booked at around $17.55/t, with shipment scheduled for 7-11 April.

Leave a Reply