- Vessel availability on Indian east coast tightens

- Australian miners rush to clear stocks before FY-end

Dry bulk iron ore freights climbed up on various routes, amid active fixtures and strong trade momentum. Freights from the Indian Ocean to China witnessed an increase this week amid pre-monsoon restocking demand by Chinese steel mills, which drove up cargo volumes due to concerns over seasonal weather disruptions. Additionally, tightening vessel availability on the Indian east coast pushed up freights. Despite overall soft sentiment globally, the regional surge in cargo activity, combined with limited spot tonnage on the India-China route, supported the upward movement in freights.

The increase in iron ore Capesize vessel freights can primarily be attributed to a surge in cargo supply driven by Western Australian miners rushing to clear inventories and boost revenue before the financial year-end on 30 June. Key mining companies such as Rio Tinto and FMG were actively fixing vessels at higher rates for mid to late June laycans.

Another factor fuelling the rate hike was vessel owners’ shift in focus from the Atlantic to the Pacific market, as the latter offered higher time-charter equivalent (TCE) earnings on shorter hauls. This tightened vessel supply in the Pacific basin, increasing competition among charterers and raising spot freights. Although Capesize forward freight agreements lost some momentum during Asian trading hours, the physical market was buoyed by the rapid uptake of vessels, further driving up rates.

Additionally, while the Atlantic market remains mixed – with some tightness in supply for late June to early July and others pointing to a more balanced tonnage list – the recent freight surge from Tubarao to Qingdao temporarily spiked market sentiment. However, the momentum did not fully carry forward, with some suggesting the uptick was driven more by sentiment than sustained demand.

Factors influencing freights

- Baltic indices shows mixed trend w-o-w: The Baltic indices, indicating trends in vessel demand, exhibited mixed trends. The Baltic Dry Index (BDI) was recorded at 1,418 on 2 June, increasing by 78 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,277, up by 377 points w-o-w. However, the Baltic Supramax Index (BSI) inched down w-o-w by 32 points w-o-w to 951 points.

- China’s iron ore spot prices dip $1/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $95.35/t CFR on 3 June, down by $1/t w-o-w. The drop was driven by mills prioritising margin preservation and opting for mid-grade blend optimisation. Restocking remained limited to need-only purchases, while falling port stocks fuelled expectations of a near-term rise in lump premiums.

Route-wise updates

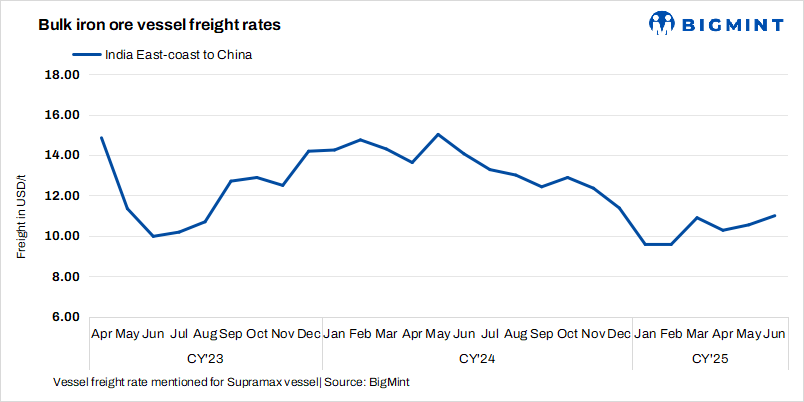

- India-China: Freights from the Indian Ocean to China were recorded at $11/tonne (t), edging up by $0.4/t w-o-w. Sources pointed to a recent Supramax fixture at around $9.8/t for a prompt laycan of 9-12 June. Several other fixtures were under negotiation, reflecting sustained activity and a strengthening sentiment in the region.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $9.1/t on 21 May, rising by $0.7/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP, and FMG booked Capesize vessels from a Western Australian port to Qingdao at around $8.35-9.25/t. Shipment is scheduled for 15-22 June.

- Brazil-China: Freights for Capesize vessels from Brazil to China fell this week. Rates from Tubarao to Qingdao Port were assessed at $22/t on 4 June, up sharply by $3.3/t w-o-w. As per sources, Vale, Panocean, and Element booked a Capesize vessel from Tubarao to Qingdao at $19.15-22/t for a shipment period of 18-28 June.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao increased by $1.5/t w-o-w to $15.9/t on 4 June. Sources informed BigMint that increased competition for prompt tonnage helped push rates higher.

Leave a Reply