- Capesize strength lifts iron ore freight market

- Active restocking ahead of winter supports freight rates

Iron ore freight sentiment strengthened this week, supported by firmer vessel demand and improving market activity. Capesize freights on key routes – Australia-China, Brazil-China, and South Africa-China – edged higher amid active chartering, limited vessel availability, and steady iron ore flows to China ahead of winter restocking.

Meanwhile, the India-China Supramax route held steady, with regional demand remaining in balance with available tonnage. Overall, gains on long-haul Capesize routes underscore improving dry bulk market sentiment and sustained Chinese import demand driving vessel utilisation.

A major Indian steelmaker said, “The market appears quite dull at the moment. Export activity seems uncertain, but it’s clear that the supply of higher-grade iron ore is noticeably tighter compared to last year, particularly since around April-May 2025.”

Meanwhile, FFA rates firmed this week in line with stronger spot market trends, supported by active chartering and tighter vessel supply. Key contracts saw modest gains amid steady iron ore exports and winter restocking demand. Meanwhile, Supramax FFAs were largely stable, reflecting subdued physical market activity. Overall, forward sentiment in the dry bulk market remains cautiously bullish, led by the Capesize segment.

However, bunker fuel prices edged higher this week, adding mild upward pressure on voyage costs and freight rates. The uptick was driven by steady crude oil prices and firm demand for marine fuels in key bunkering hubs such as Singapore and Fujairah.

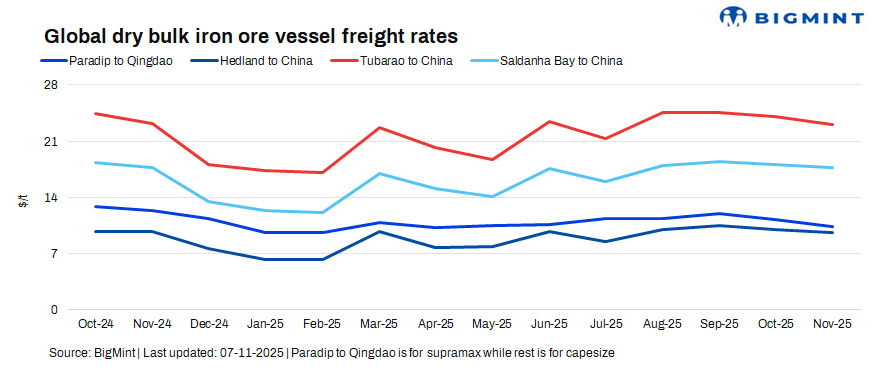

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China remained stable at $10.50/dry metric tonne (dmt) on 7 November against 29 October.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China increased by $0.8/dmt to $10.1/dmt, supported by active chartering from major miners such as BHP and Rio Tinto. The surge in fixtures tightened prompt tonnage availability, giving vessel owners stronger negotiating leverage.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments rose by $0.7/dmt to $23.2/dmt, supported by steady export activity and firm chartering demand. The long voyage continues to boost tonne-mile utilisation, while sustained Chinese restocking ahead of winter added further strength to the route.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao rose by $0.8/dmt to $17.8/dmt, supported by tight vessel supply and port-related delays in South Africa. Steady Chinese demand for medium-grade ore further underpinned rates despite limited fixture activity.

Market highlights

- Baltic index continues to surge on strong demand: The Baltic Exchange’s main dry bulk sea freight index strengthened this week as rates firmed across the larger vessel segments. As of 6 November, the overall index climbed by about 80 points w-o-w to 2,063. The Capesize segment led the gains, surging 297 points to 3,242, while the Panamax segment edged lower by 32 points to 1,817.

- Brent crude oil futures edge higher w-o-w: Brent crude oil futures increased by about $0.33/barrel (bbl) w-o-w to $64.07/bbl on 7 November 2025. A modest uptick in oil prices was driven by short-term supply concerns and geopolitical risk, which briefly outweighed demand weakness. US crude inventories rose more than expected, but the market took encouragement from disruptions and tighter supply signals.

Outlook

The near-term outlook for the dry bulk iron ore freight market remains firm, supported by steady Chinese restocking and strong export activity from Australia and Brazil. Tight vessel supply and rising bunker costs may keep rates elevated, with seasonal congestion adding mild upward pressure. However, slower winter steel output in China and broader economic uncertainties could limit gains. Overall, sentiment stays cautiously bullish, led by strength in the Capesize segment.

Leave a Reply