- Improved fixture flow, fresh cargo releases lift Capesize rates

- Supramax rates fall on ample tonnage supply, muted demand

Dry bulk iron ore freight rates showed a mixed trend across major routes during the week, driven by improving Capesize fundamentals and softer Supramax performance. Capesize freights strengthened across all key routes, including Brazil-China, West Australia-China, and South Africa-China, supported by post-Lunar New Year cargo enquiries and improved vessel absorption in major loading regions.

In contrast, Supramax rates from the Indian Ocean faced pressure, reflecting muted demand and comfortable tonnage availability. A ship-broker said, “Iron ore cargoes are scarce, with only 2-3 available in the market. Weak commodity rates are limiting exports, and although several traders hold cargoes, most remain unsold.”

Fixture activity remained moderate but improved w-o-w, with higher volumes supported by fresh cargo releases from major iron ore producers, particularly in the Pacific basin. However, chartering sentiment stayed cautious, limiting the pace of rate gains despite firmer Capesize fundamentals.

Macro factors continued to influence market behaviour, as Chinese steel margins remained under pressure and near-term construction demand stayed uncertain, prompting charterers to remain selective and capping upside potential.

Iron ore exports from major producers remained steady, with improved spot market activity helping absorb available Capesize tonnage. Meanwhile, the pace of ballasting into key loading regions slowed, leading to a more balanced tonnage list, especially in the Pacific. Despite this, ample vessel availability in the Supramax segments continued to weigh on rates.

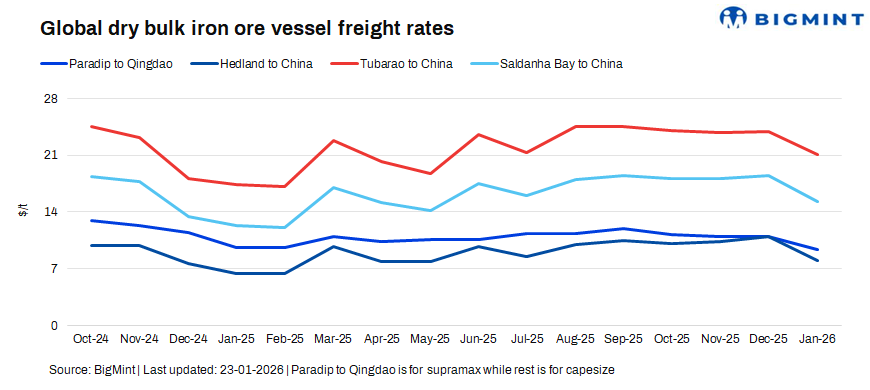

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China fell by $0.1/dry metric tonne (dmt) w-o-w to $9/dmt on 23 January.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China increased by $1.4/dmt w-o-w to $8.6/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil-China iron ore shipments surged by $2.6/dmt w-o-w to $21.8/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao were up by $1.6/dmt w-o-w to $15.5/dmt.

Market highlights

- Baltic index rallies w-o-w on improved bulk cargo demand: The Baltic Dry Index surged by 229 points w-o-w to 1,761 on 22 January, supported by improved Capesize and Panamax earnings amid increased iron ore and grain cargo activity, coupled with tighter vessel availability in key trading basins.

- Brent crude futures rise w-o-w: Brent crude oil futures edged up by around $0.7/bbl w-o-w to $65.2/bbl for the March 2026 contract on 23 January, supported by expectations of tighter supply and rising demand.

- DCE iron ore futures slide w-o-w amid weak steel fundamentals: Iron ore futures on the Dalian Commodity Exchange dropped by RMB 17/t ($2.44) w-o-w to RMB 795/t ($114/t) on 23 January, weighed down by weaker steel margins, subdued downstream demand, and expectations of stable near-term port inventories.

Outlook

Iron ore freight rates are expected to stay largely stable in the near term. Steady exports from major producers are balanced by ample vessel availability and cautious chartering. While post-holiday cargo enquiries may provide some support, weaker Chinese steel margins and uncertain construction demand are likely to limit any significant upside, with few fixtures reported at softer levels later in the week.

Leave a Reply