- Chartering activity picks up amid steady iron ore demand

- Falling Brent crude futures, ample vessel supply raise concerns

Dry bulk iron ore freights rallied across key global routes this week, reversing the decline seen in the previous period. The recovery was supported by stronger market activity, with increased chartering interest and firm tonnage demand from major exporting regions.

Capesize freights in the Pacific basin recorded gains this week, as positive momentum carried over from earlier sessions. A surge in fixing activity, especially on the Western Australia-China iron ore route, supported the uptrend. Increased chartering interest and active market participation added further strength to the segment, keeping sentiment supportive throughout the week. Adding to the upbeat market sentiment, a source told BigMint, “Freights rose this week, with many new orders entering the market.”

Iron ore demand in the Pacific also remained steady, underpinned by healthy shipment requirements from key producers. All three major Western Australia miners — Rio Tinto, BHP, and FMG — were in the market seeking tonnage for end-August 2025 laycans, indicating sustained export volumes. This steady flow of cargo inquiries continued to lend firm support to Capesize employment in the region, reinforcing expectations of stable activity in the near term.

In the Atlantic basin, too, market fundamentals continued to favour shipowners, supported by steady demand on the Brazil-China route. Interest was particularly strong for standard Capesize vessels, with a notable list of cargoes lined up for September loadings, ensuring healthy volumes in the weeks ahead.

Meanwhile, the Supramax market also witnessed a decent positive trend this week, particularly on the India-China route. “The India-China route saw a slight uptick in rates, reflecting improved activity. However, bunker prices fell today, which could offer some cost relief for operators,” a source told BigMint.

Another source noted, “Paper markets jumped on strong short-term buying, with September seeing the biggest gains. Prices for later months also went up, mainly due to positive sentiment rather than new cargo demand. There were more fixtures than last week, and forward freight agreement (FFA) rates also increased.“

Route-wise updates

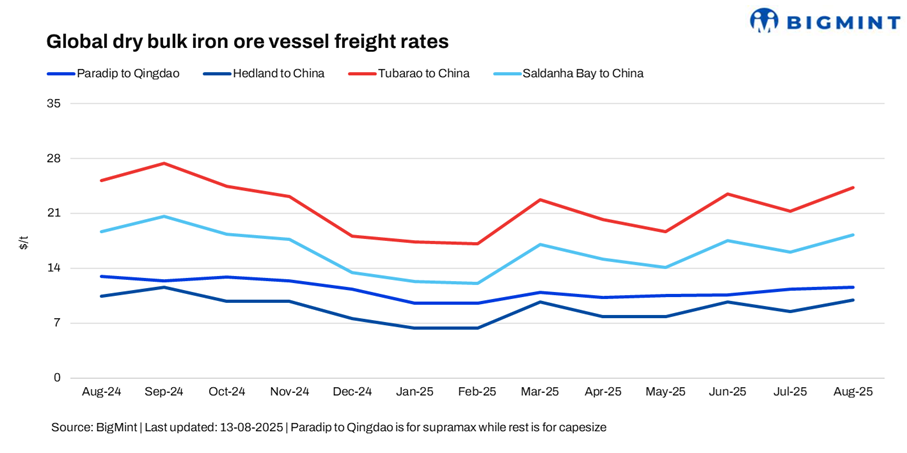

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China inched up by $0.2/dry metric tonne (dmt) w-o-w to $11.70/dmt. However, persistent monsoon rains disrupted mining and dispatch activities, driving up domestic prices and making exports less feasible. Many Indian exporters with available cargo held back, anticipating a potential price recovery before proceeding with shipments. Meanwhile, a few indicatives were also heard at higher levels of around $13/dmt.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China rose by $0.25/dmt w-o-w to $10.05/dmt. The uptick was attributed to active chartering by major Australian miners, including Rio Tinto, BHP, and FMG, which fixed vessels to Qingdao at rates between $9.95-10.6/dmt for end-August 2025 laycans. This surge in activity led to a tightening of available tonnage, sources informed BigMint.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments rose significantly by $0.98/dmt w-o-w, settling at $24.78/DMT. Three fixtures were reported on the Tubarao-Qingdao route, concluded in the range of $24.10-24.65/dmt, all for laycans in the first week of September 2025. According to sources, the market firmed up, with stronger fixture levels emerging after a recent soft spell.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao also increased by $1.1/dmt w-o-w, settling at $18.8/dmt. The uptick was partly driven by a fixture concluded yesterday by Anglo American at a higher level of $18.75/dmt.

Market highlights

- Baltic index posts w-o-w recovery: The Baltic Exchange’s main sea freight index, which tracks rates for dry bulk carriers, increased w-o-w on 12 August 2025, driven by strong demand across all vessel segments. The overall index went up by 96 points w-o-w to 2,017, with the Capesize index witnessing a noticeable increase of 255 points w-o-w to 3,261. Meanwhile, the Supramax index also increased by 50 points w-o-w to 1,329.

- China’s iron ore spot prices up $2/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $104/tonne (t) CFR China on 12 August 2025, a hike of $2/t w-o-w. The uptrend was fuelled by active trading due to the 90-day US-China tariff extension. Firmer steel prices also lifted iron ore tags. Meanwhile, port-stock prices also climbed up with coking coal’s rally, though high rates kept liquidity thin as mills bought only when needed.

- DCE iron ore futures stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract remained unchanged w-o-w at RMB 795/t ($111/t) on 13 August 2025. By mid-week, market indicators showed a slight pick-up in activity. Declining finished steel inventories, stabilising steel production, and higher iron ore imports suggested that mills had begun restocking. These factors helped limit further price declines and offered some support to the market.

However, oil prices declined after the International Energy Agency (IEA) projected that supply would outpace demand this year, while investors looked ahead to Friday’s meeting between the US and Russian presidents. Reflecting the weaker sentiment, Brent crude futures fell by $0.45/barrel (bbl) w-o-w to $65.67/bbl on 12 August 2025, sparking concern among market participants.

Outlook

The dry bulk iron ore freight market faces an uncertain outlook in the near term as some Capesize vessels from Australia started getting fixed at comparatively lower rates by mid-week. Market sources highlighted sluggish conditions, with sentiment easing despite freight derivatives remaining slightly positive. According to BigMint, Pacific tonnage supply stayed abundant, with more shipowners circulating vessels, suggesting that prolonged healthy supply could continue to pressure the market downward.

Leave a Reply