- Vessel shortage seen in Indian Ocean due to holiday disruption

- Higher bunker fuel costs add to voyage expenses

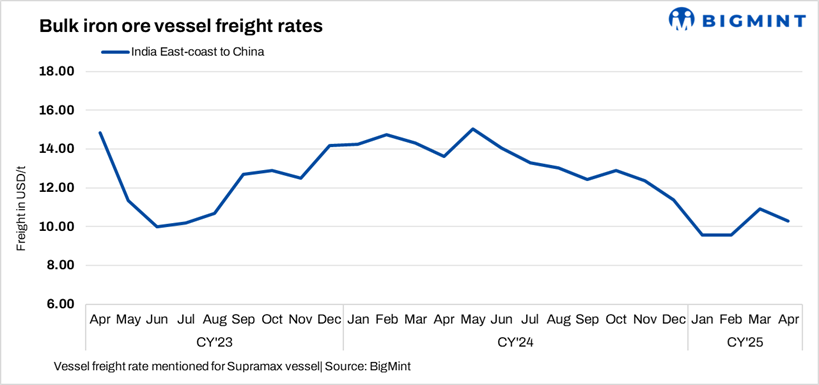

Dry bulk iron ore freights from India to China witnessed an uptrend this week, diverging from the overall mixed sentiment across global routes. This positive movement is largely attributed to a rebound in Chinese steel sector activity, with renewed demand for raw materials following the holiday period.

Moreover, limited vessel availability in the Indian Ocean region has contributed to this rate escalation. After the Easter holidays, particularly in the Atlantic and US Gulf, vessel circulation has been disrupted which has created a regional tonnage imbalance. With fewer prompt vessels in position, charterers moving iron ore from India to China are facing tightened supply, allowing shipowners to negotiate firmer rates.

“After the long Easter weekend when markets opened yesterday, freights rose as cargoes on the India-China route showed up,” a source informed.

Adding to this pressure, prevailing logistical inefficiencies and rising bunker fuel costs have inflated voyage expenses. As owners seek to offset these operational challenges, they are factoring these cost increases into their freight rate negotiations.

The decline in Capesize freight rates can primarily be attributed to subdued trading activity and weakening market sentiment, particularly in the Pacific. Despite a steady build-up in iron ore cargoes, the lack of trades and declining freight derivative values led to softer bids and offers.

China’s iron ore spot prices decrease by $1/t w-o-w: China’s spot prices of iron ore fines (Fe 62%) were assessed at $99.30/tonne (t) CFR on 22 April, down $1/t w-o-w amid weakening steel mill margins in China, which have reduced buying appetite for seaborne cargoes. With downstream steel prices under pressure and profitability shrinking, mills are showing limited interest in procuring high-grade iron ore, leading to subdued trading activity. Additionally, falling portside prices and cautious sentiment across the supply chain have further weighed on seaborne prices.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.6/tonne (t), up $1/t w-o-w primarily driven by higher bunker fuel costs. Despite the uptick in rates, fixture activity on the route remained relatively subdued, suggesting that the rate increase was cost-driven rather than demand-led.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $7/t on 23 April, a decrease of $0.7/t w-o-w. According to sources, major Australian miners Rio Tinto and FMG were seen actively booking Capesize vessels from a Western Australian port to Qingdao Port at around $7-7.25/t. Shipment is scheduled for 2 -10 May.

- Brazil-China: Freights for Capesize vessels from Brazil to China dipped this week. Rates from Tubarao to Qingdao were assessed at $18.7/t on 23 April, falling by $0.5/t w-o-w due to subdued market activity and excess vessel availability in the Atlantic. The Easter holidays delayed fixtures, while forward-dated cargoes reduced fixing urgency. As a result, charterers gained leverage, pressuring rates downward.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port dropped by $0.9/t w-o-w to $13.7/t. The absence of immediate demand and limited urgency from charterers to secure tonnage weighed on freights.

Leave a Reply