- BDI climbs to a one-month high on stronger Capesize demand

- Firm iron ore trade and tighter vessel supply support freight rates

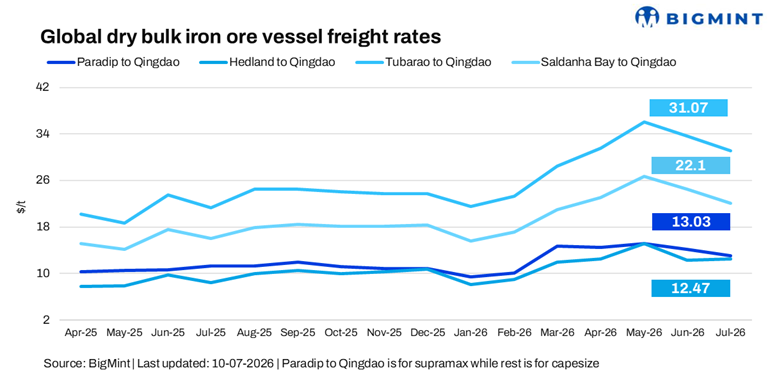

Dry bulk iron ore freight sentiment climbed in the week ended 10 July. Supramax freight rates rose on the Paradip-Qingdao route, underpinned by sustained cargo enquiries, healthy fixture volumes, and improved market sentiment.

Capesize market sentiment remained firm, supported by robust iron ore exports from Australia and Brazil and tight prompt vessel availability, which lifted freight rates w-o-w. However, limited fresh cargo enquiries, weaker freight derivatives (FFA) trading and typhoon-related disruptions at some Chinese ports capped further gains.

Route-wise update

Factors influencing freight rates

- Baltic Dry Index (BDI) reaches a one-month high: The BDI advanced 10% (260 points) w-o-w to 2,910 on 9 July, marking its highest level in a month. The rally was driven by a 17% (648 points) surge in the Capesize Index to 4,569, supported by miner participation, improving cargo enquiries, and tighter vessel availability across the Pacific and Atlantic basins. Meanwhile, the Supramax Index edged up 1% (25 points) w-o-w to 1,700, backed by steady demand for minor bulks and stable regional chartering activity.

- Brent crude futures gain w-o-w: Brent crude futures (September 2026 contract) gained $3.87/barrel (bbl) w-o-w to $76.65/bbl on 10 July, supported by renewed geopolitical tensions in the Middle East and concerns over potential supply disruptions through the Strait of Hormuz, despite expectations of adequate global oil supply.

- DCE iron ore futures surge w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) climbed RMB 17.5/tonne (t) w-o-w to RMB 751.5/t ($110.6/t) on 10 July, supported by expectations of stronger Chinese steel demand, resilient iron ore demand, and steel mill restocking, which boosted buying interest and strengthened seaborne market sentiment.

However, bunker prices fell by $9/t w-o-w to $652/t as of 10 July, pressured by softer crude oil prices and improved marine fuel availability across major bunkering hubs. Ongoing geopolitical tensions in the Middle East, however, continued to temper the decline by keeping market sentiment cautious.

Outlook

Dry bulk iron ore freight rates are expected to remain firm in the near term, supported by healthy iron ore export programmes from Australia and Brazil, steady cargo enquiries, and balanced vessel availability across key loading regions. Continued chartering activity and resilient Capesize demand are also likely to provide underlying support to market sentiment.

However, the pace of further gains may be influenced by fluctuations in Chinese steel production and iron ore demand, weather-related disruptions at major loading ports, and changes in FFA sentiment. Vessel supply dynamics, evolving trade flows, and broader macroeconomic developments will also remain key factors shaping freight market direction.

Leave a Reply