- Prolonged absence of fresh cargoes suppresses tonnage demand

- Market activity in the Atlantic remains largely subdued

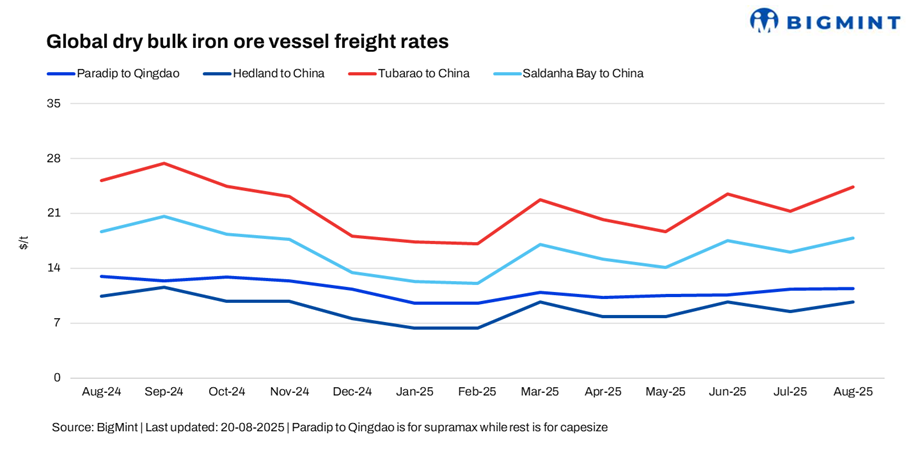

Dry bulk iron ore freight rates weakened across major global routes this week, weighed down by muted market activity, reduced chartering demand, and fewer fixtures.

Capesize freight rates came under pressure, weighed down by persistent bearish sentiment as freight derivative contracts witnessed a downtrend through the Asian trading session. Market participants noted that the weakness largely carried over since the beginning of this week when activity levels were subdued and the pace of exchanges slowed considerably. With comparatively lower number of fixtures against last week, shipowners and charterers alike faced limited opportunities, keeping sentiment fragile and discouraging fresh fixtures.

Adding to the pressure, cargo volumes out of both the Pacific and Atlantic basins remained thin, offering little support to freight rates. Market sources remarked that confidence among participants was visibly eroded, as hopes of a rebound were undermined by the lack of new demand.

“The absence of significant drivers in either basin meant there were few bright spots to offset the prevailing downtrend, leaving rates vulnerable to further downward pressure in the near term”, mentioned a source.

The Supramax market remained under pressure this week, with sluggish sentiment particularly evident on the India–China route. Another source said, “A meaningful recovery in Chinese iron ore demand could take several years, given the current economic scenario. Adding to the weakness, the ongoing monsoon season continued to disrupt trading activity, and sources suggested that the outlook may not show much improvement even after the monsoon period ends.”

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China inched down by $0.7/dry metric tonne (dmt) w-o-w to $11/dmt. However, persistent monsoon rains disrupted mining and dispatch activities, driving up domestic prices and making exports less feasible.Demand remained moderate but eased compared to the previous week, as buyers mostly limited their purchases to covering immediate needs.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China fell by $0.75/dmt w-o-w to $9.3/dmt. During Asian trading hours, Rio Tinto was reported to be the only iron ore miner from Western Australia reported to be in the market seeking tonnage. Capesize offers on the Australia-China route opened the week at relatively high levels of around $10.40/dmt. However, as the week progressed, offers gradually softened to about $9.85/dmt, with indicative bids remaining below prevailing offer levels. Sources noted that bearish sentiment continued to weigh on the market, driving offers further down. By late Asian trading hours, Rio Tinto was reported to have fixed a Capesize vessel from Dampier to Qingdao at around $9.15/dmt for 3–5 September 2015 laycans.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments decreased by $0.28/dmt w-o-w, settling at $24.5/dmt. On the Tubarao to Qingdao route, only two fixtures were reported this week. The first was concluded at around $24.75/dmt early in the week, followed by a second at a slightly lower level of about $24.50/dmt. According to sources, cargo volumes out of Brazil declined further amid a shortage of fresh requirements, while trading activity remained lackluster through much of the Asian session.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao also decreased sharply by $1.82/dmt w-o-w, settling at $16.98/dmt. A South Africa to China fixture was reportedly concluded at lower levels of around $16.98/dmt, further weighing on overall market sentiment.

Market highlights

- Baltic index drops w-o-w: Baltic Exchange’s main dry bulk sea freight index declined w-o-w on 19 August, primarily due to sharp losses in the Capesize segment. The overall index slipped 53 points to 1,964, with the Capesize index plunging by 238 points to 3,023. In contrast, the Supramax segment showed some resilience, rising 40 points w-o-w to 1,369.

- China’s iron ore spot prices fall $3/t w-o-w: Chinese spot prices of iron ore fines (Fe62%) were assessed at $101/tonne (t) CFR China on 19 August, a decrease of $3/t w-o-w. Prices found support initially from active seaborne trading, though Chinese portside iron ore values eased amid thinner liquidity, with buying interest centered on medium-grade fines, which weighed on spot levels. Meanwhile, adequate port inventories, steady mill margins, and tight pellet availability helped sustain lump premiums.

- DCE iron ore futures head south w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract witnessed downtrend w-o-w by RMB 26/t ($4/t)to RMB 769/t ($107/t) on 20 August. By mid-week, market indicators showed a slight pick-up in activity. DCE iron ore futures fell as comfortable seaborne supply and high Chinese port inventories coincide with weak steel demand from a sluggish property and construction sector, while limited policy support and bearish sentiment further weigh on market confidence.

Outlook

The near-term outlook for the dry bulk iron ore freight market remains uncertain, as several Capesize vessels from Australia continued to secure fixtures at relatively lower rates through the week. Market participants pointed to subdued conditions, with sentiment softening further on declining freight forward assessments (FFAs).

Leave a Reply