- No fresh fixtures in key routes

- Baltic Capesize index falls w-o-w

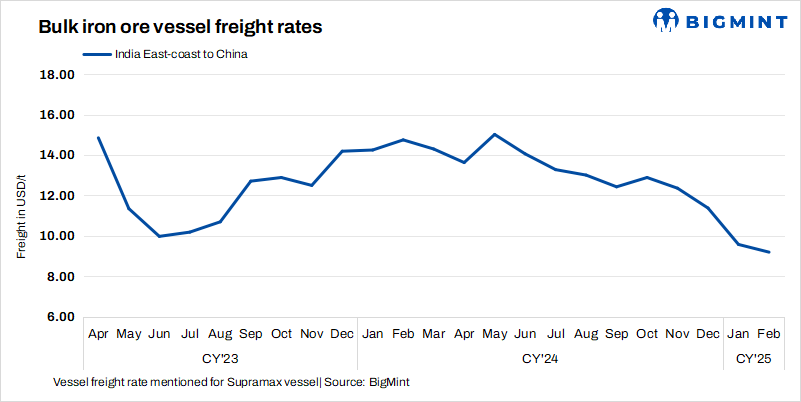

Dry bulk iron ore freights from India to China saw a slight uptick this week, as charterers rushed to secure cargoes on active fines and pellet export deals reported last week. Despite overall weak market sentiment and a general shortage of cargoes, this temporary surge in demand helped buoy rates. Additionally, many vessel owners were reluctant to fix their ships at lower rates, leading to tighter tonnage availability supporting freight levels. This combination of last-minute bookings and owners holding out for better returns contributed to the slight uptick in Supramax iron ore freight rates.

However, Capesize vessel freight rates have edged lower due due to limited fresh iron ore cargoes, particularly from Western Australia, where cyclones and heavy rains have disrupted mining operations and delayed shipments. In the Pacific, weak demand has kept fixing activity slow.

Factors influencing freights

- Baltic indices exhibit mixed trends w-o-w: The Baltic Dry Index (BDI) was recorded at 792 points on 17 February, decreasing by 23 points w-o-w. Meanwhile, the Baltic Capesize Index (BCI) stood at 716 points, dipped by 124 points w-o-w. However, the Baltic Supramax Index (BSI) rose by 88 points w-o-w to 765 points, reflecting an improvement in demand.

- China’s iron ore spot prices decrease by $1/t w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $107.60/t CFR on 18 February, down by $1/t w-o-w with cautious buying amid weak market fundamentals. Reports suggested that market conditions remained largely unchanged in the new trading week, with procurement activity lagging due to weak steel mill margins. Australian ports and mining operations are gradually resuming post-hurricane, but shipments are temporarily affected, leading to delayed vessel schedules.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10/t, up by 0.4/t w-o-w. Some fixtures for this route is under negotiation.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $6/t on 19 February, decreasing by $0.4/t w-o-w. According to sources, freight rates have fallen due to supply disruptions caused by cyclones and heavy rains in Western Australia, which have delayed loading schedules and reduced the availability of fresh cargoes. With fewer shipments, demand for Capesize vessels has weakened, leading to downward pressure on rates.

- Brazil-China: Freights for Capesize vessels from Brazil to China inched up this week. Rates from Tubarao to Qingdao Port were assessed at $17.10/t on 12 February, down by $0.1/t w-o-w. As per sources, the slow pace of fixing activity and an oversupply of available tonnage in the Atlantic have kept freight rates subdued. The market remains under pressure as there is insufficient fresh cargo from Brazil, and demand from Chinese steel mills remains cautious amid economic uncertainties.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port fell by $0.56/t w-o-w to $11.74/t. A combination of lower iron ore demand and increased vessel availability around the Chinese coast has weighed on South African shipments.

Leave a Reply