- Supramax remained firm, supported by active cargo discussions

- Major miners concluding fixtures at relatively lower levels

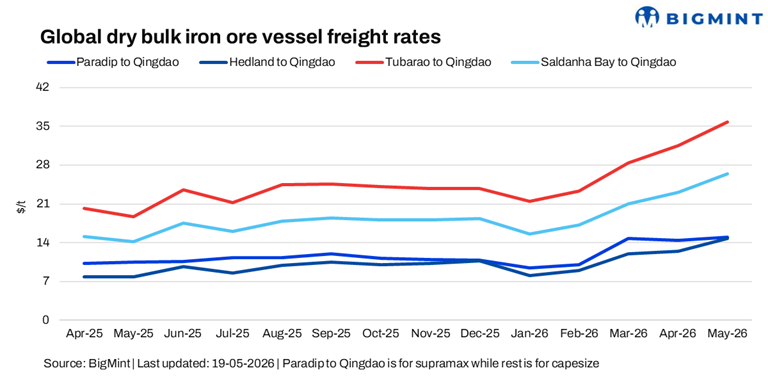

Dry bulk iron ore freight dynamics reflected a divergence between the Pacific and Atlantic basins. While Pacific rates softened amid miner-led pressure and ample vessel supply, Atlantic routes remained elevated due to longer-haul demand, geopolitical uncertainties, and sustained cargo flow. This imbalance continues to influence tonnage distribution and supports relatively stronger earnings potential for vessels positioned in the Atlantic basin.

Supramax sentiment remained firm this week, supported by steady cargo flow, rising bunker prices and ongoing negotiations on key routes. India-China route saw rates inch up w-o-w with several fixtures still under discussion. Market activity indicates underlying strength, as charterers continue to show interest while owners maintain a firm stance, anticipating further upside.

Capesize sentiment, however, showed a mixed-to-soft trend across major iron ore corridors. In the Pacific basin, shipments from Port Hedland to Qingdao declined, with major miners concluding fixtures at relatively lower levels. In contrast, the Atlantic basin remained comparatively stronger, driven by firm cargo volumes and tighter vessel availability.

“Capesize segment softened, while Panamax remained firm and Supramax and Handysize continued to hold steady. Market activity stayed limited, with several deals nearing conclusion but not yet fixed, as owners held back to gauge further market direction before committing,” a shipbroker mentioned.

Route-wise update

Outlook

Iron ore freights may remain uncertain in the near term, as mixed signals across basins and ongoing geopolitical factors continue to influence sentiment. While Atlantic strength may lend some support, softer Pacific activity and cautious chartering behavior could keep overall freight levels volatile.

Leave a Reply