- Pacific rates stay firm on firmer tonnage demand

- Inquiries drop in Atlantic basin with few fixtures at lower levels

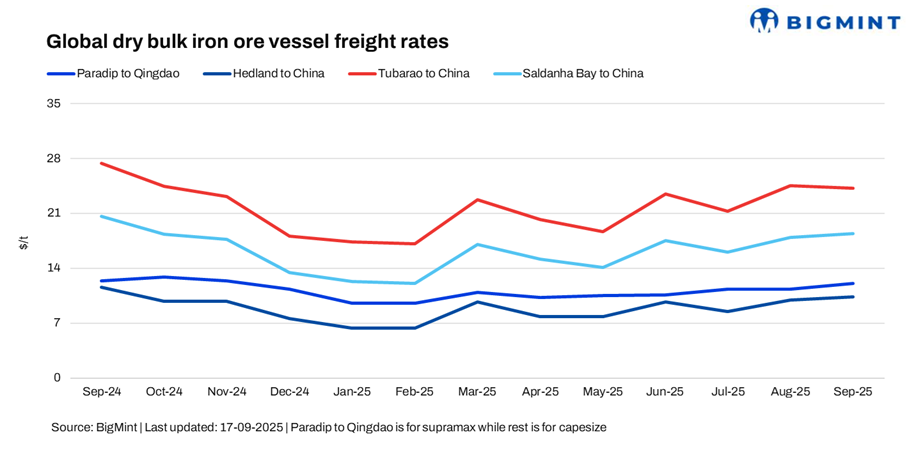

Dry bulk iron ore freight rates showed mixed movement this week, firming on Australia-China and India-China routes, while easing on Brazil-China and South Africa-China lanes, underscoring contrasting demand-supply dynamics across basins.

Positive sentiment in the Pacific basin strengthened on the back of rising cargo demand, while freight derivatives also posted healthy gains during Asian trading hours, according to sources.

In the Pacific, a surge in fresh iron ore orders from operators and traders continued to support market confidence. Additionally, Western Australia mining majors, including BHP and Rio Tinto, were actively seeking vessels through the week, further boosting tonnage demand.

However, Atlantic activity remained largely muted during Asian trading hours this week, with minimal fixtures reported. BigMint data indicates only one fixture each was recorded on the South Africa-China and Brazil-China routes.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed an increase w-o-w by $0.36/dry metric tonne (dmt) to $12.30/dmt. The market is firming as iron ore traders rush to sell and export cargoes following news of a potential 30% export duty on low-grade iron ore from early October, a Mumbai-based shipbroker told BigMint.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China continued to trend upward by $0.03/dmt w-o-w to $10.52/dmt. With fundamentals favouring sellers, shipowners initially quoted above $10.55/dmt on the Australia-China route. However, optimism faded in late Asian trading hours, with both bids and offers easing to around $10.20-10.40/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments, on contrary, witnessed a drop of $0.58/dmt w-o-w, settling at $23.84/dmt. On the Tubarao-Qingdao route, only one fixture was reported this week at around $24.25/dmt. The modest decline contrasts with firmer Pacific basin rates, underscoring divergent demand-supply dynamics across regions. Traders stayed cautious amid prevailing uncertainty, with fixture activity notably lower than the previous week.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao followed the suit and edged lower by $0.08/dmt w-o-w, settling at $18.38/dmt. Freight levels on the South Africa-China route moderated this week, with activity relatively subdued with only one fixture reported at around $17.68/dmt.

Market highlights

- Baltic index hits over 2-month high: The Baltic Exchange’s main dry bulk sea freight index rose further w-o-w on 17 September driven by higher rates across all vessel segments. The overall index increased around 75 points w-o-w to 2,154, with the Capesize index rising sharply by around 173 points w-o-w to 3,189. Additionally, the Supramax segment also increased by 18 points w-o-w to 1,491.

- DCE iron ore futures drop on supply concerns: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract increased marginally by around RMB 0.5/t ($0.1/t) to RMB 804.5/t ($113/t) on 17 September. DCE iron ore futures edged lower this week as weak steel mill demand, rising portside inventories, and cautious buying sentiment outweighed support from relatively steady seaborne cargo activity. Market participants noted that uncertainty around Chinese steel output controls and tepid downstream consumption further pressured futures.

Outlook

In the near term, dry bulk iron ore freight rates are likely to remain range-bound, with Pacific basin routes such as Australia–China and India–China supported by steady cargo flows and active chartering by miners. Sentiment may also draw some strength from derivative gains and sustained vessel demand in Asian trading hours.

Conversely, Atlantic basin routes, including Brazil-China and South Africa-China, could face continued pressure amid muted fixture activity and limited cargo availability. Overall, divergent regional dynamics are expected to keep the market mixed, with Pacific routes showing relative firmness while Atlantic routes remain subdued.

Leave a Reply