- Tight vessel supply, monsoon delays lift freights

- Baltic Panamax and Supramax indices rebound

Dry bulk coal freight rates to India strengthened across key routes this week. Panamax rates saw an uptick on both the Australia-India and South Africa-India routes, while Supramax rates on the Indonesia-India corridor also moved higher on a weekly basis. “A sudden uptick in Panamax activity was observed, driven by improved cargo movement out of ECSA. The market remained firm, with Panamax rates trending slightly higher as ECSA momentum continued to build”, told a source to BigMint.

Inquiries in the Asian thermal coal market remained steady, but limited trades were reported as miners held back low-priced cargoes, prompting buyers to adopt a more aggressive negotiation stance, sources informed.

Route-wise updates

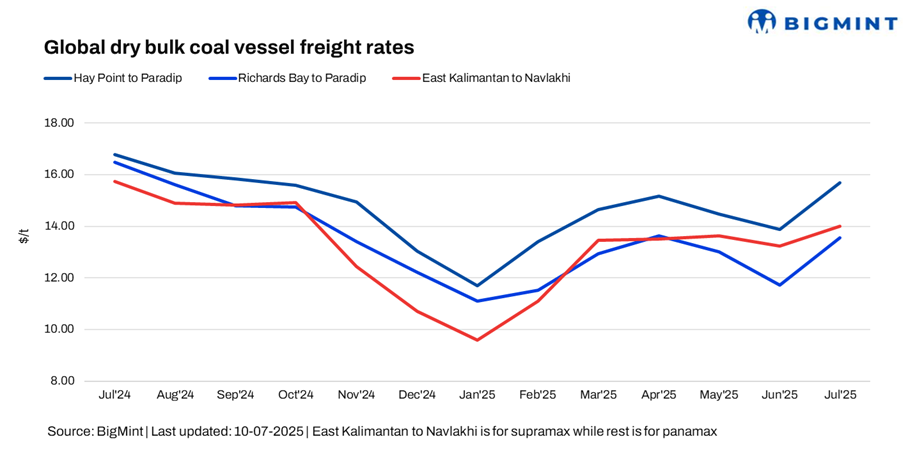

- Australia (Hay Point)-India (Paradip), Panamax: Freight rates from Australia to India increased by $0.8/dry metric tonne (DMT) w-o-w, with BigMint’s latest assessment placing the Hay Point to Paradip route at $16.10/DMT. Indian buyers, particularly blast furnace operators, increased coal procurement during the monsoon season to hedge against potential supply disruptions stemming from inland logistical bottlenecks and port congestion. This seasonal stockpiling boosted spot demand for Panamax vessels on the Australia-India route, as timely deliveries became a priority to maintain operations. Although coking coal prices remained relatively stable, heightened urgency to secure cargoes intensified competition for tonnage, pushing freight rates higher.

- South Africa (Richards Bay)-India (Paradip), Panamax: Freight rates from Richards Bay Coal Terminal (RBCT) to Paradip edged up slightly by $0.1/DMT w-o-w, reaching $13.60/DMT. Panamax freight rates for South African coal to India saw a marginal w-o-w increase. Market activity remained muted, with only need-based buying reported, while portside thermal coal inventories held steady, indicating limited demand. A key industry source noted, “Out of South Africa, trading information was scant,” reflecting the overall subdued sentiment in the market.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Coal freight rates from East Kalimantan to Navlakhi rose by $0.21/DMT w-o-w, settling at $14.11/DMT. Indonesian thermal coal demand remained muted, with the monsoon season continuing to dampen consumption from key sectors like cement and power generation. Buyers remained cautious amid steady portside inventories and elevated freight rates, driven by longer voyage times and weather-related disruptions. However, a steady rise in forward freight agreements (FFAs) led Indonesian miners to hold firm on their offer levels, pushing freight rates higher. As a result, “trading activity on the Indonesia-India coal route stayed limited,” mentioned a source to BigMint.

Another source said, “Indian buyers were reportedly exploring more cost-effective alternatives, including high-CV thermal coal from Mozambique. Around eight parcels are understood to be in the pipeline.”

Meanwhile, portside thermal coal inventories in India remained largely stable in Week 27, inching up to 15.92 million tonnes (mnt) from 15.86 mnt the previous week, as consistent arrivals kept pace with subdued demand. Among major ports, Paradip recorded a 7.4% w-o-w rise in stock levels, reaching 1.85 mnt from 1.73 mnt. This buildup contributed to reduced fixture activity for Indonesian coal bound for India.

Baltic Panamax, Supramax indices rebound

The Baltic Exchange’s dry bulk sea freight index saw a d-o-d rebound for both Panamax and Supramax vessels. The overall index, which tracks rates for Capesize, Panamax, and Supramax segments, rose by 42 points to 1,465. The Panamax index climbed by 102 points to 1,723, while the Supramax index increased by 31 points to 1,182, both on a d-o-d basis.

Outlook

In the near term, dry bulk coal freight rates are expected to remain firm to slightly bullish, supported by seasonal stockpiling in India during the monsoon, tighter vessel availability due to increased activity from regions like ECSA, and rising forward freight agreements (FFAs).

While demand from key sectors such as cement and power remains subdued due to the ongoing monsoon, stable portside inventories and weather-related delays are likely to keep vessel supply tight. As a result, Panamax rates on routes like Australia-India and South Africa-India may see moderate gains, while Supramax rates on the Indonesia-India corridor could remain steady to marginally higher.

Leave a Reply