- Pacific region freight rates remain steady

- Atlantic basin rates move higher despite lower fixtures

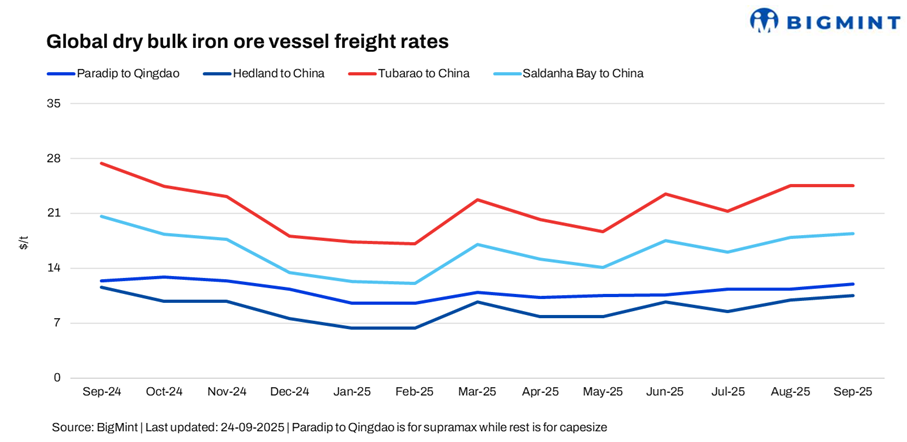

Dry bulk iron ore freight rates remained firm this week on the Australia-China, Brazil-China, and South Africa-China routes, supported by steady demand and limited tonnage. In contrast, rates on the India-China route edged lower, reflecting softer activity.

Capesize freight rates remained firm w-o-w. The Pacific region held steady amid balanced vessel demand and supply, while the Atlantic basin saw a modest uptick, despite very few fixtures.

Meanwhile, Supramax freight rates on the India-China route slipped amid uncertainty among market participants over a possible export duty imposition.

In the Pacific, iron ore mining majors from Western Australia were actively seeking tonnage, alongside multiple ship operators fixing vessels on the Australia–China route. The cargo list stayed firm overall, underpinned by solid iron ore demand out of Australia.

However, Atlantic activity remained largely muted during Asian trading hours this week, with minimal fixtures reported. BigMint data indicates only one fixture each was recorded on the Brazil-China route.

Route-wise updates

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed a decrease w-o-w of $0.58/dry metric tonne (dmt) to $11.72/dmt. “There is no government plan to impose export duty on low-grade materials; it was just a rumour,” a source told BigMint, shedding light on the export duty speculation.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China continued to trend upward by $0.27/dmt w-o-w to $10.79/dmt. With fundamentals tilting in favour of sellers, shipowners initially quoted above $10.8–11/dmt on the Australia–China route. However, sentiment softened in late Asian trading, with bids and offers easing to around $10.65/dmt before firming back up toward $10.80/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments also witnessed a significant increase of $1.56/dmt w-o-w, settling at $25.4/dmt. On the Tubarao-Qingdao route, only one fixture was reported this week at around $24.25/dmt. Despite limited fixture activity, Brazil–China freight rates edged higher as the route‘s long-haul nature kept vessels tied up for extended periods, tightening effective supply. Scarcity of tonnage in the Atlantic, coupled with costly ballast voyages from the Pacific, further supported owners‘ ability to command higher returns, while forward demand expectations added to the firming sentiment.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao followed the suit and edged higher by $0.12/dmt w-o-w, settling at $18.5/dmt. However, no new fixtures emerged from South Africa, reflecting muted activity in the region. Market participants noted limited cargo inquiries and a subdued chartering environment, with vessel availability outpacing demand and keeping sentiment soft on the South Africa–China iron ore route.

Market highlights

- Baltic index continues to head north: The Baltic Exchange’s main dry bulk sea freight index rose further w-o-w on 24 September driven by higher rates across capsize vessels. The overall index increased around 46 points w-o-w to 2,200, with the Capesize index rising sharply by around 280 points w-o-w to 3,469. However, the Supramax segment decreased by 5 points w-o-w to 1,486.

- DCE iron ore futures stay largely stable w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract decreased marginally by around RMB 1/t ($0.14/t) to RMB 803.5/t ($112.98/t) on 24 September. Iron ore futures on the DCE stayed largely stable w-o-w, with prices moving in a narrow range as balanced supply–demand dynamics kept market sentiment steady.

Outlook

Dry bulk iron ore freights are likely to stay supported in the near term, with steady shipments from Western Australia to China and balanced tonnage keeping Pacific routes firm, though daily volatility may persist with fixture flow.

Brazil–China rates may hold an upside bias as long-haul voyages tighten vessel supply, but gains could be capped by uneven Chinese demand and cautious chartering. Overall, the market is expected to remain firm yet rangebound.

Leave a Reply