- Tight supply keeps domestic prices elevated

- Uptrend continues with limited downside risk

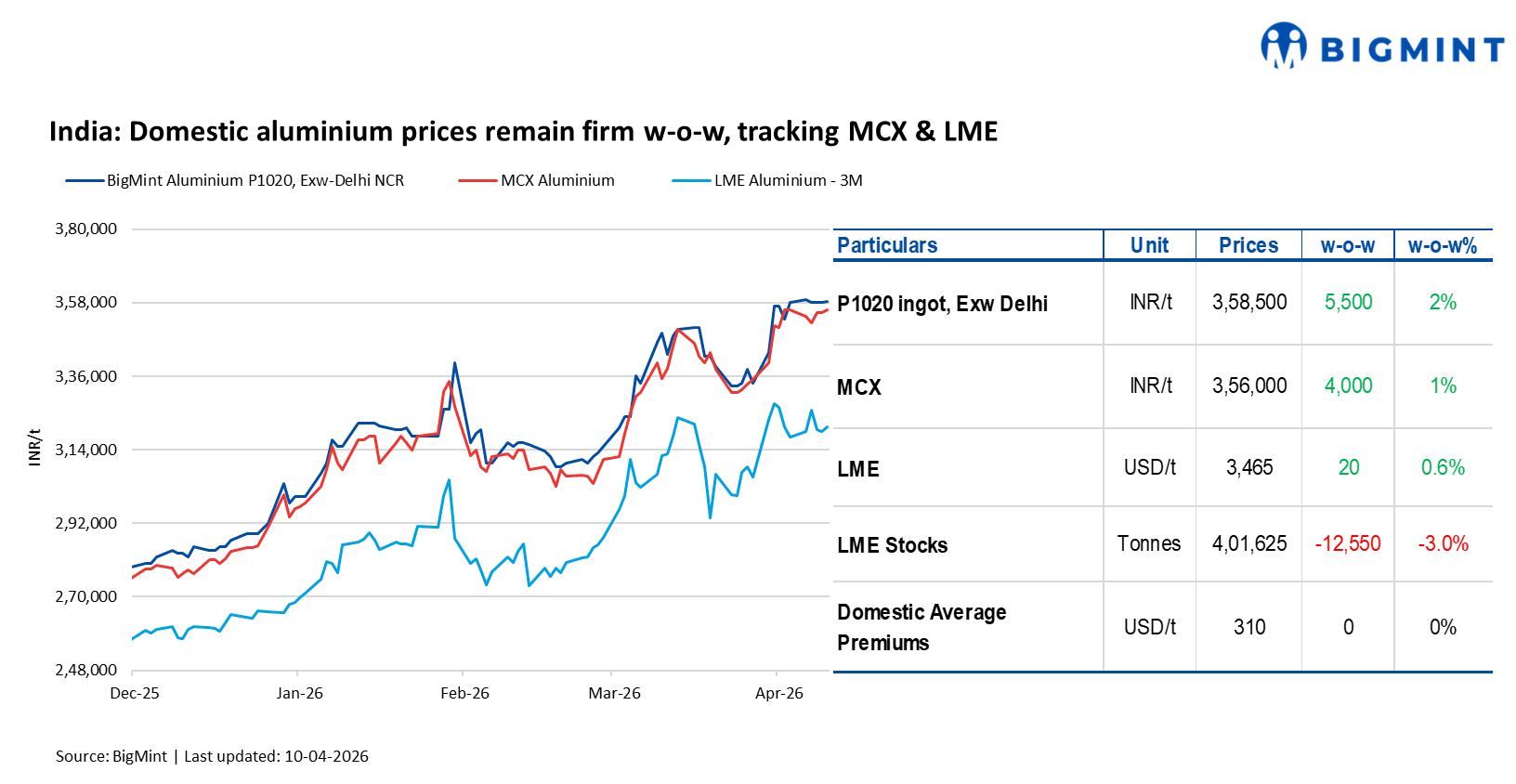

Domestic aluminium prices in India recorded a further w-o-w increase as of 10 April 2026, tracking continued gains in aluminium futures on the London Metal Exchange and Multi Commodity Exchange of India amid firm market sentiment.

As per market assessments, P1020 ingot prices in Delhi NCR rose by INR 5,500/t to INR 358,500/t on 10 April, up from INR 353,000/t on 2 April. Similarly, Mumbai prices increased by INR 5,000/t to INR 360,000/t, compared to INR 355,000/t in the previous week.

How did Indian, global exchanges perform?

Domestic aluminium futures on the Multi Commodity Exchange of India increased by INR 4,000/t, or around 1%, w-o-w to INR 356,000/t.

In the global market, 3-month aluminium prices on the London Metal Exchange edged up by $20/t, or 0.6%, to $3,450/t. Meanwhile, stocks at LME-registered warehouses declined by 12,550 t, or 3%, to 401,625 t, indicating continued supply tightness.

Aluminium prices slipped on Friday as a stronger US dollar and recession fears offset supply concerns from Middle East tensions. The market later remained closed on Friday and Monday for Good Friday and Easter holidays, while tighter global supply continued to support prices and boost prospects for Chinese exporters.

Market updates

A major primary producer reported that domestic P1020 aluminium premiums were assessed at $290-300/t, supported by steady supply conditions. Domestic demand remains moderate, though it has softened from March levels due to higher inventories and relatively slower production. Market participants noted that while material is consistently available, elevated prices continue to weigh on buying sentiment.

Reflecting the recent market correction, NALCO raised its primary aluminium ingot (P1020, 99.7%) prices by INR 8,500/t, or around 2.1%, from INR 396,750/t on 3 Apr’26 to INR 405,250/t on 8 April, indicating a firming trend in domestic aluminium prices over the week.

Meanwhile, BALCO’s average price levels increased by 2,542 t, or around 0.6%, rising to 391,208 t this week from 393,750 t in the previous week, while Hindalco’s average prices rose by INR 500/t, or around 0.1%, from INR 400,500/t to INR 401,000/t over the same period.

Asia aluminium premiums ease on weak demand

Aluminium premiums across Southeast Asia remained under pressure, with P1020 CIF Thailand levels assessed at $250-300/t, while CIF Vietnam premiums eased to $250-300/t from $305-355/t in March, reflecting softer regional demand and improved availability. At Port Klang, ex-warehouse offers were reported in the range of $200-250/t. Market sentiment stayed cautious as traders increasingly preferred regional sales due to elevated freight costs and logistical uncertainty linked to Middle East tensions, with shipping quotes valid only for short durations.

At the same time, high Asia-Europe freight rates of $170-220/t have eroded arbitrage opportunities, while adequate buyer inventories and subdued consumption have further weakened demand, collectively weighing on Asian aluminium premiums.

Outlook

Domestic aluminium prices in India are expected to remain firm in the near term, supported by higher futures on the Multi Commodity Exchange of India and global cues from the London Metal Exchange, along with tight supply conditions and steady producer pricing. However, moderate downstream demand, elevated price levels, and easing regional premiums may cap further upside, keeping the market stable with a slightly positive bias.

Leave a Reply