- LME base metals decline amid market weakness

- Oil rallies on escalating US-Iran tensions

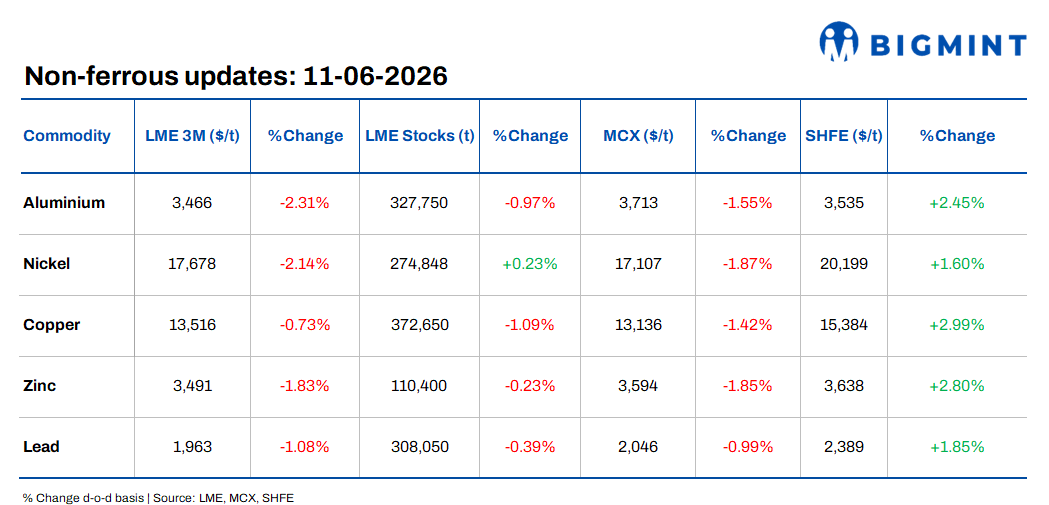

Base metals on the London Metal Exchange (LME) traded lower on 10 June 2026, reflecting continued weakness across the non-ferrous complex. Aluminium recorded the steepest decline among major base metals, falling 2.31% d-o-d to $3,466/t, followed by nickel, which dropped 2.14% to $17,678/t. Zinc declined 1.83% to $3,491/t, while lead and copper fell 1.08% and 0.73% to $1,963/t and $13,516/t, respectively.

On the inventory side, copper stocks registered the sharpest decline, falling 1.09% d-o-d to 372,650 t, followed by aluminium inventories, which decreased 0.97% to 327,750 t. Lead and zinc stocks also edged lower by 0.39% and 0.23% to 308,050 t and 110,400 t, respectively. In contrast, nickel inventories increased marginally by 0.23% to 274,848 t, indicating relatively stable warehouse availability despite broader market weakness.

Domestic market overview

India’s non-ferrous scrap prices remained largely stable on 11 June. Aluminium tense scrap (loose), ex-Delhi, held steady at INR 304,000/t, while ex-Chennai prices were also unchanged at INR 307,000/t, reflecting balanced market fundamentals and steady trading activity across key consumption centers.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, remained stable at INR 1,260,000/t with no d-o-d change, indicating a cautious market sentiment amid stable domestic demand and limited price movements in the physical scrap market.

Other updates

APAC smelters poised for strong margins

APAC aluminium smelters are expected to maintain strong margins as tightening global primary aluminium supply continues to support higher metal prices. Aluminium prices have risen nearly 20% since late February 2026 amid supply disruptions in the Middle East, boosting earnings prospects for regional producers. Smelters in China, India, and Indonesia are particularly well positioned due to integrated raw-material supply chains and relatively stable power costs.

Market fundamentals are likely to remain favorable as alumina costs have not increased at the same pace as aluminium prices, helping preserve profitability. Strong demand from electric vehicles and manufacturing sectors continues to support consumption, while restrictions on new smelting capacity in China and power constraints in Indonesia are limiting supply growth. These factors are expected to keep the aluminium market tight and support prices and margins in the near term.

Copper futures turn weak

Copper futures weakened after declining below the key support level of INR 1,012 on the MCX, indicating a bearish short-term trend. The contract closed at around INR 999.6, reflecting continued selling pressure and profit booking in the market. Technical indicators suggest that the near-term outlook remains weak unless prices recover above the resistance level of INR 1,012.

Despite the recent correction, broader market fundamentals remain supportive. Tight global copper supplies, declining exchange inventories, and concerns over mine disruptions continue to underpin long-term sentiment. Analysts indicate that copper futures could test the next support level near INR 975 if weakness persists, while a move above INR 1,012 may improve the price outlook.

Oil rises more than $1 as US-Iran tensions escalate

Global crude oil prices surged on 11 June as escalating tensions between the US and Iran intensified concerns over disruptions to global energy supplies. Brent crude futures rose 2.78% d-o-d to $93.64/bbl, while WTI crude gained 3.10% to $90.76/bbl after Iran declared the Strait of Hormuz closed following fresh US strikes on Iranian targets and renewed threats of further military action.

Concerns were further amplified by repeated violations of the fragile ceasefire, raising the risk of renewed escalation in the region. While traders continue to react to reports of potential peace negotiations, uncertainty over the timing of a lasting resolution has kept risk premiums elevated in oil markets.

Additional support came from tightening supply fundamentals, with US crude inventories falling by 7.2 mn barrels in the latest week and OPEC output declining to its lowest level in more than two decades. Analysts also highlighted growing concerns over tightening global inventories and the possibility that any reopening of the Strait of Hormuz may take weeks to translate into physical supply relief.

Leave a Reply