- If exporters rise, supply-demand balance may tighten further

- Demand resilience may support prices above structural base

India’s cumin market is gradually shifting into a tighter supply cycle after two years of sharp volatility. The extraordinary rally of 2023, followed by the correction in 2024-25, has led to acreage rationalisation. Everyone is now evaluating whether 2026 could mark the beginning of a fresh upward phase.

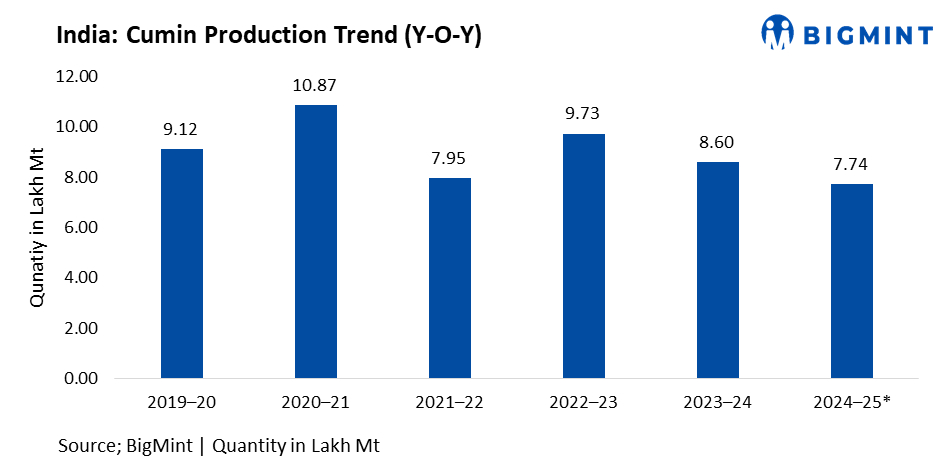

The key shift is visible in production. After prices surged in 2023, sowing expanded aggressively from the usual 7-8 lakh hectares to nearly 12-13 lakh hectares. Supported by favourable weather, output rose sharply to around 660,000-715,000 tonnes (t), creating a supply surplus and triggering a steep price correction. In 2024-25, acreage moderated but production still remained near 550,000 t, keeping pressure on prices and creating a stock overhang.

For the current season, sowing has declined meaningfully. Gujarat acreage is estimated at 30-35% lower, while Rajasthan is down 10-12%. Crop estimates now range between 412,500 t and 467,500 t. Gujarat output is projected around 121,000-165,000 t, while Rajasthan may contribute 275,000-302,500 t, depending on final yield outcomes. Carryover stock estimates range between 99,000 t and 137,500 t, although exact figures remain uncertain as substantial stocks remain in farmers’ hands.

On the demand side, annual consumption is estimated at 495,000-522,500 t, including 220,000-247,500 t of exports and about 275,000 t for domestic use. Even in a year perceived as weak for exports, shipments were estimated around 210,000 t. If exports rise toward 250,000 t, as some traders anticipate, the supply-demand balance may tighten further.

China remains key

China remains a key variable. Its annual consumption is estimated at 70,000-80,000 t. While China has expanded domestic production, yield outcomes remain weather-dependent. If Indian prices soften toward INR 21,000-22,000 per quintal, Chinese buying could re-emerge before its new harvest arrives in July-August. Meanwhile, Middle East demand has been steady but cautious, and global stocks are largely described as hand-to-mouth.

Price expectations suggest INR 19,000-21,000 per quintal as a strong structural support zone for 2026, with upside potential toward INR 26,000-30,000 depending on export momentum and monsoon developments. Compared with last year’s INR 18,000 base, INR 20,000 is increasingly viewed as the new structural floor.

Outlook

Going forward, two primary triggers will shape the market: China’s buying pattern and India’s monsoon outlook for the next sowing cycle. If monsoon concerns emerge or exports accelerate meaningfully, the market may transition from range-bound trade to a renewed upward trajectory. For now, the consensus favours accumulation on price dips rather than aggressive selling, as cumin appears to be entering a tighter and more balanced supply phase after two turbulent years.

Leave a Reply