- Rising imports restore parity for mills but tighten margins for ginners

- India’s cotton ecosystem aligns closer to global markets amid policy shift

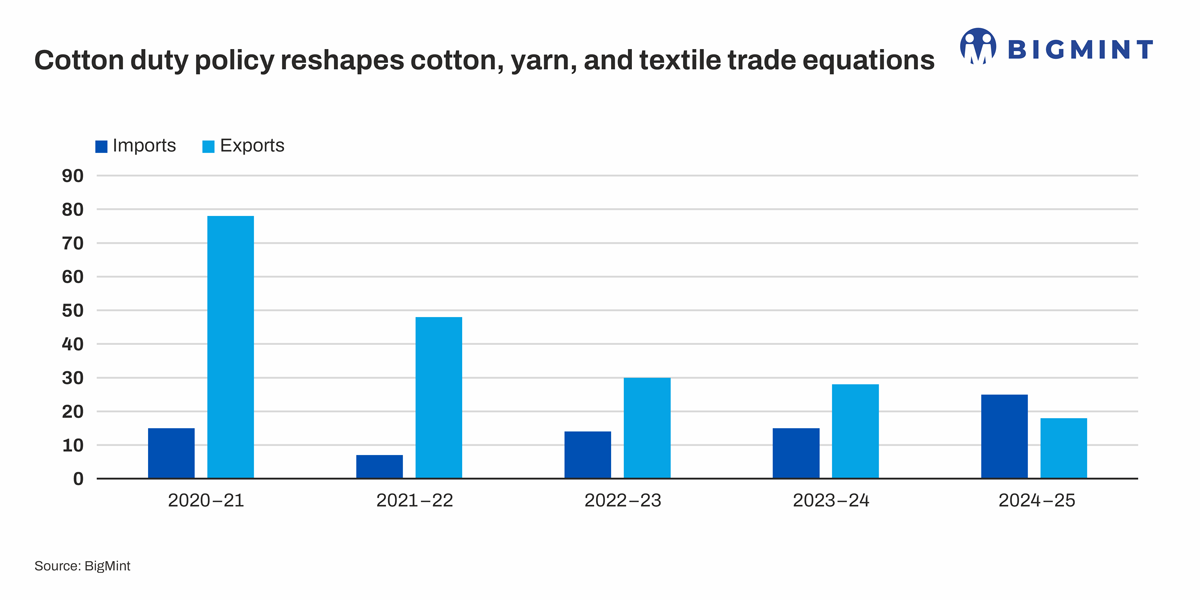

India’s cotton, cotton yarn, and textile trade dynamics have changed materially over the last five years, driven by declining domestic productivity, rising minimum support prices (MSPs), and changes in import duty policy. In 2020-21, India exported nearly 7.8 million bales of cotton and remained a dominant supplier to global markets. By contrast, in 2024-25, cotton exports fell sharply to around 1.8 million bales, while imports surged to an estimated 2.7 million bales, reflecting a clear shift from surplus to deficit conditions.

The 11% customs duty on cotton imports, introduced in 2021, was aimed at protecting domestic prices and farmer incomes. However, domestic production stagnated at around 30-31 million bales over recent seasons, while mill consumption stayed close to 31.5 million bales. Yield losses due to pink bollworm, erratic monsoons, and contamination issues widened the supply gap. At the same time, MSP for medium staple cotton rose steadily, pushing kapas prices higher. As a result, Indian cotton prices frequently traded 10-15% above international benchmarks, severely impacting spinning mill margins.

The impact was clearly visible in cotton yarn trade. India’s cotton yarn exports, which exceeded 4 million tonnes equivalent in earlier years, weakened as high raw material costs reduced competitiveness. Yarn exports declined steadily, while imports of fine-count and specialised yarns increased, particularly from Vietnam and other Asian suppliers. Textile and garment exporters also faced margin compression, losing orders to countries with cheaper cotton access such as Bangladesh and Vietnam.

The government’s decision to temporarily remove the 11% import duty in 2025 acknowledged this imbalance. Following the duty removal, spinning millers increased imports from the US, Brazil, and Africa, attracted by better fibre quality and price parity. Imported cotton landed at levels close to global prices, immediately capping domestic lint prices despite firm MSP-linked seed cotton rates. This helped mills stabilise operations and avoid deeper production cuts, even as global textile demand remained weak.

For India, the effects are mixed. Spinning millers benefit directly through lower raw material costs and improved quality consistency, supporting yarn and fabric output. Brokers expect higher trading volumes, increased arbitrage opportunities between domestic and imported cotton, and stronger liquidity across delivery periods. However, ginners face tighter margins as MSP creates a firm floor while imported cotton sets a ceiling on lint prices. Only high-quality, contamination-free cotton is able to command premiums.

Globally, India’s shift from exporter to importer has supported international cotton prices, strengthening exporters like the US and Brazil. India’s role in global cotton markets is evolving from a swing supplier to a significant buyer in deficit years, increasing its exposure to world price movements.

Leave a Reply