- Copper hits $11,660/t on 5 Dec, up 7% w-o-w amid tight supply and strong fund inflows

- Major mine disruptions and low inventories keep the market under pressure

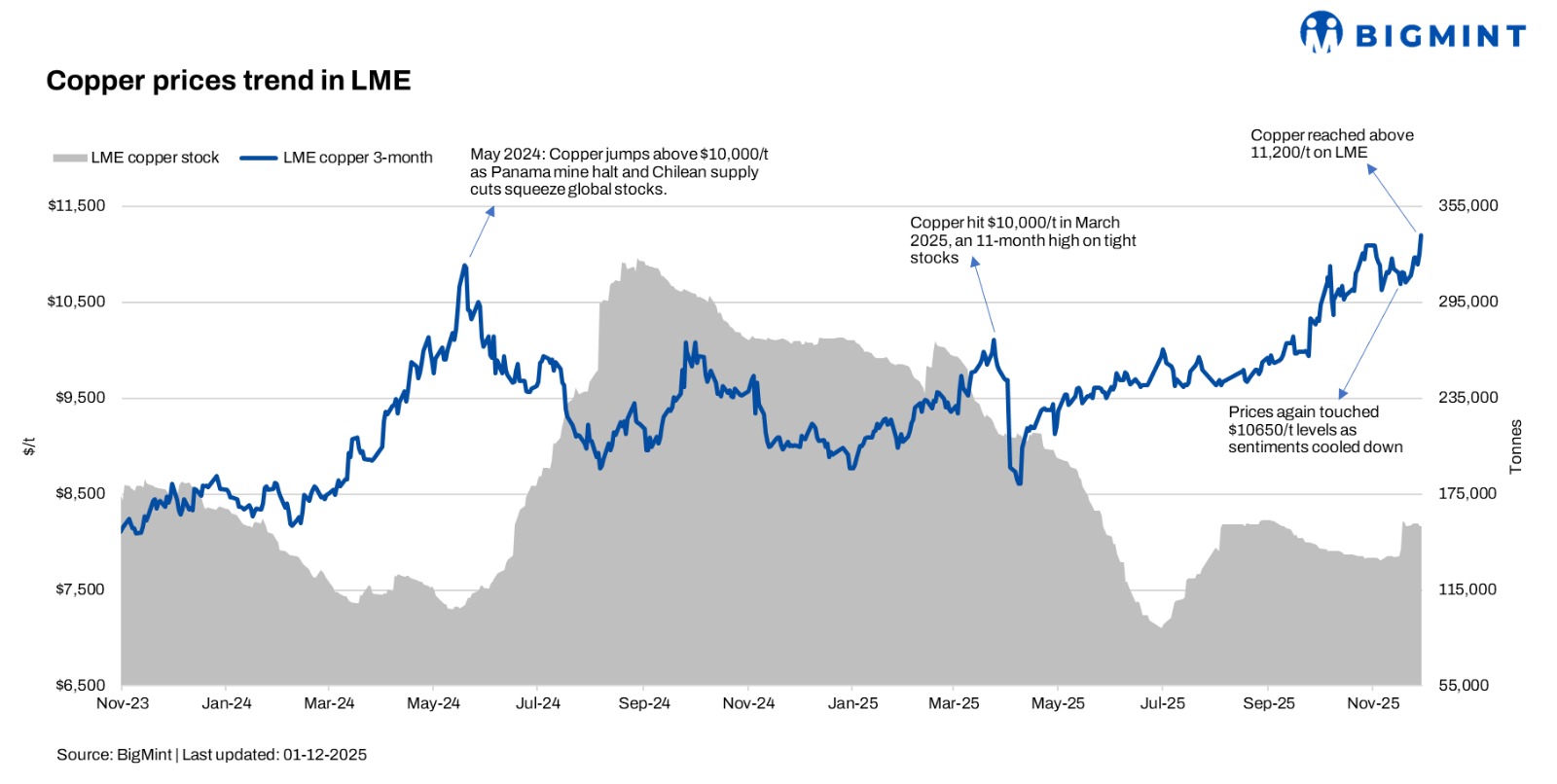

Copper prices rose sharply to $11,660/t on 5 December, up from $10,900/t on 28 November, registering a 7% w-o-w increase. The rally reflects tightening refined availability, stronger fund inflows, and a supportive macro environment.

As per reports, copper prices are surging, hitting record highs this week on both the London and Shanghai markets amid a growing supply crunch. Physical premiums are soaring as smelters face a shortage of mined concentrate, and LME stocks have fallen below 100,000 metric tons for the first time since July, highlighting tightening availability.

Supply-Side Developments

Global supply concerns regained traction as several major producers revised down output expectations heading into 2026. Operational challenges in key Latin American mines also heightened market anxiety around concentrate supply. Spot TCs, which had been signalling abundant concentrate, moderated slightly—pointing to renewed upstream tightening. The combination of refined scarcity and uncertainty in concentrates supported a bullish tone.

On the physical side, refined availability has been constrained by a combination of mine disruptions, weak concentrate supply, and margin pressure at smelters, particularly in China. Treatment and refining charges have been hovering at levels that make additional smelting uneconomic for some producers, prompting cutbacks.

Copper’s supply is under pressure from major disruptions at key mines. Freeport‑McMoRan’s Grasberg mine in Indonesia, one of the world’s largest, shut down after a fatal landslide in September 2025, cutting an estimated 600,000 tonnes of output through 2026. In Chile, Codelco’s El Teniente mine faced a tunnel collapse in July 2025, reducing production by 20,000–33,000 tonnes.

Smelters are also being squeezed by concentrate shortages. CRU Group forecasts a global deficit of about 1.1 million tonnes of copper‑in‑concentrate in 2025, forcing smaller smelters, especially in China, to cut output or idle capacity. These disruptions are driving premiums higher and tightening market availability.

Macro and Inventory Factors

A softer US dollar has mechanically boosted dollar‑denominated commodities, while recent data from major economies have pointed to stabilising or modestly improving manufacturing activity.

LME on-warrant copper inventories edged up to 159,000 t, from 156,000 t a week earlier, marking a +1.9% w-o-w increase. Despite this small build, stocks remain structurally low, keeping the physical market tight and reinforcing firm backwardation across nearby spreads. The modest rise did little to ease concerns over refined availability, as demand from Asia and Europe continues to absorb material faster than it is being replenished.

Price Forecast

Given these conditions, LME copper is expected to remain on a firmer trajectory over the next 2–4 weeks. Prices are likely to trade in the $11,500–$12,000/t range, with potential spikes toward $12,200/t.

Copper prices in 2026 are expected to stay firm, supported by strong structural demand and tightening medium-term supply, according to several major institutions. Goldman Sachs, Deutsche Bank, UBS, and J.P. Morgan Global Research have all highlighted a bullish multi-year setup driven by mine under-investment, rising consumption from EVs and renewable infrastructure, and persistent low inventories. Based on these institutional outlooks, the base-case expectation for 2026 places benchmark copper prices in the $11,500–12,200/t range, with a bullish scenario stretching up to $12,500–13,500/t if supply risks intensify or Chinese demand accelerates.

Leave a Reply