- Colombian operational and political risks continue to support Atlantic coal prices

- Soft European coal consumption may limit further price upside

European thermal coal prices have rallied sharply despite little evidence of a corresponding improvement in consumption. CIF ARA 6,000 NAR rose from approximately $128/t to $138.05/t between May 30 and June 1, a gain of more than $10/t in two trading sessions. Over the same period, FOB Colombia 6,000 NAR remained around $96/t, highlighting that the rally was driven primarily by concerns over supply availability rather than physical demand.

The immediate trigger was renewed uncertainty surrounding Cerrejón operations and Colombia’s presidential election, where right-wing candidate Abelardo de la Espriella unexpectedly emerged ahead after the first round of voting.

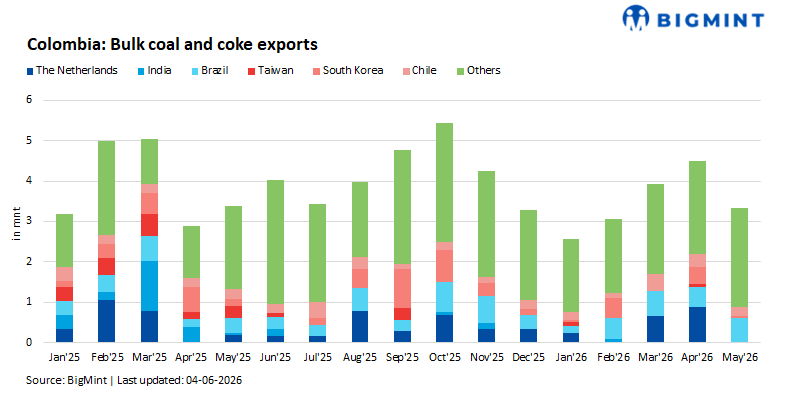

Colombia’s coal and coke shipments ease in May’26 as key export markets weaken

As per BigMint’s data, Colombia’s bulk coal and coke exports fell to 3.33 million tonnes (mnt) in May 2026, down 15.3% month-on-month (m-o-m) from 4.50 mnt in April and 1.4% year-on-year (y-o-y) from 3.38 mnt in May 2025. The decline was mainly driven by weaker shipments to South Korea and Chile, although higher exports to Brazil and other destinations provided partial support.

Cumulatively, exports during Jan-May 2026 stood at 17.4 mnt, down 11% y-o-y from 19.5 mnt recorded during the corresponding period in 2025.

Brazil became the largest export destination, with shipments rising 19.6% m-o-m and 61.2% y-o-y to 0.61 mnt, reflecting stronger import demand. Exports to South Korea dropped sharply to 0.06 mnt, down 85.7% m-o-m and 63% y-o-y, making it the primary factor behind the overall export decline. Chile-bound shipments also weakened, falling 37.5% m-o-m and 16.1% y-o-y to 0.20 mnt.

Meanwhile, exports to other destinations increased by 7% m-o-m and 19.5% y-o-y to 2.46 mnt, accounting for nearly 74% of total exports and highlighting the continued importance of diversified markets in supporting Colombian export volumes.

Operational disruptions have compounded the decline. Cerrejón experienced approximately 80 separate blockades during 2026 alone, following interruptions totalling 135 days in 2024 and 95 days in 2025.

Even minor disruptions therefore have an outsized impact on prompt European supply.

German demand continues to move in the opposite direction

While supply concerns have strengthened prices, demand fundamentals remain considerably weaker.

The most telling indicator is the widening gap between CIF ARA and the European Blended Price (EBP). On June 1, CIF ARA stood at $138.05/t, while EBP was only $114.55/t, creating a premium of $23.50/t.

This spread suggests the market is pricing a temporary supply risk rather than genuine demand strength. German utilities continue to favour lignite and increasingly competitive gas-fired generation whenever economics permit, limiting the upside for imported thermal coal.

Outlook

The current ARA rally appears to be driven primarily by political and operational risk rather than improving consumption. Unless European power demand strengthens materially, the market may struggle to sustain a premium of more than $20/t over broader European coal values. Colombia can continue to influence prompt pricing, but weak European coal burn suggests that any risk premium will ultimately face resistance from underlying demand fundamentals.

Leave a Reply