*CIL e-auction volumes touch 1-year high of 11 mnt

*Non-coking coal prices drop on higher production, supplies

*India’s coal inventory stable in Feb, but is it enough for peak summer?

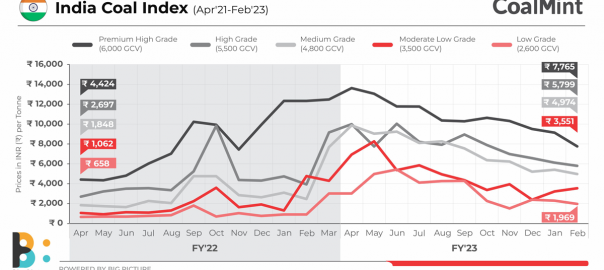

CoalMint’s India Coal Index (ICI) continued to head south in February 2023 on the back of robust domestic coal production and supplies and record coal allocations at e-auctions conducted by subsidiaries of Coal India Ltd. (CIL).

Total allocations at auctions during the month was recorded at a one-year high of 11 million tonnes (mnt), indicating a gradual return to normalcy in the domestic supply situation.

The ICI, set on a gross calorific value (GCV) basis, consists of five distinct indices formed by grouping the domestic non-coking coals from G1-G17 grades. Coal sales for these grade baskets are compiled against regular auctions conducted by State-run miner CIL.

In the aftermath of the Russia-Ukraine war, global coal supply chains had altered which resulted in prices touching record highs. This compelled the Indian government to take proactive measures to ensure adequate domestic coal availability as part of its energy security plan.

Incidentally, CIL had diverted additional production volumes towards sales against Fuel Supply Agreements (FSA), which refers to long-terms contracts initiated with the thermal power utilities.

On the other hand, allocations via e-auctions, which constitute 20% of CIL’s sales, were curtailed. In 2022, average bookings against the auctions on a monthly basis stood at 5.04 mnt as against 10.51 mnt in 2021.

However, CIL’s coal offerings at e-auctions have surged in February at a time coal prices in the international market have retreated from levels seen last year.

Auctions in Feb

In February, CIL’s coal production increased by 7% y-o-y to 68.77 mnt, as production rose to 2.46 mnt/day in the ongoing fiscal – the highest so far.

Higher production also led to inventory build-up at CIL mines, with levels rising to 50.5 mnt in end-February as against 27.09 in October last year. This provided CIL’s subsidiaries the opportunity to augment coal allocations for e-auctions.

In a significant development, all the subsidiaries conducted auctions during February. In particular, Mahanadi Coalfields (MCL) and South Eastern Coalfields (SECL) conducted auctions twice in February compared with only once a month as a general rule.

ICI extends fall

Under the impact of improved supplies, domestic coal prices continued on a downward trajectory, thereby shedding some of the spectacular gains that had resulted last year from supply tightness and global factors.

In February, the monthly weighted average price of all the indices, except for coal with moderate low specifications, declined m-o-m.

In particular, the grade basket comprising 3,500 GCV coal, attracted competitive bidding from power producers as they explored the e-auction route to accumulate additional volumes ahead of the peak summer season.

Overall, the ICI indices recorded a correction in the range of INR 4,000-6,000/t from the peaks witnessed in 2022.

Outlook

The oversupplied e-auction market contrasts with the government’s plan of ensuring adequate coal inventory at thermal power stations ahead of the peak summer season.

Towards the end of February, coal inventory was assessed almost stable at 33.65 mnt as against 33.13 mnt in end-January.

As per estimates of the Central Electricity Authority (CEA), peak electricity demand is expected to be 229 GW during April. Electricity demand was already the highest in February at 210 GW compared with anything seen in previous years.

It will be interesting to see whether CIL steps in to divert all supplies to the power sector to avert a possible crisis or the trend of higher allocations at auctions continues in the short term.

India Coal Index

The ICI is assessed on a monthly basis, as per the weighted average prices derived from the regular auctions conducted by CIL taking into account the non-coking coal grade specifications.

* The process involves collection of data comprising bid prices and sale volumes at various auctions conducted by CIL subsidiaries.

* After data standardisation, a Representative Price (RP) is calculated against each grade.

* Finally, these individual grade-wise prices are clubbed into sub-categories, and further normalised to derive the final index for various GCV bands by applying weights.

The index has been formulated in an attempt to provide a mechanism for monitoring the market and for domestic coal price comparison. CoalMint proposes to release the ICI for five distinct grades of coal.

2nd Asia Coal Outlook & Trade Summit

With elections round the corner and the pressing need to avert a power crisis, the Indian government has again mandated coal imports for power plants. What is the outlook on India’s coal imports in 2023 and beyond? Be a part of the discussion at CoalMint’s 2nd Asia Coal Outlook & Trade Summit to be held at Grand Hyatt Erawan in Bangkok, Thailand on 24-25 April, 2023.

Leave a Reply