When Coal India Ltd (CIL) opened the ninth tranche of its coal linkage auction in December, the response from sponge iron manufacturers was a mix of pragmatism and guarded optimism. The auction offered 18 million tonnes annually for ten years, a volume large enough to influence both domestic supply patterns and India’s dependence on imported coal. But the early bidding behaviour revealed an industry weighing stability against chemistry, paperwork against flexibility, and a decade-long commitment against day-to-day furnace realities.

By 8 December, bidders had taken up about 40% of the offered volume, with premiums around 14% above notified prices-a robust signal in a year marked by weaker global coal prices. Lots from SECL and ECL-the two subsidiaries whose grades suit kiln-based direct reduced iron (DRI) processes better-drew the most interest.

What is unfolding now is not a dramatic overhaul of India’s coal ecosystem but a practical recalibration. CIL is shifting more coal toward industries that actually want it, while sponge iron producers are trying to secure reliability without surrendering the performance advantages of imported coal.

Why sponge iron producers are looking at linkages again

India’s sponge iron industry, concentrated in Odisha, Chhattisgarh, Jharkhand and parts of Karnataka, is among the country’s most coal-intensive sectors. Between January and September 2025, coal-based DRI production rose 11 per cent year on year to 37.2mn tonnes, even as steel margins narrowed and power tariffs softened.

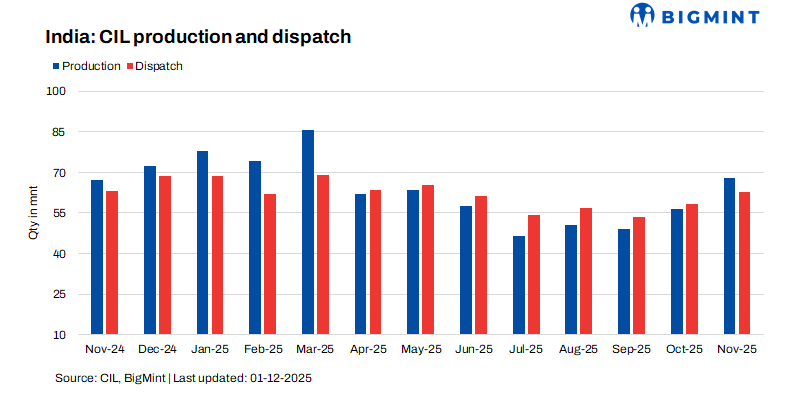

Domestic coal supplies to the sector, however, moved in the opposite direction. CIL deliveries between April and October 2025 fell to 4.32mn tonnes, a 52 per cent decline from 8.96mn tonnes a year earlier. The shortfall partly reflected logistical constraints early in the year, including limited rake availability at SECL, and partly CIL’s policy obligation to prioritise power utilities during peak demand months.

By the third quarter, those pressures eased. Coal-fired power generation was down 6 per cent year on year, inventories at power plants were comfortable, and demand from the power sector softened. CIL responded by redirecting supplies to non-power users, with dispatches rising 19 per cent to captive power plants, 30 per cent to steelmakers and 24 per cent to cement producers.

A rule-bound return to domestic coal linkages

The sponge iron industry, being a major user of fixed-carbon-rich thermal coal, became a natural candidate for renewed domestic servicing. The auction is CIL’s route to restore, and formalise, that relationship. The linkage auction is not a free-market scramble; it is a highly codified exercise governed by a detailed scheme document.

Bidders are required to calculate their Normative Coal Requirement (NCR) after adjusting for all existing sources of supply. This includes current coal linkages, allocations from earlier SHAKTI auctions, output from captive mines, and any volumes already secured through commercial or e-auction routes. Errors in this calculation are not procedural oversights: an incorrect NCR can lead to bid disqualification or post-auction reductions in allocated volumes.

The auction itself follows a price discovery process in which premiums rise in ₹75-per-tonne increments until demand matches available supply. Bidders are not permitted to increase volumes after the auction, a rule that incentivises early and decisive bidding. As a result, several sponge iron producers bid aggressively in the initial rounds to lock in baseline quantities.

Successful bidders face strict post-auction obligations. They must furnish a performance security equivalent to 6 per cent of the contract value, execute a Fuel Supply Agreement within 90 days, and consume the coal only at the declared plant. Compliance is verified by a Final Verification Agency, and any discrepancy between declared requirements and actual consumption can trigger a downward revision of the linkage quantity.

Annexure IV of the scheme document outlines immediate suspension if any authorised agency reports diversion of coal outside the intended plant. A formal charge sheet can lead to five years of blacklisting-and this blacklisting transfers to any successor if ownership changes.

For many bidders, this compliance environment is as important as coal quality. A linkage is a guarantee, but also an obligation.

The cost-plus option

A distinctive feature of this tranche is the option to bid for coal from Cost-Plus mines such as Borda UG. Here:

- The coal price is linked to actual mining cost

- The mine will start only if 85% of capacity is booked

- Bidders must place a large Risk Coverage Financial Guarantee

In return, they may get more predictable supply and insulation from market volatility. But it is a capital-heavy gamble, suitable mainly for companies with steady downstream steel commitments.

Conclusion

CIL’s ninth linkage auction offers sponge iron producers a rarity in India’s coal market: predictability. In an industry where coal drives both costs and product quality, that stability carries tangible economic value.

The compromise is familiar. Domestic coal linkages provide supply certainty but not always the desired quality, while imported coal delivers performance at the expense of price and supply volatility. Most producers are therefore expected to blend the two, calibrating their mix to kiln design, market conditions and risk appetite.

Rather than a structural overhaul, the auction marks a reset in the relationship between India’s largest coal miner and one of its most coal-intensive industries. The real test will be execution: CIL’s ability to supply consistently, and the sponge iron sector’s ability to absorb a more regulated but dependable domestic coal regime.

Leave a Reply