- Bullish coke price outlook supported by strong steel demand

- Supply-side tightness in coking coal continues to support higher coke prices

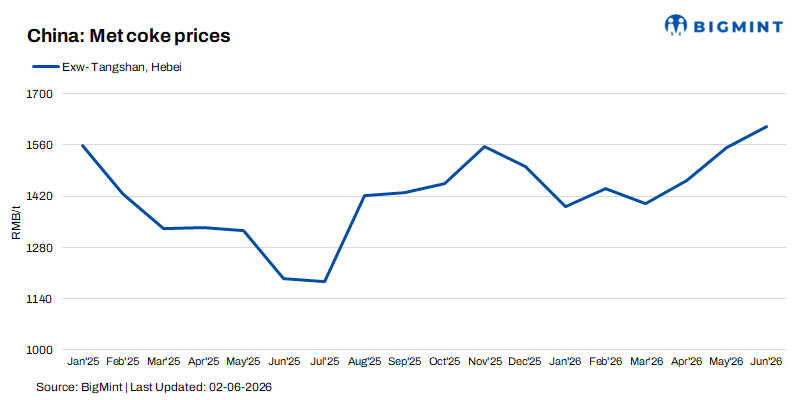

Mysteel Global: Major coke producers in North China’s Shanxi, Inner Mongolia, and Hebei announced a new round of metallurgical coke price increases on May 29, set to take effect on June 1. The short-term market outlook remains supported by resilient downstream demand and firm coal prices.

Mysteel Coke Index (MCI) CDQ, gauging China’s national dry-quenched quasi-first-grade met coke prices, stayed flat on day at Yuan 1,731.2/tonne ($255.9/t) on May 29, while the MCI CWQ for wet-quenched quasi-first-grade met coke also stood still at Yuan 1,572.5/t, both including VAT.

The new price markups those coke firms proposed last Friday remained at Yuan 50/t and Yuan 55/t for wet-quenched and dry-quenched stamp-charged met coke cargoes, but several producers also demanded a larger Yuan 85/t hike for their dry-quenched top-charged products this time, citing the tightened market supply and higher coal costs.

As of Monday morning, steel mills have yet to respond to the newly proposed coke price hikes, Mysteel notes. Market players expect the mills to eventually accept the increases despite possible attempts to delay, and the market is also believed to be open for further markups going forward.

“Given their current high hot metal output, mills seem inclined to accept the new coke pricing to lock in sufficient raw material cargoes,” a survey respondent said. Mysteel’s survey showed that daily hot metal production among the 247 integrated steel mills climbed to 2.41 million tonnes/day during May 22-28, a new high in over seven months.

Sources reported that steel mills were actively seeking additional coke cargoes, wary of potential supply disruptions amid the tightened availability of coking coal – a major input feed for making coke.

Additionally, coking coal prices have continued surging due to the ongoing broad safety inspections across the country’s major coal-mining hubs. The rising production costs also encouraged coke firms to demand further rises in met coke prices.

Mysteel’s latest survey showed that in Shanxi, 18 of the 130 coking coal mines that had been suspended after a fatal accident resumed production as of Friday morning, bringing 25.3 million tonnes/year of capacity back online. A 122 million t/y capacity remained halted, however.

Mine safety oversight in the coal hub stays tight, Mysteel has learned. Shanxi announced on May 30 the launch of a special campaign to rectify coal mine safety. Some sources expect coking coal prices to gain further momentum in the near term, thus supporting coke prices as well.

The portside coke market remained firm on Friday. Mysteel assessed wet-quenched quasi-first-grade coke (CSR 60%) and first-grade coke (CSR 65%) at Yuan 1,620/t and Yuan 1,720/t, respectively, ex-stock Rizhao port in East China’s Shandong, both higher by Yuan 10/t from the last session and including VAT.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply