- Russian thermal coal remains $13/t cheaper than domestic supply

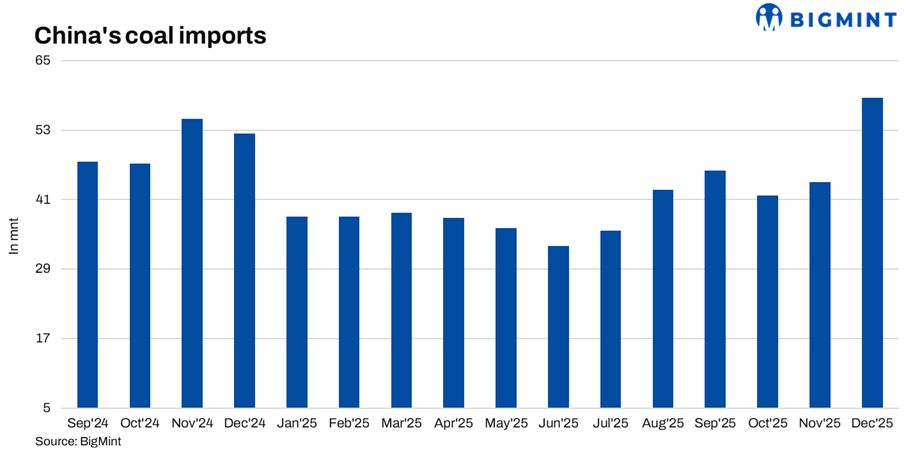

- Bohai port stocks down 23% y-o-y, signalling tightening availability

China’s non-coking or thermal coal market reflects a familiar pattern as of 23 February 2026: imported coal remains competitively priced. Seaborne Newcastle 6,000 kcal coal traded near $116/t FOB, while Richards Bay coal stood around $102-103/t FOB. Lower-rank Indonesian 4,200 GAR coal hovered near $52-53/t FOB, keeping it attractive for Asian buyers.

Russian coal continues to hold the strongest delivered advantage into China. Delivered prices into northern Asia remain roughly $13/t cheaper than comparable domestic coal, allowing Russian suppliers to maintain a steady foothold. Indonesian coal remains the next most competitive origin, though its price advantage has narrowed as FOB levels rise.

Tight port stocks keep imports relevant

Inventory data explains why imports still play an important role. By 23 February, coal stocks at China’s Bohai Sea ports were around 14.7 million tonnes (mnt), roughly 23% lower y-o-y. Qinhuangdao alone held about 5 mnt, nearly 29% below last year’s levels.

Such tight inventories would normally imply stronger import demand, reinforcing China’s continued reliance on seaborne supply when domestic logistics tighten or consumption rises.

China Shenhua expansion signals structural policy shift

At the same time, China is strengthening its domestic coal system. Regulators recently approved a major restructuring plan allowing China Shenhua Energy to acquire nearly $19 billion in assets from its parent group. Once completed, this integration will lift Shenhua’s production capacity beyond 500 mnt per year, while expanding its logistics and power generation network.

This move reflects a broader policy objective: building a vertically integrated coal system that can stabilise supply, manage pricing pressures, and respond quickly to market disruptions.

What this means for global coal trade

In the short term, China is likely to keep importing coal wherever arbitrage remains favourable — particularly from Russia and Indonesia.

But structurally, Beijing is preparing for a future where domestic producers have greater control over supply and pricing.

For exporters, this signals an important shift. China will remain a large and influential buyer, but it is becoming more strategic — entering the market selectively rather than consistently.

That transition could make global coal demand more sensitive to policy signals from Beijing than to price movements alone.

Leave a Reply