- Crude steel output dips on summer demand woes

- Manufacturing PMI plummets to 32-month low

- Strong production, sales continue in auto segment

Morning Brief: China’s steel industry experienced a downswing in May 2025, as the market remained on tenterhooks regarding the trade tensions with the US. May also marked the onset of the traditional off-season for the industry, with unfavorable weather conditions stalling construction activity.

Key macroeconomic indicators such as crude steel production, manufacturing investment, and cement output recorded declines y-o-y in January-May, indicating a slowdown in both the supply and demand sectors. In contrast, steel exports, coal production, and automobile production maintained strong growth y-o-y.

BigMint goes behind the scenes.

Crude steel production declines y-o-y: Reversing the slight uptick of January-April (4MCY’25), China’s crude steel production fell 1.7% y-o-y in January-May (5MCY’25). This was precipitated by a 6.9% y-o-y drop in May, though volumes inched up by 1% m-o-m.

The decline could be chalked up to the seasonal demand slowdown in end-user segments such as construction. A number of regions experienced extreme weather events, either sweltering heat or flood-inducing rains, which hindered end-user activity. Additionally, the government’s directives to cut steel production, issued earlier this year, are also considered to have suppressed steel-making momentum.

Parallelly, pig iron production was 0.1% lower y-o-y in January-May, compared to a 1% increase in the first quarter.

Steel export rush continues: In May, China’s steel exports increased by 9.8% y-o-y and 1.2% m-o-m to a seven-month peak of 10.58 million tonnes (mnt). This lifted January-May volumes by 8.9% compared to 8.2% in January-April.

Front-loading of shipments has led to the sustained spike in steel exports, with exporters expediting deliveries amid concerns about further flare-ups in trade tensions globally. The temporary relaxation of most tariffs, announced in mid-May, was not strong enough to bolster market confidence.

In tandem, China’s steel imports fell 16.1% y-o-y in January-May compared to 13.9% in January-April. The drop widened, possibly due to sluggish manufacturing activity.

Drop in iron ore imports shrinks: China recorded a 5.2% y-o-y drop in iron ore imports in 5MCY’25, with the gap shrinking marginally from the 5.5% fall of 4MCY’25. However, imports slipped 4.9% m-o-m and 3.8% y-o-y.

Amid trade uncertainties and cautious market sentiment, steelmakers preferred sourcing from portside inventories, which were available in abundance and at lower rates. This led to the slight drop in iron ore imports m-o-m.

Meanwhile, restocking momentum remained strong, which supported volumes.

Coal production growth slows down: While China continued to record growth in its coal output, the pace slowed to 6% y-o-y in January-May against 6.6% in 4MCY’25. March recorded modest increases of 4.2% y-o-y and 3.6% m-o-m.

The deceleration in production momentum could be due to the worsening supply glut in the market, compounded by sluggish industrial demand and a progressive shift to renewable sources of energy.

According to reports, fossil fuel-driven power generation, which is mostly coal based, fell 3.1% in 5MCY’25, while production from renewables, including wind and solar, remained robust.

The persistent domestic surplus also caused a 17.7% y-o-y decrease in May’s coal import volumes. January-May shipments were down 7.9%, sharper than the 5.3% drop in January-April volumes.

Manufacturing growth remains subdued: Overall, manufacturing activity was weak in May. The Caixin manufacturing purchasing managers’ index (PMI) dived 2.1 points m-o-m to a 32-month low of 48.3, signifying a sharp slowdown, attributed primarily to trade war-related uncertainties.

However, official data from the National Bureau of Statistics (NBS) presented a slightly contrasting picture, though it too pointed to the manufacturing sector remaining in contraction territory. NBS placed its PMI at 49.5, with a minor 0.5-point improvement from April.

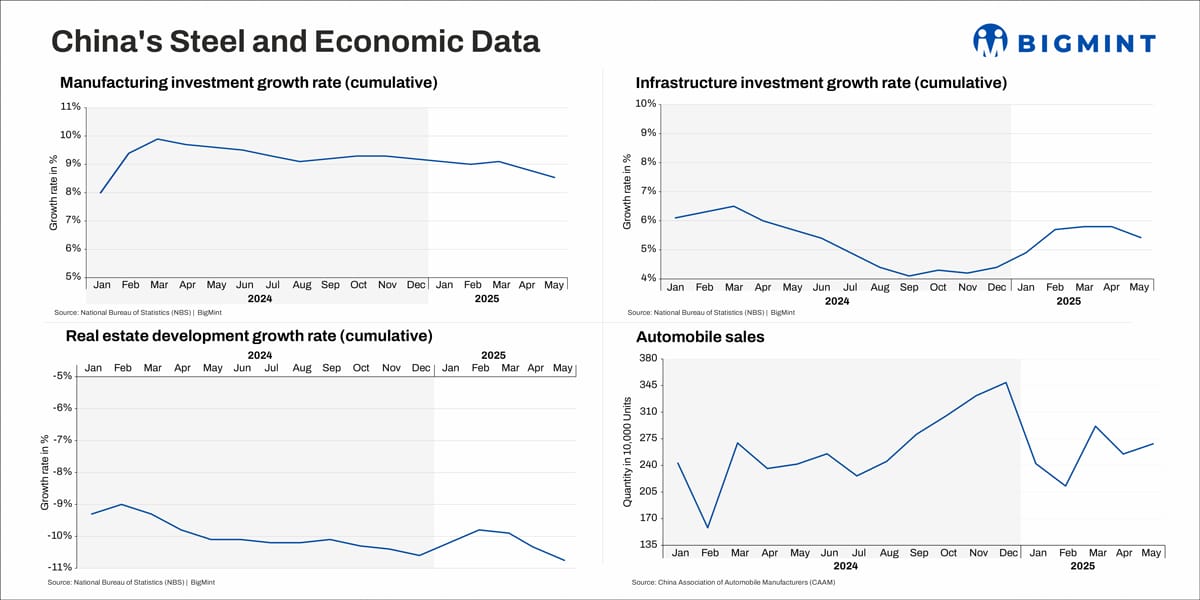

The manufacturing investment growth rate reduced to 8.5% in May from 8.8% in April. In January-May 2025, growth was at 8.9% compared to 9.3% in the year-ago period.

Auto segment remains in high gear: Auto production bucked the manufacturing downturn, with May volumes being higher by 1.1% m-o-m and 11.6% y-o-y. However, 5MCY’25 levels were lower by 0.2 percentage points from 12.9% in 4MCY’25.

Auto sales climbed up by 3.7% m-o-m and 11.1% y-o-y in May while being higher by 11% y-o-y in 5MCY’25.

In January-May, automobile exports increased 7.9% to 2.49 million units compared to 6% y-o-y in 4MCY’25.

Slide continues in realty, infra activity: Weather-driven disruptions in construction activity impacted both the infrastructure and realty segments. Moreover, realty also continued to flounder due to weak sales.

Infrastructure investment growth fell to 5.6% in May from 5.8% in April. Meanwhile, the rate fell to 5.56% in 5MCY’25 compared to 6.12% in 5MCY’24.

Real estate development growth dipped to -10.7% in May from -10.4% in April. The corresponding value for 5MCY’25 was -10.2% against -9.5% in the year-ago period.

Additionally, property sales by floor area dropped 2.9% y-o-y in January-May, slightly higher than the 2.8% of January-April. New home prices also inched down by 0.2% in May, extending a two-year downtrend.

Similarly, cement production fell a steeper 4% y-o-y in 5MCY’25 against 2.8% in 4MCY’25. However, new construction starts slumped by a slower 22.8% versus 23.8% in 4MCY’25.

Outlook

China’s steel industry may continue to weaken, as it wrestles with rampant overcapacity and a persistent supply-demand mismatch.

Recently, the China Iron and Steel Association (CISA) forecast a 4% drop in crude steel production in CY’25, aligned with the government’s efforts to curb the output glut. If this decline materialises, then iron ore and coal imports will, of course, fall further.

However, some market participants believe that these production curbs are unlikely to be enforced soon. This is because Beijing may be unwilling to undermine GDP growth targets amid a general economic contraction by placing restrictions on steel production. Nonetheless, output may soften due to flagging demand and weak prices, with the CISA recently urging mills to practice “self-discipline”.

Additionally, iron imports may rise in the near term amid restocking efforts, as steelmakers take advantage of current low prices to make opportunistic purchases.

Meanwhile, steel exports are likely to moderate, with rising trade tensions with the US being the key contributor.

Uncertainties regarding trade prospects may also dampen manufacturing sentiment in the near term. Overall, the outlook remains downcast.

Leave a Reply