- Korea, Vietnam pull up volumes y-o-y

- Middle East throws up mixed trends

- Commercial grades exports to sustain in medium term

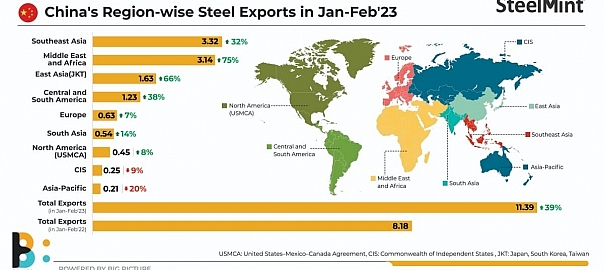

China’s steel exports over January-February, 2023 rose a substantial 39% to 11.40 mnt compared to 8.18 million tonnes (mnt) in the same two months in 2022.

M-o-m, however, volumes remained stable in February 2023, dipping a mere 1% to 5.66 mnt from 5.72 mnt in January.

Data reveals that Vietnam and Korea put up a good imports show while demand from the rest of the world was subdued.

1. Southeast Asia: China’s exports to this region in February rose 23% m-o-m and 32% over January-February 2023 compared to the same two months last year. Southeast has traditionally been the largest export market for China and the trend has sustained, although Middle East and Africa had gained some prominence last year.

Within Southeast Asia as well as globally, Vietnam was the second highest buyer from China after Korea. Its volumes rose a whopping 126% m-o-m in February and a more sedate 24% y-o-y in January-February, 2023.

Vietnam end-users had been buying considerably from China, avoiding the comparatively higher offers from Indian mills. Although the Vietnamese also bought domestically, home-grown products were pricier which goaded them to opt for Chinese material. “Chinese mills operated very strategically. If Vietnam’s domestic prices were say at around $800/t, the Chinese offers were brought down to $650-660/t,” a source informed SteelMint.

Secondly, Vietnamese end-buyers prefer certain width specifications which were readily met by the Chinese mills.

Thirdly, Vietnam’s domestic mills were focused on exports to Europe. This gave Chinese mills an opportunity to fill in the need gap in Vietnam’s domestic market.

2. Middle East & Africa: This geography has seen a mixed trend. M-o-m volumes saw a 13% drop but January-February saw a y-o-y increase of 75%. Volumes dropped in February because the Middle East was buying mainly from Indian mills.

Middle East is a substantial buyer because it lacks indigenous mills for hot rolled coils and is thus solely dependent on imports. However, the voyage time from China, Vietnam, Korea and Japan is much longer compared to India. And since most of Middle East and African buyers do need-based procurement, they require material with lesser lead time. Hence, it is more viable to not buy so much from China but India, with the voyage time from the latter being a mere 10-15 days.

Turkey, on the other hand, bought from China, with a demand rebound seen in Europe from January onwards. Volumes rose slightly m-o-m in February to 0.22 mnt (0.18 mnt in January) and 81% y-o-y to 0.41 mnt over January-February, 2023.

But African countries were absent because of weak economies and currency issues.

3. Europe: Volumes to Europe dropped 29% m-o-m in February and rose a nominal 7% y-o-y over January-February, 2023. The European Union has anti-dumping duties implemented against China, because of which volumes are never on the higher side. The EU was busy buying from India, Japan, Korea and Vietnam when it returned to the market early this year, after a long hiatus.

4. East Asia: February volumes to East Asia rose 18% m-o-m but a heftier 66% y-o-y in January-February, 2023.

Korea stole the East Asia show with the highest volume of 0.72 mnt of Chinese steel imports in February, a 20% m-o-m increase. Y-o-y, volumes rose a whopping 88% to 1.33 mnt in January-February this year. This trend can be attributed to production issues at Korean domestic mills because of factors like floods, a major cyclone, fire etc last year. Sources inform SteelMint that the impact of these factors is still being felt at leading mills in Korea with hot rolled strip production down 8% over January-November, 2022, necessitating imports.

Moreover, the voyage time between northern Chinese mills and Korea is a mere one day, where the freights are barely $10/t. “This is similar to a local shipment,” observed a source, adding it is highly cost-effective for Korean end-users to ship in material from China.

Japan, the second-highest importer within East Asia, saw a 21% m-o-m decline in February and a moderate 6% y-o-y growth in January-February. This country is looking at a closure of considerable polluting blast furnace capacity. Japan’s steel consumption dropped almost 8% in 2022. Hence, its imports also declined amid an overall decline in steel consumption while it concentrated more on exports to the EU.

5. South Asia: The currency erosion, which began from last year, has robbed countries like Bangladesh, Pakistan, Sri Lanka and Nepal of the strength to import. Dollar reserves have dwindled, giving these countries hardly any leeway to import. Therefore, the region saw a steep 58% drop m-o-m in February and a 14% growth y-o-y in January-February this year.

Outlook

The global banking financial crisis may have some impact on China’s exports in the very near term since, sources say, already, many enquiries have possibly been withdrawn.

But China’s exports of commercial grades of steel are likely to remain stable in the medium term because of two reasons. One, since the scope of value-added production is limited at present amid production cuts and the dire need to revive domestic demand, commercial grades will continue to rule for some more time.

Two, with India, Vietnam, Korea and Japan highly focused on the high-margin EU exports market, the entire Middle East, Africa and Southeast Asia are China’s happy export hunting grounds now. “These markets are not as lucrative as the EU but China competes very efficiently here,” observed a source, adding that China has also entered South and Central American markets in a big way.

Leave a Reply