- China’s total steel exports up by 22% in Jan-Jun’24

- China’s domestic steel demand remains lackluster

- Volumes may gain traction amid competitive offers

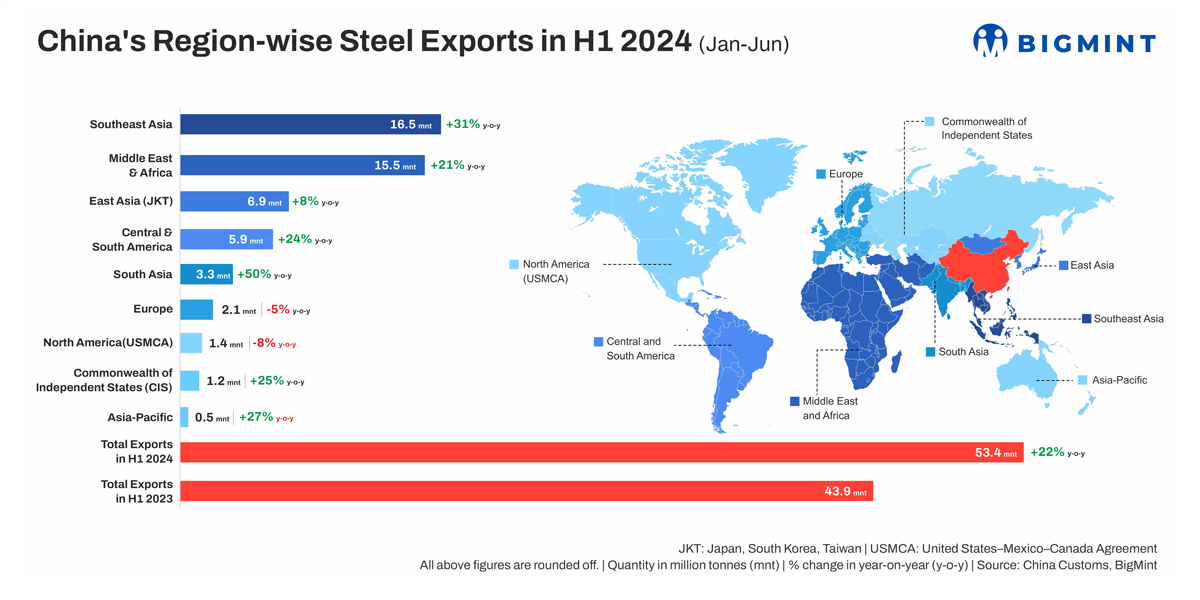

Morning Brief: China’s steel exports in the first six months of 2024 (H1CY’24) rose sharply by 22% y-o-y. As per Chinese Customs and BigMint data, exports of steel products by China in January-June 2024 reached 53.4 million tonnes (mnt) compared with 43.9 mnt in the corresponding period of 2023.

However, on m-o-m basis, total exports in June 2024 dropped by 9% to 8.74 mnt against 9.63 mnt in May. The major key importing markets recorded m-o-m declines.

ChinasRegion-wiseSteel-Exports-in-H1-2024-Jan-Jun.pdf

Region-wise exports

SE Asia continued to be the largest steel importer from China with volumes rising 31% y-o-y over January-June to nearly 16.53 mnt (12.62 mnt in the same period last year). However, m-o-m volumes fell by 11%.

Vietnam, China’s largest exporting country, saw volumes surging 73% to 6.37 mnt (3.68 mnt). Rest of the Southeast Asian geographies also recorded an increase y-o-y for the period under review.

On a m-o-m basis, Vietnam and Thailand saw a decline of 25% and 21% to 0.86 mnt (1.16 mnt) and 0.42 mnt (0.53 mnt) respectively. While, the volumes of other major countries inched up m-o-m.

Middle East & North Africa (MENA), which has been buying quite heavily from China, was in second position in H1CY’24 with almost 15.49 mnt, up 21% from 12.78 mnt seen from the same period last year. On a m-o-m basis volumes declined by 13% in June to 2.36 mnt (2.70 mnt). The UAE, the top importer, surged by 51% y-o-y to almost 2.57 mnt (1.71 mnt), although volumes dropped by 11% m-o-m. However, Turkiye experienced a 16% drop in H1CY’24 to 2.18 mnt (2.59 mnt).

The monthly volumes fell in June as market participants in the region were on holiday between 16 to 18 June for the Eid-al-Adha celebrations. Moreover, the natural choice for imports was China, not because it was the preferred option but because India got out-priced.

East Asia recorded an 8% increase to almost 7 mnt (6.38 mnt). Volumes to Japan rose 19% to 0.63 mnt (0.53 mnt) while Korea inched down by 2% to 4.42 mnt (4.51 mnt). Some of the geographies that import lesser volumes reported declines m-o-m.

South Asia witnessed a 50% increase in January-June to 3.35 mnt (2.23 mnt). Disturbingly, volumes to India rose 43% to 1.42 mnt (0.99 mnt). Here too, even if the y-o-y trend was positive, on a m-o-m basis, Pakistan, Bangladesh and Sri Lanka recorded declines.

Europe was written in red as volumes were down by 5% in January-June to 2.09 mnt (2.20 mnt) while major countries showed m-o-m declines in June and only Spain rose by 4% y-o-y In H1CY’24

Why China’s exports surged in H1?

Slack home demand: Steel demand in China remains lackluster due to the continued under performance of the construction sector, which accounts for around 35% of Chinese steel demand. Mills had no option but to eye offshore markets to offset losses incurred at home. The real estate sector is still struggling with investments falling another 10.1% in June and growth averaging -9.6% in H1CY’24 against -6.85% in the same period last year.

China’s domestic demand was also impacted by unfavourable weather conditions, including high temperatures in the north and heavy rains in the east and south, leading to slower construction activity. This, combined with lower futures prices, dampened domestic consumption. Moreover, China’s steel production inched up by 0.2% y-o-y in June to over 91.61 mnt against 91.11 mnt in the same month last year.

Price advantage: China’s steel industry continues its stronghold as the world’s largest exporter through aggressive pricing strategies. Data reveals China has been consistently keeping global HRC offers lower, undercutting competitors from India, Japan, and South Korea. China has not only captured market share globally but also posed a significant challenge to domestic producers in key markets like India and Vietnam.

In June, its HRC offers had hit a rock-bottom of $522/tonne (t) FOB whereas Japanese quoted $560/t, while Indian mills have continued to hold their HRC export offers. In July, data reveals Chinese offers are at $509/t FOB.

In addition, Vietnamese domestic demand was lackluster. However, end-buyers kept up the procurement tempo from China because domestic prices were comparatively higher. For instance, if Chinese prices averaged $573/t CNF Ho Chi Minh City (HCMC) over January-June, then Hoa Phat’s offers were higher at $590/t CIF HCMC. Formosa prices were even higher at $608/t CIF HCMC. Imports from China offered greater price viability.

Yuan depreciation boosts Chinese exports: A weaker Chinese yuan has provided a significant advantage to the country’s manufacturing and export sectors. From a high of 6.93 to the dollar in H1 CY’23, the yuan lost almost 3% to a low of 7.15 in H1 CY’24. Despite lower selling prices, Chinese mills profited by increasing export volumes. This aggressive pricing strategy successfully attracted buyers from many countries.

Outlook:

China’s HRC export prices have hit a four-year low, currently standing at approximately $500/t FOB. This marks a significant downturn, with the last instance of prices falling below the $500/t threshold occurring in August 2020, during the COVID-19 pandemic. The current price level represents a notable decline, highlighting China’s competitive export strategy in the global steel market.

China’s indirect steel exports, which have been showing a healthy growth trend, especially over the last three years, are likely to end calendar 2024 with a 9% increase to around 127 mnt.

Moreover, China’s steel exports are likely to remain robust in the second half of 2024, driven by competitive pricing and growing demand in emerging markets. Despite global economic headwinds, China’s steel exports are expected to continue growing, at a moderate pace, as the country’s steelmakers leverage their strengths to capture market share and offset sluggish domestic demand.

Leave a Reply