- Exporters ramp up shipments to get ahead of US tariffs

- Government to tighten export tax regulations from 1 May

- Predatory pricing continues, helps exporters lift volumes

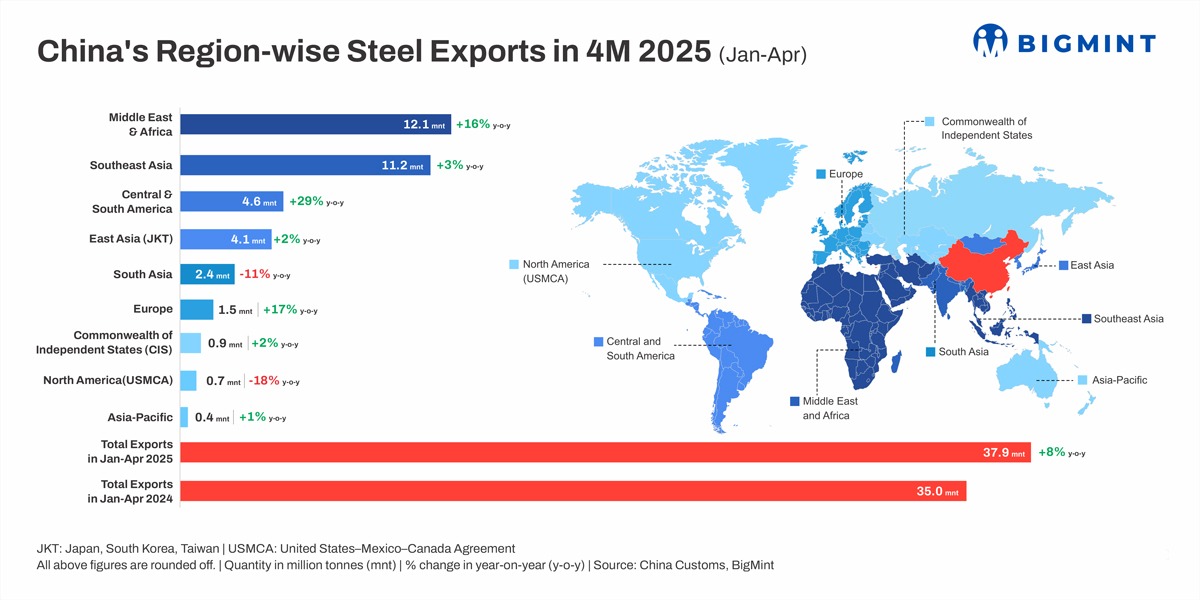

Morning Brief: China’s steel exports climbed up by a healthy 8% to 37.9 million tonnes (mnt) in January-April 2025 (4MCY’5) from 35 mnt recorded in the year-ago period, as per data compiled by BigMint.

China’s steel exports continued at a healthy pace in January-April, as suppliers ramped up shipments amid fears of spiralling trade tensions with the US. Additionally, rising protectionism globally also pushed exporters to seek new destinations, with trade barriers in place in key importing countries such as Vietnam, South Korea, Europe, and India.

Export momentum also accelerated m-o-m in April, given that January-March witnessed a slower 6% growth. In April, exports were 10.5 mnt, stable m-o-m but up 13% y-o-y.

Click here to download the pdf- China’s steel exports picked up in Jan-Apr’25 despite tariff pressures. But is the peak approaching?

Region-wise break-up

China’s leading export destination in 4MCY’25 was the Middle East and North Africa, which logged a 16% y-o-y increase to 12.1 mnt. All the countries in this region, except for Turkiye, recorded positive growth in imports from China during this period. The UAE led in terms of volumes received, with 1.96 mnt (13% y-o-y growth), followed by Saudi Arabia at 1.76 mnt (up 13% y-o-y).

Notably, China has been offering extremely competitive prices to the Middle East in the recent past, which has prompted Indian mills to withdraw active offers to this region. Meanwhile, Turkiye has been grappling with subdued steel demand.

Southeast Asia was a close second with 11.2 mnt, a y-o-y increase of 3%. Only Vietnam saw a 26% drop in volumes to 3.23 mnt, amid the imposition of anti-dumping duties on hot-rolled coil (HRC) imports from China.

Shipments to East Asia dropped 11% y-o-y in January-April to 4.1 mnt. In this region, exports to South Korea plunged 21% y-o-y to 2.40 mnt and to Taiwan by 27% y-o-y to 0.45 mnt. Again, South Korea has imposed an anti-dumping duty on Chinese steel plates, while Taiwan is mulling the same on hot-rolled and flat-rolled steel imports.

Volumes to South Asia grew 17% y-o-y to 2.44 mnt, with India being the sole country to see a drop. Volumes to India fell 29% y-o-y to 0.6 mnt in 4MCY’25, driven by cautious sentiment amid the safeguard duty.

Exports to North America saw an 18% decline y-o-y to 0.74 mnt. However, despite further escalations in the trade war with the US and the 25% steel import tariffs, the country recorded a 12% y-o-y rise in Chinese steel arrivals to 0.30 mnt due to knee-jerk buying ahead of the tariffs coming into force.

Central and South America witnessed a 29% surge to 4.6 mnt, while Europe experienced a slight 2% uptick to 1.49 mnt.

Factors impacting China’s steel exports in Jan-Apr’25

Tariff battle with US intensifies: While it was expected that Trump’s ascension to the Oval Office would further strain Sino-US relations, tensions escalated exponentially in April, following the unveiling of reciprocal tariffs. A fierce back-and-forth ensued, with China and the US both firing back by increasing tariffs on each other’s products. Ultimately, the US’s tariffs on Chinese exports totalled a whopping 145%, while those imposed by China on US-origin goods were an equally severe 125%, before they were rolled back to 30% and 10%, respectively, for a 90-day period.

This led to intense market uncertainty and volatility, and Chinese exporters frontloaded shipments to avoid the brunt of heightened trade barriers.

Trump’s earlier 25% steel import tariffs were less of a worry, with China’s direct exports to the US constituting a minor share of its total.

Additionally, it is to be noted that the US’s reciprocal tariffs are set to impact most of its trading partners and will be applicable to a number of downstream products. The tariff fear, consequently, led numerous producers globally to ship higher volumes to the US. Consequently, with China being a key source of cost-competitive steel for numerous manufacturing units globally, demand for its imports was also higher.

China undercuts offers from other exporting regions: China continued to outprice other regions in steel exports. While HRCs from China were offered at $467/t FOB Rizhao, those from Japan were at $471/t FOB Tokyo. On the other hand, India’s offers were intermittent throughout this period, with offers to the Middle East on pause from mid-March, for example, because exporters were unable to compete with China.

These predatory pricing tactics allowed China to keep export volumes high.

Domestic demand makes sluggish recovery: While the warmer weather led to a recovery in domestic demand in early 2025, the rebound was slow and, overall, insufficient to absorb China’s mounting production volumes.

To illustrate, manufacturing investment growth averaged 9% in January-April compared to 9.3% in the corresponding period last year. Moreover, infrastructure investment growth was lower y-o-y at 5.55% in 4MCY’25 against 6.23% in the corresponding period of last year. Meanwhile, real estate development growth was -10.1% in 4MCY’25 against -9.4% in 4MCY’24. These indicate lack of business confidence and activity in these sectors. However, the auto sector bucked the downtrend, with a 13% y-o-y rise in production in 4MCY’25.

Even domestic steel prices reflect a downtrend. Rebars declined by RMB 40/tonne (t) ($6/t) to an average of RMB 3,290/t ($457/t) exw-Donghua in April from January, while HRCs fell around RMB 100/t ($14/t) to RMB 3,350/t ($465/t) in the same period. Both commodities saw a slight rally in February before falling in April.

Government cracks down on export tax evasion: Exporters also rushed to ship out goods before the government’s new regulations, aiming to put a stop to export tax evasion, came into effect on 1 May.

As per the new rules, relevant tax payment certificates are mandatory for customs declarations, and value-added and consumption taxes will be levied on exports at the same rate as on domestic sales.

These new regulations are significant, given that the use of fraudulent contracts and the under reporting of export values are common practices in the Chinese steel industry. This move is also expected to address concerns raised by other countries regarding China’s rock-bottom export prices and steel dumping.

Outlook

China’s domestic steel consumption is expected to decline this year, and mills will, no doubt, try to route as much merchandise as possible overseas. However, steel exports are unlikely to continue at this elevated level, given mounting trade barriers and an eventual moderation in production volumes. The new regulations to curb tax evasion may also pull down volumes in May. Earlier in April, the China Iron and Steel Association (CISA) had projected a 20 mnt drop in China’s exports this year.

However, indirect steel exports, such as through automobiles or machinery equipment, are expected to remain robust. China’s auto exports, for example, increased by 6% y-o-y to 1.9 million units in 4MCY’25 amid competitive prices and stronger demand from countries in the Global South.

Leave a Reply