- Steel exports rise a slower 23% in Jan-May’24

- Output caps may limit overseas sales in long term

- Country to discourage low-value items exports

Morning Brief: China’s steel exports are showing a slowdown in their growth momentum. Data collated by BigMint reveals, exports over January-May, 2024 (5MCY’24) grew a slower 23% y-o-y compared to the 30% seen over January-February and 28% in Q1CY’24 (January-March). Over January-April, exports rose 25%.

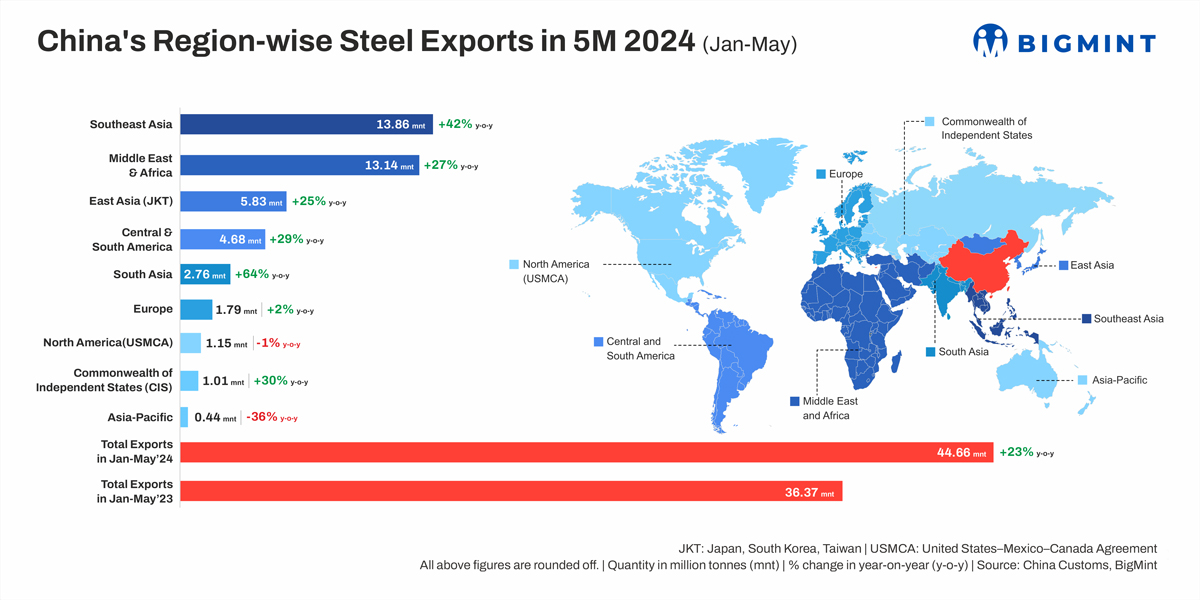

Volumes over January-May, 2024 were recorded at almost 45 million tonnes (mnt) against 37 mnt seen in the same five months in 2023.

On m-o-m basis, total exports in May 2024 rose a mere 4% to 9.63 mnt against 9.22 mnt in April.

China’s steel exports growth slows down in 5MCY’24.

Country-wise exports

SE Asia continued to be the largest steel importer from China with volumes rising 42% y-o-y over January-May to nearly 14 mnt (10 mnt in the same period last year). M-o-m volumes rose a mere 2%. Vietnam, China’s largest exporting county, saw volumes surging 89% to 5.51 mnt (2.92 mnt). But two of the major Southeast Asian geographies — Indonesia (-8%) and Malaysia (-4%) –recorded a decrease m-o-m in May.

Middle East & Africa showed a fairly healthy 27% growth y-o-y to 13.14 mnt (10.37 mnt). But Turkiye experienced an 18% drop over 5MCY’24 although volumes rose 17% m-o-m. M-o-m, Iraq’s imports too dropped 26% and Saudi Arabia’s, by 32% amid Eid celebrations.

East Asia recorded a 25% increase to almost 6 mnt (4.65 mnt). Volumes to Japan rose 21% to 0.50 mnt (0.41 mnt) and to Korea by 7% to 4 mnt (3.58 mnt). Some of the geographies that import lesser volumes reported declines m-o-m.

South Asia witnessed a 64% increase in January-May to 2.76 mnt (1.69 mnt). Disturbingly, volumes to India rose 51% to 1.10 mnt (0.73 mnt).

Europe was written in red as volumes upped a marginal 2% in January-May to 1.79 mnt (1.75 mnt) while major countries showed m-o-m declines in May and Italy, Poland, and The Netherlands over 5MCY’24.

Factors that influenced China’s steel exports in Jan-May’24

Crude steel production drop: After recording a 1.6% increase in January-February 2024, China’s crude steel production has been in decline and this may have impacted export allocations. Crude steel output dipped 1.9% over the first three months of 2024, and by 3% over January-April. A decline of 1.4% was seen in January-May, 2024. M-o-m, volumes have fallen since March, 2024 but rebounded 2.7% in May.

A few reasons are behind caps on output. One is the decline in key macro parameters over 5MCY’24, indicating sustained decreased steel consumption and squeezed margins of mills. Real estate construction, which contributes around 60% of downstream demand, has continued to perform poorly. Plus, manufacturing and infra performance has become sluggish leading to rising inventory levels.

Secondly, China is keen to achieve its decarbonisation goals and has issued special action plans for energy conservation and carbon reduction in four industries, including steel, which warrants production cuts.

Sustained lack of home demand: Sustained sluggish domestic consumption and squeezed margins are leaving Chinese mills with no option but to offload inventory overseas. Benchmarked HRC prices in Tangshan have fallen 7% to RMB 3,985/t ($549/t) in January-May 2024 from RMB 4,291/t ($591/t) in the year-ago period. Likewise, rebars lost 6% to RMB 3,769/t ($519/t) from RMB 4,001/t ($551/t).

Over January-May, funds in place for real estate developers fell by 24.3% y-o-y and new commercial housing sales declined 28% y-o-y, and newly started housing areas, by 24% y-o-y. Real estate development has been in negative territory since Covid and the collapse of realty giants a few years back.

Aggressive pricing strategy: But still China is holding on to its position as the largest steel exporter globally through its aggressive pricing strategy which is not only edging out suppliers from India, Japan, and Korea but also challenging domestic producers as well in various geographies, including India and Vietnam. For instance, Chinese-origin offers into Vietnam in 5MCY’24 averaged $578/t CNF Ho Chi Minh City (HCMC) against Indian mills $599/t CNF HCMC.

Vietnamese domestic producers were also on the backfoot in the face of the price onslaught. Hoa Phat’s offers were higher at $596/t CIF HCMC and Formosa’s at $614/t over January-May.Such a scenario has driven struggling Vietnamese producers to lobby with their government to launch an anti-dumping probe against imports of galvanised steel from China and Korea covering the period from 1 April 2023-March 2024. EU tube-makers last month also welcomed an anti-dumping investigation into low-priced imports of circular seamless pipes from China.

Middle East sees frenetic development: The Middle East and North Africa (MENA) region is poised for higher steel demand. Some sources pin the growth at 4% in 2024 while worldsteel has forecasted a 3.2% increase in this year. With Saudi Arabia having won the rights to host the Expo 2030 and the FIFA World Cup in 2034, frenetic development is taking place there. Plus, other regions are seeing accelerated demand for high-value API grades in the face of freshly-announced oil and gas projects. Thus, Saudi Arabia has shown a healthy 54% increase in 5MCY’24. This region is possibly going to remain a happy hunting ground for Chinese steel exporters.

Europe demand drops amid flat domestic prices: The European Union is not a heavy consumer of Chinese steel but still volumes were markedly down 19% m-o-m and up a marginal 2% y-o-y in 5MCY’24. Demand has been lacklustre amid still-high interest rates and energy prices. Imports were low because these were costlier as domestic mills kept prices flat amid uncertainty about changes in safeguard measures.

Outlook

There are proposals to resume tax rebates on exports of high-end products to encourage overseas sales of the same.

In end-May, China’s State Council issued an action plan for energy conservation and carbon reduction for 2024-2025. The policy envisages control on steel capacity and output and promotes high value-added products. It aims to put strict caps on exports of low value-added products, reflecting Beijing’s policy guidance for the country’s steel industry. Growing output caps may also reduce exports in the medium to long term.

Leave a Reply