- Weak global demand, rising trade barriers impact China’s steel exports

- High-value steel exports cushion impact of slowing construction steel demand

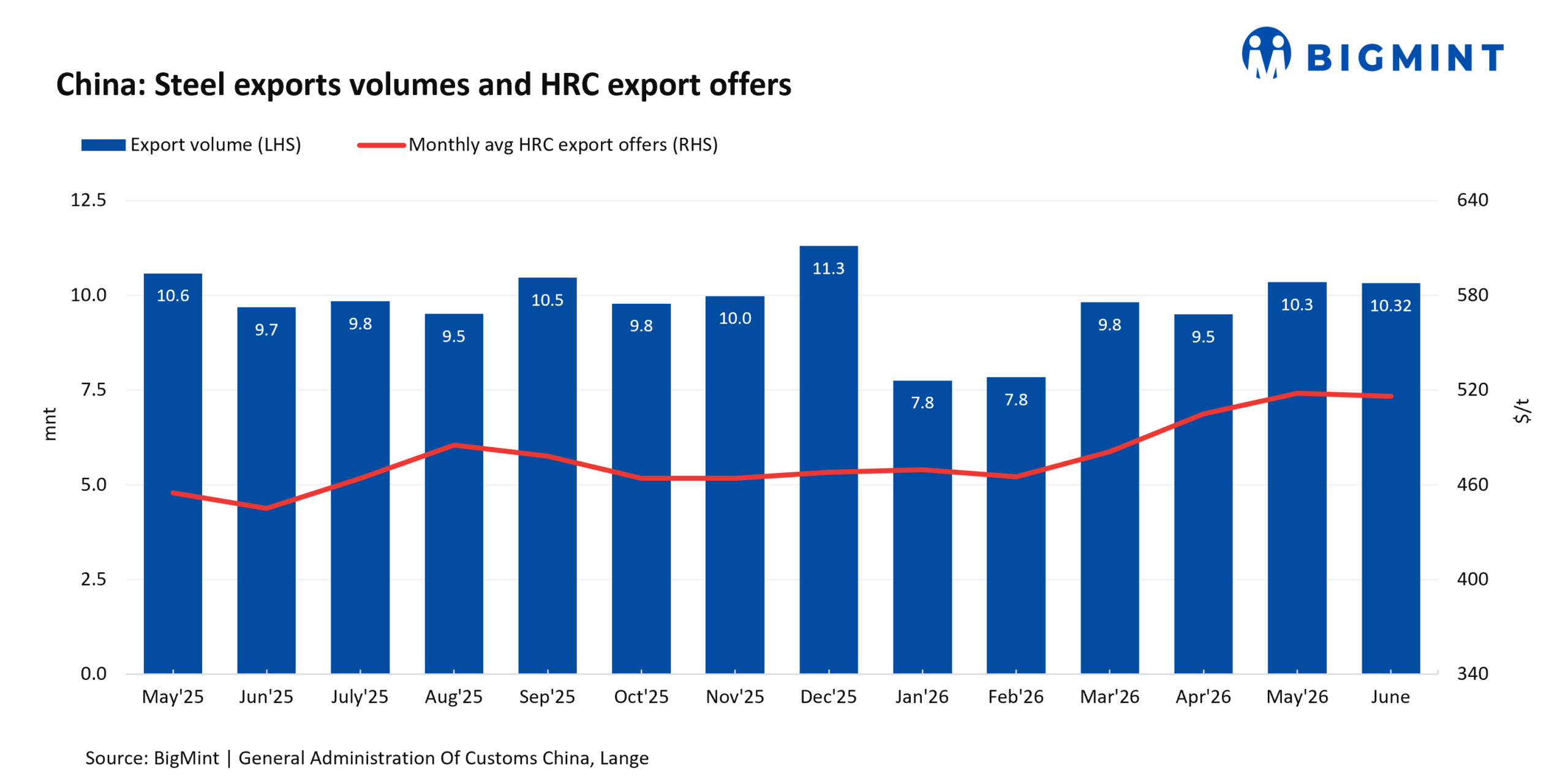

China exported 10.32 million tonnes (mnt) of steel in June 2026, up 6.6% y-o-y, reflecting stronger monthly shipments despite an increasingly challenging global trade environment. However, the improvement in June was insufficient to reverse the broader trend witnessed during the first half of the year. Cumulative exports during January-June 2026 declined 5.6% y-o-y to 54.874 mnt, as weaker overseas demand, expanding trade barriers and a stronger yuan continued to weigh on China’s export performance.

Export trends

Although June recorded the highest monthly shipment in recent months, export momentum remained uneven throughout the first half of the year. Early weakness in overseas bookings, coupled with slower demand across key importing regions, limited cumulative export volumes. The June recovery reflected improved shipment execution rather than a broad-based revival in global demand, leaving first-half exports below the corresponding period last year.

Weak global demand weighs on China’s steel exports

China’s steel exports remained under pressure during the first half of 2026 as weaker global demand reduced overseas buying interest and limited fresh export bookings. Demand softened across Southeast Asia, the Middle East and Europe, restricting sales opportunities for Chinese mills. While export volumes improved in June, the rebound was not sufficient to offset the weakness recorded earlier in the year.

In response to changing market conditions, Chinese mills increasingly shifted their export strategy towards higher-value flat steel products, including coated steel, electrical steel, automotive-grade steel and high-strength steel. This helped support export earnings even as demand for conventional construction steel products remained subdued.

Domestic demand remains weak

China’s domestic steel market also remained under pressure during the first half of 2026 as the prolonged downturn in the real estate sector continued to suppress construction activity, reducing demand for long steel products such as rebar and wire rod.

Although the manufacturing sector remained comparatively resilient, supporting consumption of flat steel used in the automotive, machinery, shipbuilding and renewable energy industries, the improvement was insufficient to compensate for the weakness in construction-related demand. At the same time, slowing overseas demand and growing trade restrictions curtailed export opportunities, leaving both domestic and international markets subdued during the period.

Trade barriers, geopolitical tensions curb China’s exports

Expanding trade protection measures emerged as one of the biggest challenges for Chinese steel exporters during the first half of 2026. Between June and July, Japan, the European Union, India, Brazil and South Korea initiated a series of anti-dumping investigations covering products including hot-rolled and cold-rolled steel sheets, welded steel mesh, steel shelving, grain-oriented silicon steel, hot-rolled steel plates, welded carbon steel pipes and tinplate.

The pressure was compounded by stricter import requirements in Europe and the United States, while geopolitical tensions in the Middle East weakened downstream steel demand across several key export destinations.

As overseas opportunities narrowed, Chinese mills increasingly focused on exporting higher-value steel products, while larger volumes of commodity-grade steel were redirected to the domestic market. The additional domestic supply intensified competition and placed further downward pressure on local steel prices.

Appreciating yuan reduces export competitiveness

The appreciation of the Chinese yuan also reduced the competitiveness of Chinese steel in overseas markets during the first half of 2026. The yuan strengthened from RMB 0.142818 to RMB 0.147297 over the period, making Chinese steel more expensive for foreign buyers.

The stronger currency, combined with the continued absence of export VAT rebates, increased exporters’ cost burden and further constrained export volumes during January-June.

Recovery in overseas steel production impacts China’s exports

Improving steel production outside China also reshaped global trade flows during the first half of 2026. As steelmakers in major producing regions increased output, importing countries relied more heavily on domestic supply, reducing their dependence on Chinese steel.

According to the World Steel Association, crude steel production across 70 countries and regions reached 157.9 mnt in May, down only 0.3% y-o-y, with the pace of decline narrowing significantly from the previous month. Excluding China, crude steel production increased 1.8% y-o-y to 73.5 mnt, reflecting higher operating rates among overseas mills.

Greater domestic steel availability in importing countries diverted procurement away from China, limiting export opportunities and adding further pressure on Chinese steel shipments.

Impact of VAT rebate removal

The continued absence of export VAT rebates remained another key factor behind the decline in China’s steel exports. Without the rebate, exporters are unable to recover the 13% VAT incurred during production, increasing export costs and compressing profit margins.

The higher cost burden has particularly discouraged exports of lower-value steel products. Combined with weak global demand, a stronger yuan and expanding trade protection measures, the removal of the rebate continued to weigh on China’s overall export performance.

Outlook

China’s steel export market is expected to remain challenging during July 2026 as tighter trade restrictions and subdued overseas demand continue to constrain shipment volumes. Nevertheless, exports of higher-value steel products are likely to remain comparatively resilient, supported by stable manufacturing demand and the ongoing shift towards a higher-value export mix.

Leave a Reply