- September output forecast at 3.44 mnt

- Mills resume operations post-shutdowns

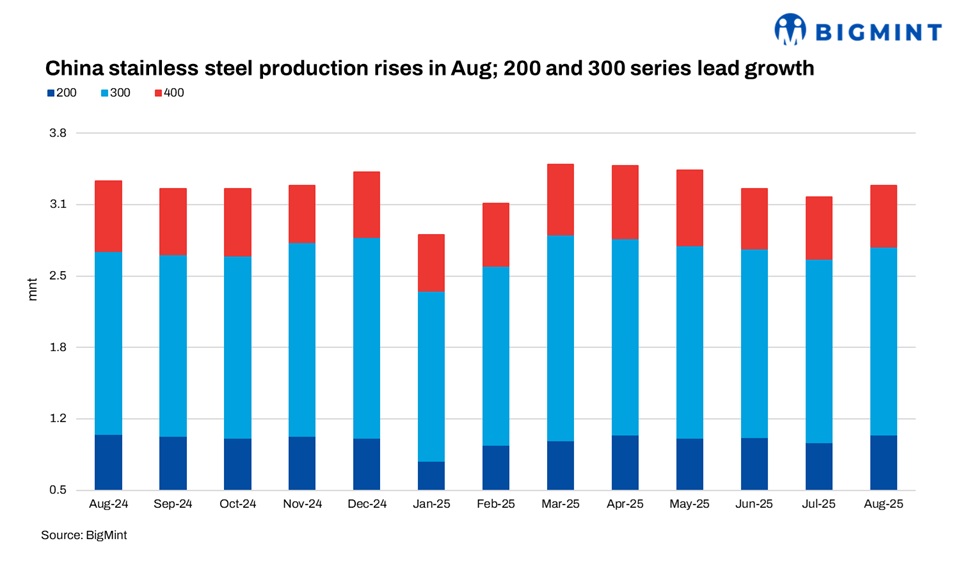

SteelDaily: China’s crude stainless steel production rebounded in August 2025, reaching 3.3 million tonnes (mnt), up 3.8% m-o-m but down 1.29% y-o-y. The increase was driven largely by strong performances in the 200- and 300-series grades, while the 400-series remained subdued. Production momentum is expected to carry into September, with forecasts pointing to 3.44 mnt, a rise of 3.8% m-o-m and 4.8% y-o-y.

Series-wise output

- 200 series: Production of 200-series stood at 1.01 mnt, up by 7.4% m-o-m, but a drop of 1% y-o-y as compared to last year.

- 300 series: Output of 300-series amounted to 1.74 mnt, 2.4% m-o-m rise and 3% y-o-y increase from last year’s 1.70 mnt.

- 400 series: Conversely, 400-series production remained largely stable m-o-m and a 12.23% y-o-y decrease, totaling 0.57 t.

September projections suggest continued growth, with the 200- and 300-series expected to rise 2.65% and 3.73%, respectively, while the 400-series could rebound with nearly 6% growth.

Hot-rolled and long products

Hot-rolled stainless steel production rose 5.9% m-o-m to 2.2 mnt in August, though it was 2.1% lower y-o-y. Within this, 200-series hot-rolled steel surged 11.3% m-o-m to 819,300 t.

- Bars: Production dipped 1% m-o-m but jumped 28.2% y-o-y to 180,000 t.

- Wire rods: Output rose 2.8% m-o-m and 19.1% y-o-y.

Cold-rolled stainless steel

Cold-rolled stainless steel production climbed 1.4% m-o-m to 1.48 mnt in August, up a sharp 9.6% y-o-y. The 200-series led growth with a 10.8% m-o-m rise, while the 300-series slipped 1.2% m-o-m. From January to August, cold-rolled output totaled 11.14 mnt, up 5.1% y-o-y. September production is forecast at 1.52 mnt, with 200-series output expected to hit a yearly high.

Outlook

China’s stainless steel rebound reflects mills resuming normal operations after maintenance shutdowns and stronger downstream demand. The 200- and 300-series continue to dominate the market, while the 400-series shows signs of recovery. Analysts suggest the near-term outlook remains positive, underpinned by seasonal demand and stabilized production levels.

Leave a Reply