- Crude steel production drops to combat overcapacity

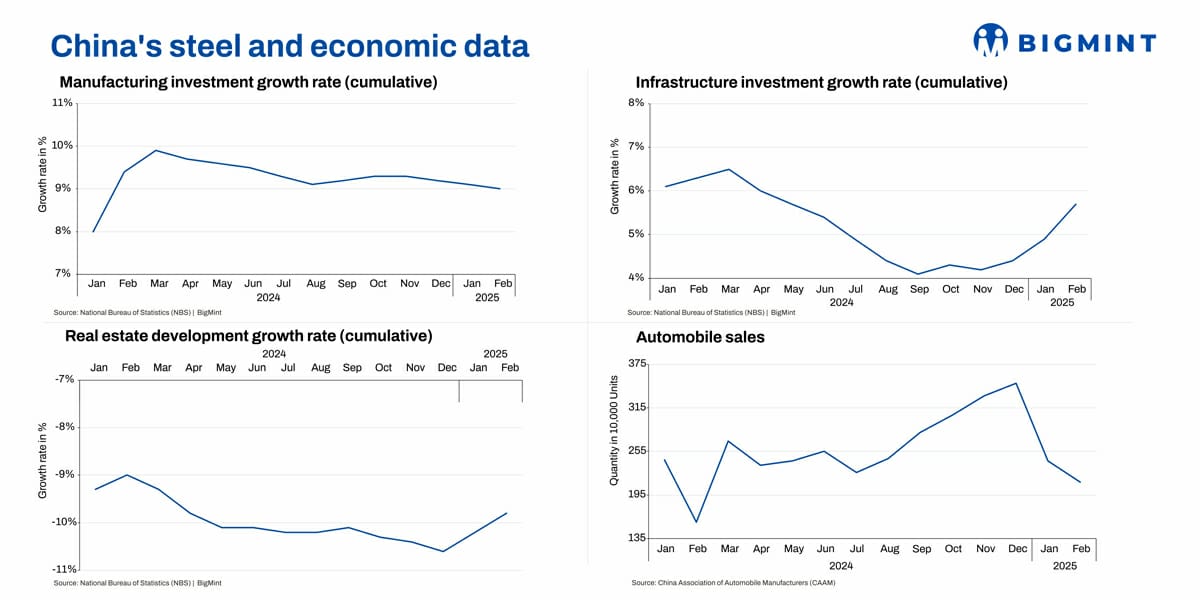

- Infra investment surges to 11-month high in Feb’25

- Realty still down but Feb momentum eases m-o-m

Morning Brief: China began 2025 with a mixed but promising performance across its key macro indicators. Crude steel production continued to fall to rationalise the overcapacity mills are grappling with. Manufacturing and infra investments did not perform poorly even though real estate continued to flounder. Exports retained their momentum, offering the much-needed solace in the face of poor home demand.

Crude steel production continues to fall: China’s crude steel production over January-February, 2025 showed a 1.50% y-o-y decline to 166.30 million tonnes (mnt). For the full year 2024, output dropped 1.70% to 1,005 mnt.

This continued production undercutting denotes the pressures mills are facing in the face of sustained overcapacity amid sluggish home demand. China had decided to continue with crude steel output controls and promoting industry restructuring this year to promote development of high-quality steels, as per a draft plan for national economic and social development in 2025, released during the much- anticipated “Two Sessions” meetings — the annual conference of the National People’s Congress and National Committee of Chinese People’s Political Consultative Conference, held recently in Beijing. Although the National Development & Reforms Commission (NDRC) has not specified any production cut targets, speculations are rife of further cuts to rebalance market dynamics.

Pig iron production also dipped 0.50% in this period to nearly 141 mnt.

Iron ore imports trail output cuts, fall 8%: China, needless to say, is the largest guzzler and importer of this key steel-making raw material. However, with crude steel experiencing sustained production cuts amid the lack of domestic demand, iron ore imports have also fallen correspondingly. Over January-February, 2025, these fell 8.40% y-o-y to over 191 mnt. However, for the full year 2024, iron ore imports were up 5% to 1,237 mnt, propelled by the higher exports needs, enticement to stock up during the phases of weak pricing and ahead of the various festive breaks.

Steel exports continue northward march: China’s steel exports continued their northward march into the new calendar. Volumes rose almost 7% y-o-y to 17 mnt over January-February, 2025. In 2024, these spurted by 23% to 111 mnt. Mills, pressured by a lack of home demand amid overcapacity, have no option but to look overseas to sell their products. A key ploy for selling overseas has been its predatory pricing.

HRC export offers over January-February averaged $470/t, the lowest when pitted against India’s $505/t, Japan’s 477/t and Russia’s $482/t, all on FOB basis.

Imports, meanwhile, dropped over 7% to 1.05 mnt in the first two months of the calendar and this is not surprising considering mills are not being able to sell their products at home.

Manufacturing investment growth range-bound: Manufacturing investment growth remained range-bound, hovering in the vicinity of 9% across both months under consideration and this is a slight drop from the 9.2% seen in December 2024 and 9.3% over October-November 2024. China’s industrial output expanded by 5.9% y-o-y in January-February 2025, marking a slight slowdown from December’s 6.2%. Growth remains steady, but data suggests mounting external pressures, including US trade tariffs and subdued global demand, are beginning to weigh on the country’s manufacturing sector. The manufacturing industry grew by 6.9% y-o-y, supported by strong gains in high-tech and equipment manufacturing.

Automobile production rose over 16% over January-February, 2025, to 4.55 million units, indicating manufacturing is holding firm.

Infra investment growth spurts in Feb m-o-m: Infrastructure investment grew an average 5.3% in the first two months of the calendar. Actually, February’s growth of 5.7% was at an 11-month highest since May 2024, reinforcing that the economy improved somewhat with the start of the year. Infrastructure investment expanded by 5.6% y-o-y.

Private investment remained flat y-o-y, indicating continued caution in the business environment. However, when excluding real estate, private investment grew 6%, suggesting stronger confidence in other sectors.

Realty still losing ground but momentum eases: Real estate investment contracted by a further 9.8% provisionally in February 2025 but which was a tad better against a decline of -10.2% in January. However, the decline in newly built commercial building sales showed signs of easing. The floor space of newly built commercial buildings sold decreased 5.1% y-o-y, but this was a 7.8 percentage point improvement compared to 2024. Similarly, total sales value of commercial buildings fell by 2.6%, a significantly narrower decline than the 14.5 percentage point drop recorded in the previous year.

In tandem with the declined scenario in the real estate space, cement production fell 6% y-o-y to 171 mnt in January-February, 2025.

Coal production, imports rise to meet domestic needs: China’s coal production rose 8% to 770 mnt across both months under review while imports of the same were up 2% to 76 mnt. This trend was in keeping with miners response to Beijing’s commitment to attaining energy security for meeting higher domestic power needs during winter heating. However, the NBS data revealed that the nation’s electricity generation fell 1.3% y-o-y to 1,492.1 billion kilowatt-hours (kWh) in the first two months of this year, with a 5.8% y-o-y downturn in thermal power production (mostly coal-fired) at 1,021.4 billion kWh which has caused concern that going forward output may need to be capped.

Outlook

Going forward, it is to be seen whether China will be able to sustain this slight economic upturn through the year. Much will depend upon its own policy support as well as external headwinds in the form of US trade strategies as well as stricter carbon emission-related guidelines. With the EU aiming to impose carbon tariffs on steel, aluminium, cement and other commodities from 2026, China’s steel exports to the EU will face a carbon cost of $54-76/t. Therefore, it is imperative for China to strengthen its green competitiveness in global markets.

Leave a Reply