- Export-oriented manufacturing drives steelmakers to boost output

- Steel exports cross 10 mnt in Jun’26 for second consecutive month

- Chinese mills resorting to indirect exports to bypass steel trade barriers

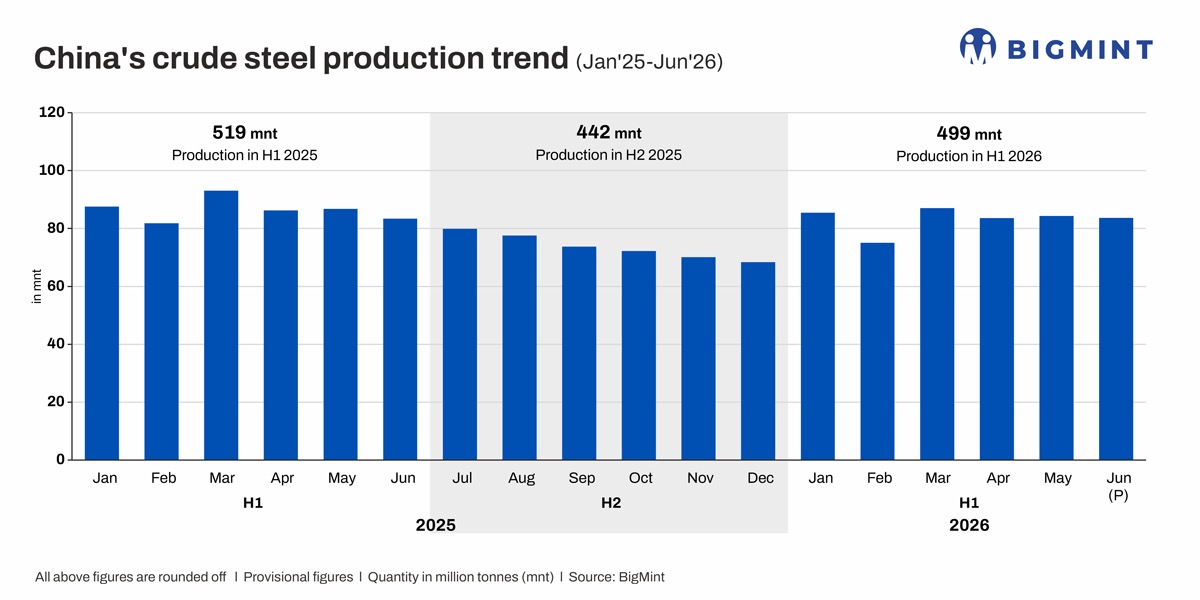

Morning Brief: China’s crude steel production rose 0.4% y-o-y to 83.67 million tonnes (mnt) in June 2026, marking the first y-o-y increase since April 2025, according to data released by the National Bureau of Statistics (NBS). The increase was driven by export-oriented manufacturing activity, as domestic consumption remained sluggish despite retail sales inching up by 1% y-o-y.

China’s total merchandise exports rose 27% y-o-y in US dollar terms in June, the fastest pace since October 2021. Shipments to the US climbed around 14%, according to CNBC, as manufacturers accelerated exports ahead of the possible expiry of the temporary tariff truce on 24 July. The improvement lifted factory activity across machinery, automobiles, appliances, and engineering products, translating into stronger steel demand.

However, crude steel output still fell 0.8% m-o-m from 84.31 mnt in May, indicating mills remained cautious amid weak profitability and continued efforts to avoid excessive inventory build-up.

Export-led manufacturing offsets weak construction demand

China’s manufacturing sector has increasingly relied on overseas demand as domestic consumption remains subdued following the cessation of a number of consumer trade-in programmes.

The official manufacturing Purchasing Managers’ Index (PMI) has remained above the 50%-point expansion threshold since March, signalling a gradual recovery in industrial activity given that the index was in contraction territory for much of the past year.

The recovery has been driven primarily by export orders rather than domestic demand. Exports of household electrical appliances rose 16% y-o-y in June, motor vehicles (including chassis fitted with engines) increased 73%, ships gained 12%, general machinery climbed up 15%, and high-tech products jumped 52%, underscoring strength across steel-intensive manufacturing sectors.

Automobile exports, in particular, jumped 75% y-o-y to a record 1.037 million units in June, surpassing one million units for the first time. In contrast, China’s overall vehicle sales declined 3% to 2.8 million units, as domestic sales dropped 23% y-o-y to 1.773 million units. New energy vehicle (NEV) exports reached a record 523,000 units, rising 1.6 times from a year earlier.

Additionally, air conditioner exports surged 42% y-o-y during H1CY’26 as an intense European heatwave boosted demand.

The improvement in manufacturing has only partly offset continued weakness in the property sector, where new housing starts, real estate investment, and land purchases continue to contract. As a result, China’s steel demand is becoming increasingly dependent on manufacturing and exports rather than construction.

The shift also reflects China’s growing reliance on indirect steel exports. As anti-dumping duties and safeguard measures increasingly target Chinese steel, manufacturers are exporting more steel embedded in automobiles, machinery, household appliances, ships, and renewable energy equipment. Dao Fortune estimates that nearly 30 mnt of China’s steel exports could be affected by trade measures in CY’26, almost double the 14-15 mnt impacted last year.

The divergence between manufacturing and construction has also influenced finished steel production trends. Flat steel production has generally outperformed construction steel, although performance within the flat steel segment has varied.

Hot-rolled coil (HRC) production fell 6.7% y-o-y to 88.5 mnt during January-May, likely reflecting weak demand and the growing number of trade actions targeting HRC exports. In contrast, cold-rolled coil (CRC) output increased 5.6% to 20.7 mnt, supported by stronger demand from appliance and manufacturing sectors. Rebar production declined 12.2% to 72.6 mnt, highlighting the continued weakness in construction activity.

Margins also remained under pressure for rebar more than flats. Average operating margins for rebars were a loss of RMB 71/t ($11/t) during June, compared with a loss of RMB 26/t ($4/t) for HRCs. Heavy plates remained one of the few profitable products, generating an average margin of RMB 43/t ($6/t), suggesting strong demand from the shipbuilding segment.

However, the modest increase in crude steel production despite the sharp recovery in manufacturing exports suggests mills continue to prioritise inventory discipline and cash flow over maximising output. Steel inventories remain elevated, and July-August also typically sees slow domestic demand.

Steel exports remain above 10 mnt for second consecutive month

China’s finished steel exports rose 6.6% y-o-y to 10.32 mnt in June, marking the first y-o-y increase in six months and remaining above the 10 mnt mark for a second consecutive month, according to General Administration of Customs (GACC) data. The rebound helped mills sustain production despite subdued domestic steel demand.

According to Japan Metal Daily, shipments to Gulf Cooperation Council (GCC) countries recovered after disruptions linked to the Strait of Hormuz, with exporters increasingly routing cargoes through Saudi Arabia’s Jeddah port. Chinese suppliers have also stepped up sales to Southeast Asia, Africa, and Latin America to diversify export destinations.

Additionally, although finished steel exports fell 5.6% y-o-y to 54.9 mnt during H1CY’26, exports of semi-finished steel continued to rise sharply. During January-May, semi-finished steel exports reached 6.8 mnt, up 43.2% y-o-y from 4.8 mnt a year earlier.

The surge in semi-finished exports has partly offset weaker finished steel shipments. Combining finished and semi-finished products, China’s steel exports during January-May declined by roughly 3.5% y-o-y, compared with an 8.1% drop in finished steel exports alone. The figures suggest Chinese mills are adapting to tighter trade restrictions by changing their export mix rather than materially reducing overseas sales. This is another factor that has sustained steady crude steel production.

Outlook

The key question in H2CY’26 is whether external demand can continue to offset domestic weakness. BigMint believes that the slight y-o-y increase might be a temporary development rather than the beginning of a sustained reversal of the downtrend seen earlier this year.

First, China’s trade surplus with major importers continues to widen, prompting governments to step up measures to protect domestic manufacturing. The EU, for instance, is expected to tighten scrutiny of Chinese imports as it seeks to revive its industrial base and improve capacity utilisation among domestic steelmakers.

China has, however, demonstrated considerable flexibility in adapting to changing trade conditions. As anti-dumping duties and safeguard measures expanded to cover more finished steel products, exporters rapidly increased shipments of billets and slabs, which remain outside the scope of most trade actions.

At the same time, Beijing’s push towards high-value manufacturing, including electric vehicles, renewable energy equipment, semiconductors, robotics, and AI-related industries, is creating new sources of steel demand that are less dependent on the property sector. These shifts should help support crude steel production, although they are unlikely to generate enough demand to drive a meaningful expansion in output.

Domestic investment trends also remain unfavourable. Growth in both manufacturing and infrastructure investment moderated during January-June, even if the slowdown was far less severe than the 18% contraction in real estate development. Together, they suggest China’s domestic steel demand is unlikely to strengthen materially during the second half.

Meanwhile, steelmakers continue to face weak profitability and elevated inventories. Export orders are also likely to slow as inflationary pressures emerge globally. Therefore, China’s crude steel output is likely to inch down through the remainder of CY’26.

Leave a Reply