- Realty sector woes choke steel demand

- Mills’ profit margins halve as prices tumble

- Steel mills facing brunt of rising global protectionism

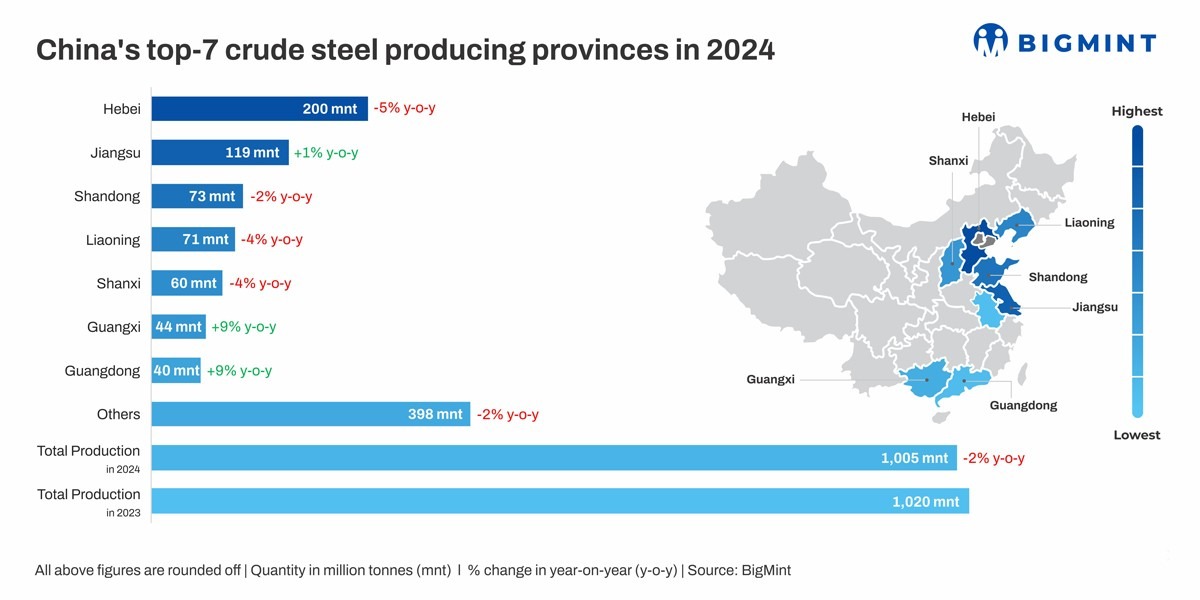

Morning Brief: China’s crude steel production shrank 2% y-o-y to 1,005 million tonnes (mnt)-1.005 billion tonnes (bnt)-in CY’24 against 1,020 mnt in CY’23, according to data maintained with BigMint.

Notably, although output stood at its lowest in five years, since 2019’s 996 mnt, the figure remained above the one-billion-tonne mark, as has been the norm since 2020.

Since CY’21, a range of factors, including an ailing property sector, subdued demand, and tumbling steel mill margins, has induced an atmosphere of gloom in China’s steel industry.

Government mandated steel production cuts have taken a toll. However, the decline has been incremental, with CY’21’s volume just 60 mnt lower than 2020’s peak of 1,065 mnt.

Province-wise crude steel output

Hebei emerged as the leading steel-producing province in CY’24. However, its CY’24 total of 200 mnt was 5% lower than that of CY’23 (210 mnt).

Second was Jiangsu, with 119 mnt, up 1% y-o-y from 118 mnt in CY’24.

Meanwhile, production in Shandong, Liaoning, and Shanxi edged down as well, by 2% to 73 mnt, 4% to 71 mnt, and 4% to 60 mnt, respectively, compared to 75 mnt, 73 mnt, and 63 mnt in CY’23.

In contrast, there were certain pockets of growth, with both Guangxi and Guangdong recording a 9% uptick to 44 mnt and 40 mnt in CY’24, respectively, compared to 40 mnt and 37 mnt.

Factors impacting crude steel production

Steel consumption drops: Although crude steel production has hovered at around 1 billion tonne (bnt) over the past five years, domestic steel consumption has fallen steeply to 892 mnt last year from a peak of 1.05 bnt in 2020, as per CISA. This downtrend can be traced back to the 2021 collapse of the Chinese real estate giant Evergrande, which set off a property debt crisis that continues to plague the sector four years down the line.

Realty woes impact steel demand: Previously, the property sector used to anchor steel demand in China, consuming, in around 2010, over 40% of the steel production that year. However, in 2023, its share has declined to 24%. As a result, the steel industry has been struggling to redirect the huge volumes that the construction segment would consume. As such, it seems that in CY’24, steelmakers prioritised prudence, refraining from lifting output.

Producers stare at bleak profit margins: Chinese mills profits halved in CY’24, as most steelmakers regularly trimmed their offers as part of desperate efforts to lift sales. According to data from CISA, average profit margins of key enterprises dropped to 0.71% in CY’24 from 1.34% in CY’23, while annual profits of RMB 42.9 billion were recorded, lower by around 50% y-o-y.

Protectionist brickwall: Amid recessionary tendencies globally, countries have adopted stringent measures to protect their economies. Chinese mills have resorted to aggressive exports to recover production costs, and domestic prices of the recipients tumbled headlong as a result of the supply glut. Thirty-three trade remedy investigations were initiated against China in CY’24, which exceeds the total conducted during 2020-23.

Mills bank BFs amid unfavourable market conditions: Chinese mills also shut down blast furnaces for maintenance last year in response to persistent subdued domestic demand and poor profit margins.

Decarbonisation efforts gain focus: Steelmakers have been accelerating efforts to decarbonise steel production as part of China’s 2070 neutrality goals, given that (1) the sector suffers from overcapacity and (2) coal-based production remains dominant in steelmaking (around 90%) despite rollout of significant renewable energy capacity. To this end, in 2024, the government announced intentions to introduce regulations to curb the carbon footprint of several industrial products, including steel.

Outlook

Chinese steelmakers are expected to implement further production cuts in response to persistent dull demand afflicting the domestic industry. Prices and profits will recover only if the gap between supply and demand narrows.

However, producers are expected to redirect efforts to special steel manufacturing for the sunrise sectors such as electric vehicles and renewables, etc. over and above general manufacturing. This may keep crude steel production at relatively stable levels y-o-y in CY’5, although decline in China’s steel production is a phenomenon which seems to have certainly settled in.

Leave a Reply