- Washed coal inventory declines 26% since Jan’26

- Low inventories will continue to support prices

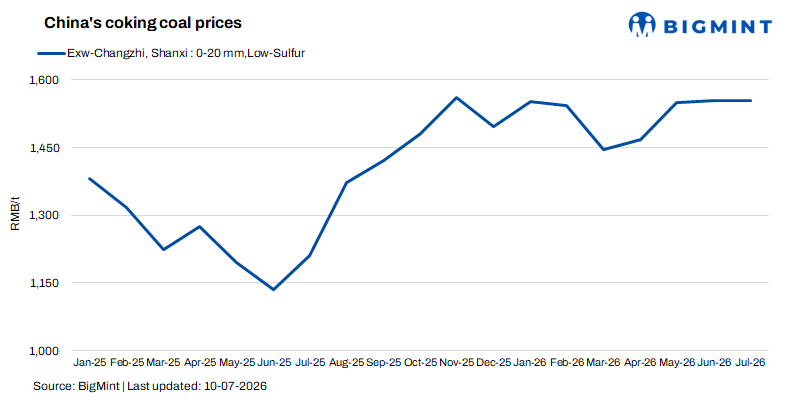

Mysteel Global: Following the strong trend witnessed in China’s coking coal prices during this year’s January-June half, the protracted supply tightness is expected to shore up the market during the current July-December period, with further increases in coal prices also in prospect, Mysteel’s half-yearly report on the commodity shows.

Incident-driven surges: China’s coking coal price trend in H1

On June 30, Mysteel Coking Coal index (MCCI), which tracks coking coal prices nationwide in China, stood at Yuan 1,712.3/tonne ($252.1/t) including the 13% VAT, surging 35% from the level recorded on December 31 last year of Yuan 1,267.4/t with VAT.

The jump in price over the six months was in sharp contrast to the first half of 2025 when an entrenched supply glut sent domestic coking coal prices into a steady decline, with MCCI ending the period on June 30 2025 at Yuan 938/t with VAT, the lowest level seen in years, as Mysteel Global reported.

For this year’s H1 period, the report emphasized that unexpected events boosted the domestic market. In March, sentiment in China’s coal market strengthened considerably from the escalated conflicts in the Middle East and the ensuing global energy chaos, the report notes. Participants highlighted coal’s role as a major energy source amid the disrupted supplies of oil and natural gas, driving up prices of the commodity, including those of coking coal, as reported.

Then in late May, the deadly mine explosion in North China’s Shanxi province triggered extensive safety inspections across the country’s major coking coal hubs, forcing numerous mines into suspension, as reported. Domestic coking coal prices surged rapidly following the sudden supply tightness and ended H1 at high levels.

Protracted supply tightness: China’s H2 coking coal market

Intensified inspection campaigns have severely impacted the operations of Chinese coking coal producers. After the Shanxi mine accident, coal production among the 523 coking coal miners that Mysteel regularly monitors nationwide in June lingered at the lowest levels since Mysteel began tracking the data in 2021. Over July 2-8, raw coal output among the sampled miners averaged only 1.48 million tonnes/day, almost on par with the lowest level recorded in July 2021, according to Mysteel’s survey.

Market participants anticipate that authorities will continue tightening controls on mine operations during this half. On July 1, a revised Standard for Determining Major Coal Mine Accident Hidden Dangers took effect, supplementing details on mine safety management, according to government documents seen by Mysteel Global.

The tighter regulations are also expected to keep domestic miners’ production during most of this half below H1 levels. Three years ago in 2023, mine accidents and concealment practices among some mining companies also prompted authorities to conduct frequent inspections of coal mines. As a result, average raw coal output among the 523 sampled miners dropped to 2.08 million t/d for H2 of the year, down 3.6% from the H1 average, Mysteel Global calculated based on the data.

In H1 of this year, the 523 miners’ average raw coal output reached 1.85 million t/d, already the third lowest half-yearly level since 2021, following the daily averages of 1.82 million tonnes in H1 last year and 1.83 million tonnes in January-June 2021, according to the calculation.

Low inventories at coal miners and washeries

Coal stocks among the 523 coking coal miners and 314 independent coal washeries under Mysteel’s survey have declined notably since late May, as the unexpected supply disruptions had prompted end-users such as coking plants and steel mills to build up their coal feed stocks. By July 9, their combined washed coal inventories stood at 4.58 million tonnes, lower by more than 26% from the beginning of the year, according to Mysteel’s tracking.

As end-users have tended to take a cautious stance when buying coking coal recently, low inventory levels at coal miners and washeries should help strengthen the bargaining power of coal suppliers. Meanwhile, the half-yearly report notes that low stocks could also amplify upward momentum in coking coal prices once demand improves, considering that supply disruptions will largely persist in H2.

Additional increases expected in prices: H2 outlook

Mysteel’s report expects tight fundamentals to further lift domestic coking coal prices in H2, though the pace of growth may slow from H1. “Low-sulfur primary coking coal is expected to fluctuate around Yuan 1,900-2,300/t and may top Yuan 2,400/t in an upside scenario,” the report says. On June 30, the sub-index for the coal type used for MCCI reached Yuan 1,991/t with VAT, Mysteel’s data showed.

“The prices of other primary coking coal types with mid- and high-sulfur content and of fat coal are also expected to rise from H1,” the report adds.

It suggests increases in other lower-grade coal types are expected to be more modest during this half and cites imported coking coal as the substitute, especially given the ample supplies from Mongolia. “The quality of Mongolian coal is relatively unstable and tends to have higher ash and sulfur content. However, Mongolian imports still play an important role in supplementing domestic supply, contributing to more cost-effective coal blending for metallurgical coke makers,” it adds.

According to China’s General Administration of Customs, China’s coking coal imports from Mongolia over January-May totaled 33.39 million tonnes, surging 67% from the same period last year. The volume also accounted for around 61% of China’s total coal imports during this year’s first five months.

Note: This article has been published in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply