- Shanxi disruptions are tightening domestic coal supply sentiment

- Summer restocking could lift coal prices and import demand

China’s thermal coal market is entering a critical transition period. After a softer April marked by weaker imports, stronger hydropower generation and resilient domestic coal supply, the market had begun stabilising. Buyers appeared less urgent, seaborne prices softened and inventories remained comfortable.

But just as the market settled into a hydro-led cooling phase, widening mine shutdowns and inspections in Shanxi have begun introducing fresh uncertainty — raising questions over how much supply cushion China really has ahead of peak summer demand.

The key issue is no longer whether thermal coal demand has weakened — April data suggest it has not. Instead, the focus is shifting to whether domestic supply and logistics can sustain a market that looked increasingly comfortable only weeks ago.

Hydro gains and domestic supply cool April imports

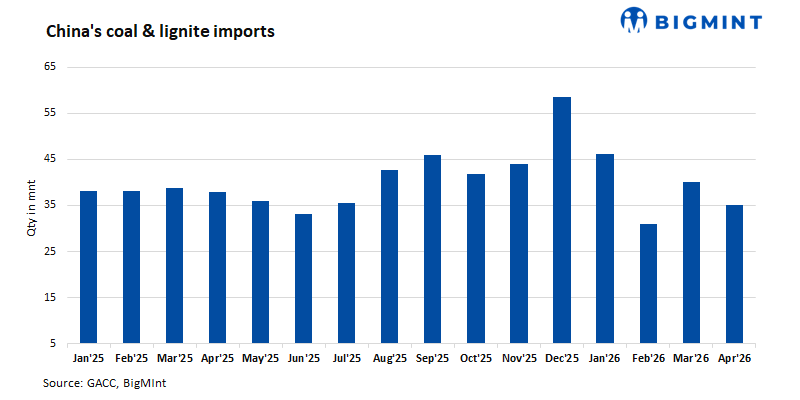

China’s non-coking coal imports weakened in April 2026 as stronger hydropower generation, elevated inventories and stable domestic output reduced procurement urgency.

Imports stood at 9.42 million tonnes (mnt) in April, down from 10.06 mnt in March and 11.38 mnt in April 2025, reflecting a 6.4% month-on-month (m-o-m) and 17.2% year-on-year (y-o-y) decline.

Yet the broader trend was less bearish than headline April numbers suggest. During January-April 2026, China imported 41.60 mnt of non-coking coal, compared with 43.31 mnt a year earlier, representing a relatively modest 3.9% y-o-y decline.

The moderation reflected weaker buying urgency rather than weak demand.

Heavy rainfall across southern China boosted hydropower generation, reducing coal burn at the margin, while domestic coal production remained resilient, albeit softer at the margin. China produced around 385 mnt of raw coal in April, down 1% y-o-y and 12.5% m-o-m from approximately 440 mnt in March. During January-April 2026, cumulative raw coal production reached around 1.58 billion tonnes, broadly flat (-0.1% y-o-y), suggesting supply remained stable but was not meaningfully expanding heading into summer.

Higher freight costs also weakened import competitiveness, particularly for lower-rank Indonesian coal, encouraging utilities to prioritise domestic tonnes.

Supplier mix shows selective weakness

The slowdown in imports was broad-based, though uneven.

Australia remained China’s largest non-coking coal supplier, but shipments weakened materially. Imports from Australia during January-April stood at 18.44 mnt, down 11.9% y-o-y from 20.94 mnt.

Indonesia also softened, with imports slipping to 5.00 mnt, down 5.7% y-o-y, reflecting weaker import economics and softer demand for lower-calorific-value coal.

Russia proved comparatively resilient, with shipments edging slightly higher to 10.62 mnt, broadly stable against 10.47 mnt last year.

Mongolia emerged as the clear outperformer. Rail-linked imports rose to 6.81 mnt, up 20.3% y-o-y, benefiting from stable overland logistics and insulation from maritime freight volatility.

The takeaway is important: China’s softer imports reflected temporary comfort with domestic availability — not a collapse in thermal coal demand.

Indeed, power sector data suggest coal consumption remained resilient. During January-April 2026, China’s total power generation increased 3.3% y-o-y, while thermal power generation rose 3.1%, despite hydropower output surging 12.2%. In other words, hydro eased coal burn at the margin, but did not displace coal demand materially.

Shanxi disruptions are changing sentiment

That narrative, however, is beginning to shift.

Following the recent Shanxi mine accident, surveys indicate around 109 mines have been shut, representing an estimated 122 mnt of production capacity, with roughly 319,500 tonnes/day of raw coal production disrupted.

The immediate impact remains concentrated in coking coal. But thermal coal markets are reacting because traders increasingly fear a broader safety inspection cycle across China’s major coal-producing regions.

The timing matters.

Provincial production data suggest momentum in China’s largest coal-producing regions had already begun softening before the accident. Combined coal output from Shanxi, Inner Mongolia, Shaanxi and Xinjiang fell to around 275.6 mnt in April, down 23.5% m-o-m and 12.2% y-o-y, even as national production remained broadly stable. That leaves less room for disruption as cooling demand accelerates into summer.

If inspections remain localised, the market is likely to absorb the disruption comfortably. But if scrutiny broadens or delays inland restocking, supply conditions could tighten faster than current inventory levels imply.

Inland replenishment is emerging as the real risk

The bigger concern may not be immediate supply loss — but where stress emerges.

Coastal utilities have reportedly relied more heavily on inland coal transfers and domestic logistics as imports softened, helping maintain relatively healthy coastal inventories. But this may have delayed replenishment deeper inland.

If temperatures rise through June and inland thermal plants begin restocking while Shanxi disruptions persist, competition for domestic tonnes could intensify quickly.

In effect, China may not have removed tightness from the system — it may simply have shifted it inland.

Qinhuangdao inventories may be giving a misleading signal

Northern port inventories have recently recovered after falling toward 0.5-0.56 mnt, but traders caution this may not signal oversupply.

The rebuilding partly reflects slower cargo turnaround and inland-to-coastal diversions rather than outright market weakness.

The more important signal will be whether outbound shipments strengthen in early June — potentially pointing to tighter inland replenishment demand.

Meanwhile, FOB Qinhuangdao 5,500 NAR prices have stabilised near CNY 845/t, suggesting a modest inspection-driven risk premium is now embedded in the market.

Outlook: April’s comfort faces its first real test

China’s thermal coal market is no longer simply a story of stronger hydro, stable supply and softer imports.

April reflected a market in temporary cooling mode. But lower import dependence, rising reliance on inland replenishment and fresh domestic supply uncertainty are beginning to test how durable that comfort really is.

The Shanxi accident has not fundamentally tightened the market — but it has exposed how dependent China remains on uninterrupted domestic production just as summer demand approaches.

External energy markets may soften if easing geopolitical tensions pressure crude, LNG and gas prices lower. Yet China’s summer coal balance is likely to be shaped far more by domestic production stability than by global energy sentiment.

The next 10-14 days may determine whether China remains comfortably supplied through summer — or shifts more quickly toward tighter thermal coal balances and stronger import demand.

Leave a Reply